By Judith Waker: Quite a few of us have come to explore economics and how they work later rather than sooner in our trading careers and there is no time like the last few weeks to really understand the mechanics in action.

By Judith Waker: Quite a few of us have come to explore economics and how they work later rather than sooner in our trading careers and there is no time like the last few weeks to really understand the mechanics in action.

With the Federal Reserve acting to end QE and the Japanese rocking the boat with ‘shock and awe’ that was more to do with their intentions than their results, it is also a time when the ‘energy’ we call ‘the market’ is tested constantly in both its stress levels and its wisdom.

It is said that the market always knows best and cannot be second guessed by any media or any Central Bank for that matter, and it is the market’s behaviour that holds the clues for the trader predicting the future of his own decisions.

Polar Opposites

Starting first with monetary policy.

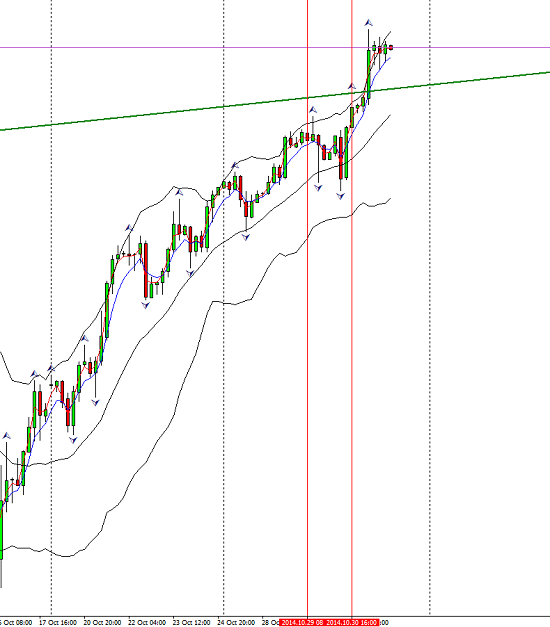

When I started to accumulate material for this week’s report on Thursday evening, it was going to be focused on the FOMC decision to end QE. This was indeed big news and had its effect felt in the market though only halted the equity uptrend to a minor degree. . Whilst interest rates stayed the same the tone of the FOMC was much more upbeat especially where employment statistics were concerned and the hawks had their way with the QE program. This after speculation only last week from a Fed member that more QE might be appropriate if the data doesn’t stand up to the growth tests. So yes it was unexpected but the market did seem to take it in its stride. Here is the S&P four hour chart for the 29th.

The dollar moved higher on the news as of course the end of QE signals the possible beginning of rate hikes although there was no indication of that happening any time soon.

Interestingly, Yellen did not mention monetary policy in her speech the following day and here it should be noted that there was a dissenter who believed that an inflation number of 2% should be achieved before the QE ship was abandoned.

On Friday morning all this was eclipsed by the stunning announcement of the BOJ to increase their Quantitative Easing program by another 10 trillion Yen. The Japanese central bank fear falling falling prices may pull them into deflation. What made this more of a surprise is Japan’s Mr. Kuroda has been upbeat on economic prospects of late but on Friday the fears seemingly returned. With gloomy global projections and negative wage growth they launched another round of ‘easing’.

European Monetary policy has not yet formerly adopted QE. All sorts of liquidations have been launched but now it may well be Mr. Draghi’s turn to head off inflation. Either way we can see that the diversity between these three giant economies and their policies are becoming ever more polarised.

A depressing perspective of Japan against Euro data

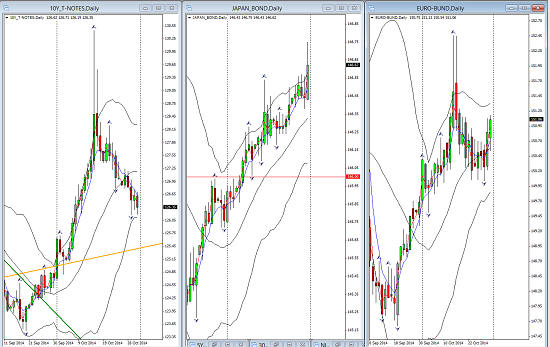

The Revelations of the Bond Market Action This Week

The Bond market has revealed its own wisdom this week. As the following chart displays very clearly, Japanese and European Bonds have headed up bringing yields ever lower. The US bonds declined this week as their yields rose on continuing and now affirmed expectation of economic recovery.

The comparison of the week, the German 10 year Bund yield versus the US 10 year note yield.

It closed at 0.84, admittedly above its low for the month but the downtrend is disturbing for those trying to be optimistic for even a weak recovery. The US up-beat week was reflected in the US bond market not just in the 10yr note but across the board. Here is the bond price inverse to the yield in the 5yr and 30yr note.

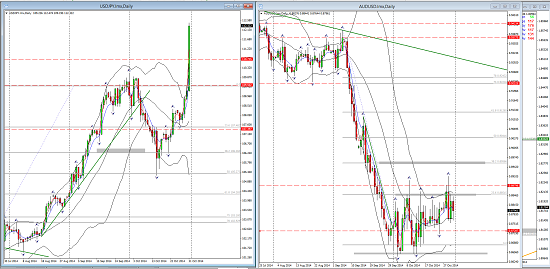

And the dollar reacted even more to Japanese news than to the FOMC earlier in the week. With deflation looming in the Eurozone and in Japan there is no way for the Dollar than to resume it’s uptrend and that is precisely what it did. Whilst wild moves were seen in the USDJPY and the EURUSD, there are pairs still in consolidation which presents dollar buying opportunities. These 2 charts show the different effect in the USDJPY and one of our commodity pairs, AUDUSD

Commodities did have a better week, oil consolidated on its lows from last week and Gold took another step downwards. There is still no doubt of the weakness in commodities generally so any breakout on the downside in the Aussie or the Kiwi may be particularly fruitful. The Canadian economy showed us a shrinking GDP moving to a minus number, a lot to do with a sinking oil price. This is the first contraction in 8 months.

Polar Bears! (you can see where this is headed!)

Back to the eurozone. Euro inflation shows weak signs of rising to meet expectations rising from 0.3 to 0.4 although core inflation dipped. There was no change in jobless numbers and holding steady does not meet the brief when deflation is the worry. Without ‘Japanification’ Europe is likely to continue shrinking so the pressure continues to build. Germany has opposed any full-on QE and the argument is that with costs of borrowing already at extreme low levels it might not work any way. While Germany resist investment, Italy and France struggle on as do the periphery countries. The Euro may have a good deal further to fall. When assesing data from Europe it is always important to look behind it at the many individual economies it embraces. Jobless numbers hold hidden problems for example with Germany on 5% , France twice that on 10% Italy at 12.5% and Greece at a little in excess of 26%.

What to Watch for next Week

A slew of PMI’s next week. Statistics so far show the US ahead of the pack by some margin and bearing in mind that 50 is critical for growth this is an interesting over-view. Again, taking this into account, this table shows exactly why the global outlook has been downgraded to dismal! Lets see if the week’s data changes anything here;

Euro retail sales are due out Wednesday, Aussie employment on thursday, with the UK rate and and ECB press conference the same day. And of course on Friday the always important non-farm payrolls especially now that Hawk-watch is back on the screen. Oh and to that you can add yet another Fed member speech for more clue hunting. The sentiment barometer as discussed last week showed strong equity moves in the last seven days, with bonds gaining and the AUDJPY in ‘take off’ mode. With the Vix slipping back to 14 there leaves little room to doubt the mood of the markets.

Plenty of action to watch for next week and as we know from these incredibly unpredictable times in the markets as a whole, be prepared and protected for anything!

Judith Waker

0 Comments