Last week was a tricky one for FX traders, with thin volumes and material difficult to interpret especially in the longer term. Could this devaluation continue? Could this cause capital flows from China? Could cheap Chinese exports create havoc in its neighbouring economies and particularly in the larger economies such as the EZ?

Could this indeed change the view of the FOMC and hinder the tightening cycle launch and slow down the timetable? Of course as the week progressed and the alternatives considered, it was inevitable that the focus would once again rest on US policy.

The macro issue that has the potential to develop into a major theme is the risk trends.

Preparing For Profit : Watching the Renminbi

Two focal points followed as far as the ‘watchers’ were concerned; the first was the acknowledgment that this is a way for Chinese deflation to be exported across a global economy whose recovery is fragile to say the least. The second is that the Chinese have either consciously or otherwise begun a currency war. John Kicklighter at daily fx referred to it rather as a currency cold war, since it has to be true that where monetary policy concerned no-one is going to admit that their devaluations are for purposes of gaining global advantages and that all policy comes under the umbrella of promoting the individual country’s economic health and managing it as best as possible. Its a valid point and there is no mechanism for effectively preventing it even if currently it is more of a debate than a reality.

What ensued on an interpretive level was somewhat confusing in that the opinions of the professionals have been mixed and conflicting. It did not help that the first devaluation, by way of an adjustment with the ‘fix’ and which amounted to 1.9% was labelled a one off event. This one off event was to be followed by a second which brought the total devaluation to 2.85%.

Time alone will tell if the Chinese devaluation continues or reaches dangerous levels and because t will take time speculation will continue. I do not think there is any doubt that the decision and the ensuing discussion has rattled the market.

Preparing For Profit: The State Of Play In The USA

Close-up of United States Federal Reserve System symbol

With the China headwinds and the obvious debate about the extent to which the devaluation has affected the Fed decision on rates, the data flowed in pretty steadily supporting US recovery and growth patterns. The Jolts number missed by a fraction but elsewhere expectations were met and with PPI and Industrial production, they were exceeded.

The all important retail numbers came in on the expected number as did the core. The September hike is still on the table and the sentiment by and large is that there is a majority to go ahead. The dovish Dudley, whilst reticent on Chinese effects, still referred to the interest rates rising ‘in the near future’ .

There is little doubt now that there is sufficient improvement on the domestic front to warrant the beginning of the tightening schedule.

Next week brings two major US events, the FOMC minutes (which of course pre-date the China move) and CPI and core CPI. That is another crucial piece of data to the Fed and thus to the speculators.

Preparing For Profit : Focus of The Week; Risk Trends

Risk-on or risk-off?

These last few weeks have shown concepts of both environments and that is not unusual. To have a black and white definition is rare, but what is significant is that the reactions are showing increasing nervousness.

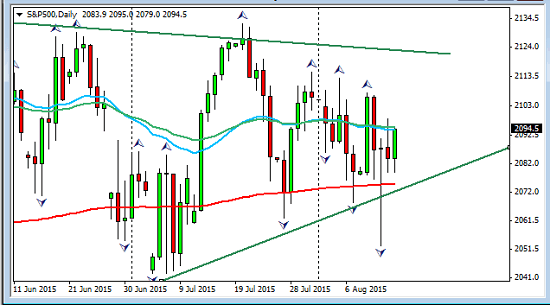

The US equities are always at the forefront of this deliberation. This week was slightly on the upside but the weekly chart does not look particularly strong is in a technical downtrend and has tightened into a relatively small range.

The Daily chart lshows the fear factor we saw during the week as China twice announced a move;

The Dow looks similar as would be expected;

The problem for equities is that if we shift further into a risk aversion environment they are set for a fall. It looks like the danger is a double edged sword, for equities will suffer also even in a risk on scenario, should the Fed go ahead with the first hike. That presents something of a self-fulfilling prophecy.

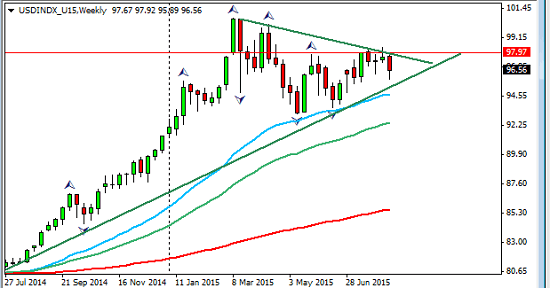

As for the US Index, the week was down on the Asian news although recovering from the lows on Friday as PPI came in strongly.

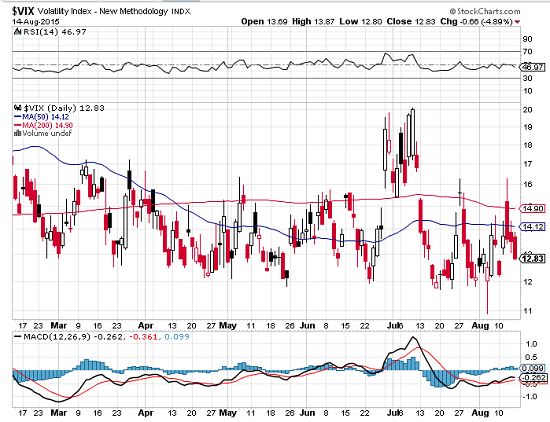

The Vix shows little in the way of fear, chart courtesy of stockcharts.com

This is not a clear risk aversion scenario but nonetheless it is a wary and sensitive market and we know if it shifts further the rules will change and we should be prepared.

The AUDJPY should be on the radar if there are further shifts towards aversion

Preparing For Profit: The Other Side Of The Pond

There have been some factors that have buoyed up the Euro. A settlement with Greece has been one of them although it should be noted that the IMF is still calling for debt relief from the ECB before they themselves commit. The data coming from the zone has been improving but no doubt GDP numbers this week were a little disappointing and don’t yet point to a reliable recovery and thus any early talk of QE ending early was nipped in the bud by this weeks set backs which of course include the Chinese devaluation. To say the EZ is not out of the woods yet is the ‘feel’ from the market. The misses on the numbers in the individual countries were not massive but seen together with the new deflationary threat it could promote more gloom than faint optimism. It is vital to see content in context.

There have been some factors that have buoyed up the Euro. A settlement with Greece has been one of them although it should be noted that the IMF is still calling for debt relief from the ECB before they themselves commit. The data coming from the zone has been improving but no doubt GDP numbers this week were a little disappointing and don’t yet point to a reliable recovery and thus any early talk of QE ending early was nipped in the bud by this weeks set backs which of course include the Chinese devaluation. To say the EZ is not out of the woods yet is the ‘feel’ from the market. The misses on the numbers in the individual countries were not massive but seen together with the new deflationary threat it could promote more gloom than faint optimism. It is vital to see content in context.

The fact is that the same factors that threaten a deflationary downturn can also bring a short term buzz in GDP.

There has been evidence for a while that the Euro has become a funding currency so expect bullish moves (quite unrelated to underlying strength) if the risk environment develops into aversion. The growing yield differential only adds weight to this proposition.

As for the UK, some disappointing labour numbers this week have underlined the changing speculation on the outlook for the GBP. Still in number two position for interest rates it has seen some challenges in the inflationary path including wage growth, an important concept of inflationary traction which missed its expected number. It is decreasing in strength as far as the recovery is concerned and where it is in the monetary policy curve but this does alter the position has comparatively to the global economies.

The Antipodes

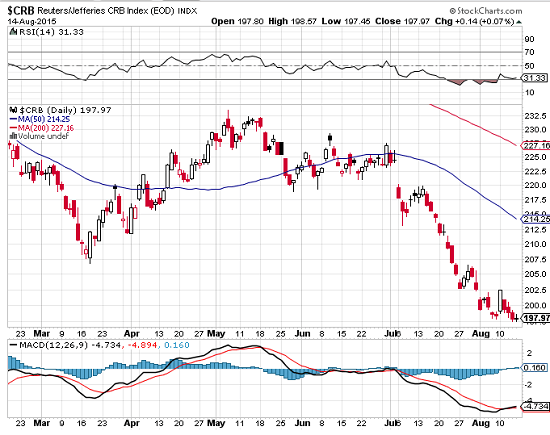

China has exacerbated the situation with commodity currencies effectively improving exports for themselves they have increased costs elsewhere and no more so than in Australia. New Zealand continues to deteriorate spurred by the collapse in the dairy industry. Commodities are still falling

chart courtesy of stockcharts.com

Oil continues its decline;

The Week Ahead

Aussie Monetary policy minutes are Tuesday. along with GBP CPI, a major catalyst. Also NZ dairy prices and US building permits.

Wednesday is the another big number for the US, CPI and core CPI. Also we see the FOMC minutes

Thursday brings JPY policy abd statement from the BOJ, GBP retail sales, US unemployment and Cad Wholesale sales.

Friday sees more eurozone PMI, French and German, and more CPI this time from Canada.

Summer Winds

Time to take care, this last week’s unpredictability, warns of the thin volumes and the truth is many professionals are away from their trading desks. If you must trade, proceed with caution and impeccable risk/ reward management. If you prefer, then use this time to consider and monitor the development of the longer term themes we can use to our advantage when September brings the volume back to the FX. As summer winds blow (and I live in the UK , I should know!) err on the side of caution. With all the changes they may bring , they may also waft in some clarity and opportunity and therein lies the edge.

Time to take care, this last week’s unpredictability, warns of the thin volumes and the truth is many professionals are away from their trading desks. If you must trade, proceed with caution and impeccable risk/ reward management. If you prefer, then use this time to consider and monitor the development of the longer term themes we can use to our advantage when September brings the volume back to the FX. As summer winds blow (and I live in the UK , I should know!) err on the side of caution. With all the changes they may bring , they may also waft in some clarity and opportunity and therein lies the edge.

Judith Waker

0 Comments