In a world where Central banks intervene to unprecedented levels to avoid the economic pitfalls, particularly the threat of deflation, the understanding of the fundamentals that drive the market, the Global Macro environment is becoming ever more important to understand in order to trade successfully and reduce some of the risk.

And then there are the geo-political concerns.

Unrest in Russia and Ukraine , the IS movement, terrorism fears; so much is brought to our attention by the media that it is easy to develop a kind of press immunity. And yet we should watch the signs as we all know that events from this category have the ability to rock the markets or at least send shock waves and we should know how to anticipate and prepare for them.

Being news -aware, whether it be monetary policy, daily data, world conflicts or how the equity and bond markets are moving are tools of our trade.

In this column I will sum up the preceding trading week as I see it, focusing on the Global Macro scene, including what to look for in the week ahead.

In the last few weeks a lot of focus has been on monetary policies, the growing divide between loosening in Europe and Japan and tightening in the US. The FOMC ending QE, the Japanese dumping another 10 trillion into their economy and there seems to be a hawk or a dove in the news every day.

Geopolitical events have admittedly quiet in comparative terms for a few weeks but there are multiple fragilities to watch out for in a world of ‘hot spots’ .

With the price of oil causing deep problems in Russia where sanctions are beginning to bite, trouble seems to be brewing again on the borders with Ukraine.

Forty two Russian tanks crossed over on friday, a step criticised by NATO and had the Ukraine President announcing a breach in the treaty agreement.

It’s a bit of a chicken and egg situation, the currency is no doubt in trouble as a result of the drop in oil prices and a pressured Putin has chosen to accelerate tensions in Ukraine, which brought his country into the turmoil of sanctions in the first place.

This renewed action caused Friday’s rout in the rouble which lost 8% in one week. Russia is in the midst of a financial crisis which can only increase anxiety for an already unstable region.

In terms of overall sentiment of the global market, events such as these will need to be monitored. With an equity market at all time highs with no outward signs of nerves , all seems well. Here is the vix at surprisingly low and steady levels as the following chart shows;

Stockcarts.com

Stockcarts.com

However geopolitical events as we have seen from the past can change the scenery very quickly. We trade for the present with a fundamental eye on the future. That is the way it is for traders interested in the long term.

Commodities in Crisis

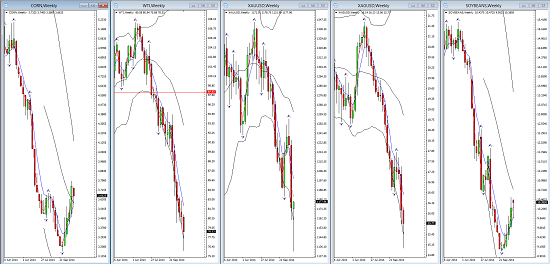

Its almost impossible to discuss any event or piece of data this week without discussing the price of oil. Commodities are dropping across the board. The following chart shows the moves since March this year in some of the key commodity markets, corn, oil, gold, silver and soybeans.

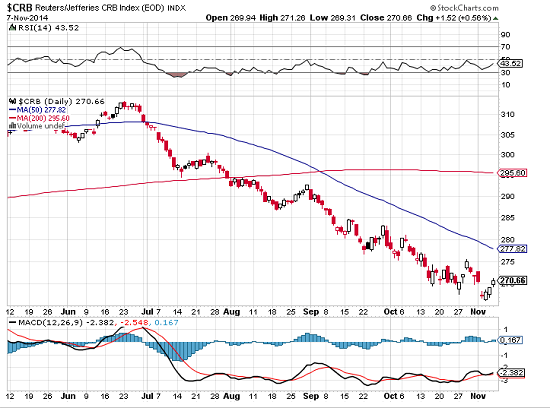

The weekly chart of the CRB, the index of commodity prices shows levels at 26 month lows ealier this month, although an improvement was seen this week;

courtesy of Stockcharts.com

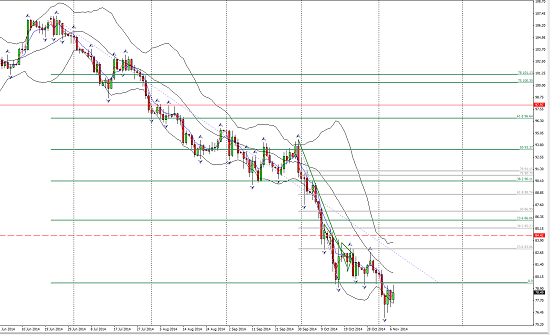

And this is Crude Oil on a daily chart.

This week it settled out at 78.49. So who are the beneficiaries? There is some interesting data around and somewhat speculative. It is about identifying producers and consumers and of course like the US some fall into both categories. Russia and most of the the Opec countries are most at risk, There are 12 member countries in Opec, Saudi Arabia, Iran, Kuwait, Venezuela, Qatar Indonesia, Libya, UEA, Algeria, Nigeria and Angola. Most of these (with the exception of Kuwait) need oil trading at 110 and more in Venezuela. Canada is also a victim needing oil above 100. Even in the UK anything below 80 will result in losses for deep sea drilling.

The US has a band of production costs so some will struggle some won’t but in any event the US is set to benefit hugely from low prices as it directly improves household expenditure. China will benefit, as will Europe and Japan but here other factors have to be weighed. It is never simple! What is likely is that lower oil prices will help global growth which as the IMF keep reminding us, needs all the help it can get.

Gold has been another victim of market sentiments and liquidations of late and that has weighed on the Index, but this week was much more interesting.With an impressive rally on Friday erasing all the weeks losses including a sharp down day on Wednesday it looked like a strong move but was it just a relief rally? Yes, probably on the back of the rather soft data from the US . In the context of the overall downtrend, it still is $100 dollars beneath last week’s close. The weekly chart tells the tale and shows how critically it is currently placed.

Still it really was welcome relief but certainly not a sign of trend change. Chinese demand has dried up as well as sentiment factors making for a hard climate for gold bulls to find the traction they need.

When considering the long term trend in commodities, the two pairs to watch for shorts remain to be AUD/USD, NZD/USD, and longs in the USD/CAD

This Week with the Greenback.

Well on Friday you would think from the reactions and the media that the US recovery might be falling apart, but the truth of the data was that unemployment numbers actually improved and jobs were added even if below the number expected for now 49 straight months.

Well on Friday you would think from the reactions and the media that the US recovery might be falling apart, but the truth of the data was that unemployment numbers actually improved and jobs were added even if below the number expected for now 49 straight months.

That hasn’t been seen since the thirties.

It is so important to eliminate the noise and ignore the distractions that big days like the NFP results can cause and stick to the plan.

Nothing has really changed in the mid to long term picture. It just serves to provide opportunities (we hope) in the coming week to resume buying positions on the USD. Remember also the midterms put the republicans back in control of the senate and when it comes to replacing FOMC members they will oppose the doves and support the hawks, and it is traditionally a spur to the equity markets. Statistically the S&P has prospered well in the year following mid term elections whoever is in control, so no sign of policy change and dollar strengthening going off course for some time to come, subject always to world events. It never pays to be complacent or to make assumptions.

Eurozone Resisting Still

The ECB met this week, more rhetoric and further liquidation from Mr. Draghi which still didn’t satisfy the QE lobby, and he talked of unanimity which only exists as far as it goes and certainly does not exist for the kind of QE that may be required to avoid the deflationary spiral.

Germany stands defiant. At least half of the zone is not growing and Germany itself fell short of expectations in both factory orders and industrial production. The European Commission had this to say, “ The longer the recovery in the EU remains weak the less convincing becomes the argument that this is a typical pattern to be experienced following a deep financial and monetary crisis” There are even rumours now growing of those questioning Mr. Draghi’s ability to lead.

News from the UK

The data has been mixed of late, not depressing but disappointing enough to confirm a slow down in the pick-up!

Not surprisingly the BOE kept the rate on hold.

Shafik, the deputy governor reported ’no significant evidence of upward pressure’ Neat.

Expectations for a rate rise have been delayed to at least the 3rd quarter of 2015, and while that is acknowledged it is still true to say that the British economy is still on a recovery path even if fragile. Like the US it is vulnerable to a deteriorating Eurozone and this will keep reigns on the economic growth of these two major economies. With all that in mind, cross pairs should offer some buying options for the GBP, especially where the commodity currencies are concerned.

Concluding comments

‘Keep your powder dry’ springs to mind, in these extraordinary times of world unrest and over-manipulated markets. That doesn’t mean no trading, quite the contrary, opportunities abound but be selective and stay informed. The FOMC news was not great in terms of expectation but jobs are being added and the direction is the same, Don’t be distracted by one day’s noise and volatility . Keep the bigger picture in mind when you are making long term decisions and make those decisions to create a structure around which you can take trades with confidence. That is the profitable and professional way.

I will be back next week with another round-up of events.

Judith Waker

0 Comments