What, you may ask happens when a circle is broken, the symbol of never ending unity? This was the intended design and concept of the European Union and indeed of the European Monetary Alliance…The Eurozone, incorporated into the flag by the Council of Europe in 1955.

What, you may ask happens when a circle is broken, the symbol of never ending unity? This was the intended design and concept of the European Union and indeed of the European Monetary Alliance…The Eurozone, incorporated into the flag by the Council of Europe in 1955.

We recall the more recent words of the president of the ECB, Mario Draghi, ‘Europe’s single currency is irrevocable’.

So what now? Impasse has been reached, the Greeks unable to agree to conditions which they , and many economists believe, would bring them a continuing debt spiral from which they will never recover with no optimism of improving economics as austerity measures will be escalated by the Troika.

The decision by the government this weekend is to go back to the public by referendum to decide whether or not to accept the bailout conditions. As the Greek finance minister reminded us there are no provisions for exit from the Eurozone and the Euro currency.

Extension was denied at the weekend and and then Sunday the news came of enforced bank closure which sure enough started on Monday morning. That is likely to last until after the referendum. Varafoukis in a public address Sunday, stated that this refusal of the Euro-group to agree the extension will ‘damage the credibility of the Eurogroup as a democratic union of partner States’

Last week has also witnessed some grave geopolitical events which as we know from the past can easily disturb the sentiment of the market and cause risk aversion. The recent atrocities in Tunisia, Kuwait and France only serve to remind us just how fragile our world is and just how exposed we are to politics and international tensions.

Global Macro; A Rock and a Hard Place

It is clear from the decision that the Greek Government has made that the choice discussed last week between austerity and bankruptcy is really an impossible one to make without a further mandate from the people.

This situation is unprecedented, un-chartered territory and impossible to predict the outcome except as we have seen from Sunday’s open we can expect plenty of volatility. Unless the extension is re-thought, that is where we are with a payment to the IMF now due.

Since there is no exit mechanism the more appropriately called Grex-accident will open up a can of worms for the Euro group with the possibility of the peripheral politics coming into play. With elections in Portugal in near sight, the timing is not good for the Eurozone.

The integrity of the EU is at stake and only in the fragile beginnings of economic recovery. They too have manoeuvred themselves into the proverbial rock and a hard place. Such is the cost of dual game of brinkmanship.

Politics aside (if that were only possible!) what are the ramifications for the market and the trading community? There are two aspects. Firstly, and it was clear last week from the thin volumes and the market action that many are positioning and awaiting the outcome, so to trade any euro pair is a big-stake risk. The Euro gapped down and interseting came back to the same place. Speculation and the hope of a deal will keep this choppy athough today the ECB said it will not consider any more proposals until after the referendum.

Secondly and more importantly, risk appetite is changing. This is not conclusive, yet, but is and will be an integral part of our trading plans going forward into this unknown environment. We have witnessed what seems to be a relentless risk averse trend in the S and P for four years. But now what? And how can we assess, as assess we must, what the current sentiment is and how to monitor the shifts?

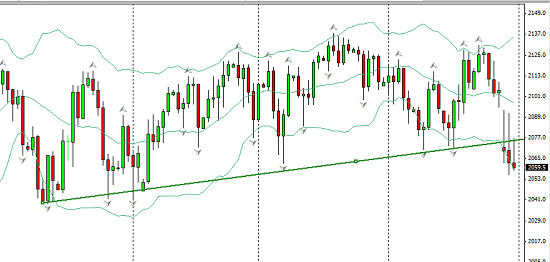

Global Macro ;The Evidence of Risk Aversion 1. S and P

This is the rally seen on a weekly perspective;

Interesting to analyse this on a daily basis. It was riding high following the rally the week before, until US data hit the wire on Wednesday . This as a result of data which brought the final (annualised) GDP right in on the expected number. This was an important number bearing in mind the dovishness of the last FOMC and maybe serving the opinion that rate hikes are still a possibility in September. Then again the uncertainties in the Eurozone may have played their part.The index closed down on the week, but not a bearish weekly candle and nothing showing at the week’s end of trading to rattle the nerves.

This all changed Monday morning,

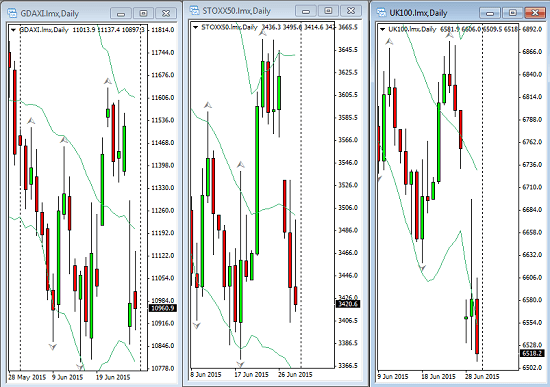

2.European Equities

The Dax and the Eurstoxx 50 both saw gains last week that were not indicative of any risk aversion or of Grexit.

As a commentary it should be pointed out that there was a fair bit of optimism in the markets during the last week, that a deal would be struck but that has all changed and we will have to see the initial outcome on Sunday opening. And it is not over yet but the fall out is obvious:

3.Chinese equities

A daily limit down on Friday was enough to cause global concern into this week . After a nasty week last week the Shanghai index lost 7.4% in one day and 12% over five sessions. I did talk of bubbles two weeks ago and this was looking less like a correction. Another limit down on Monday and we left correction territory. China of course effects the commodity currencies but it is also sends a shiver through the global economic community.

The equity boom is hard to figure with little in the way fundamentally behind it and we all know what happens when structures are built on sand. This is a market that could start a domino risk aversion trend and is a major factor in the way sentiment will be assessed inside the market in the days and maybe weeks ahead.

4. The Bond market

Another example of resilience last week, in terms of risk tolerance as Bonds continued to sell. That changed too on Monday

In the US, 10yr note yield looks like this;

5. AUDJPY and the JPY Another measure of fear. Very neatly ranging for some time and with a down bias it blew through that on Monday

The JPY will strengthen in risk averse conditions . Definitely one to watch and trade should the sentiment shift in that direction.

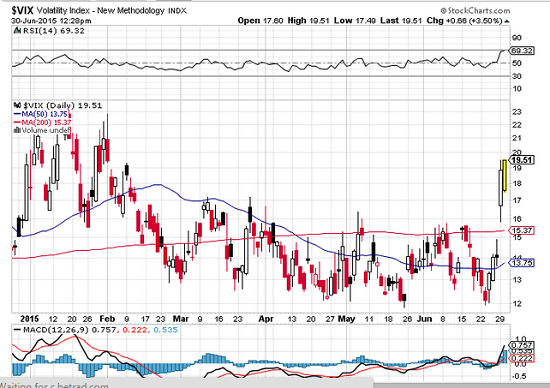

6. Volatility indexes.

These must be monitored for sentiment, especially the VIX, here is the drama as seen in the ‘fear index’ of the S and P

;7. Emerging Markets Known to do well when risk appetite is high.The opposite is true when sentiment becomes risk averse. I am focused on longs in the USDSGD.

The Summary

We know have to watch for signs of follow through. A change of mind in Europe will affect sentiment although even if we go that direction, and it seems unlikely, then it may be shrt lived with the Chinese economy to worry about. The bias would lean in the direction of sentiment shifting further towards risk aversion simply because of the geopolitical uncertainty we have at present. Add this the fact that low yields have inevitably extended the risk profile as returns are sought in ever diminishing places. All these factors have to be monitored on a daily basis and we will soon see what effect the weekend’s events will have on the market emotions. One thing is sure, opportunities will shift as sentiment does.

Global Macro ; A brief Survey of Monetary Policy Standing

Having established that much depends on sentiment here is a brief look at policy issues and standing.

Commodity currencies are all weakened with Chinese difficulties.

The Aussie Economy is an obvious weak point and Mr. Stevens from the RBA has long held the view that it should be weaker to support a recovery. The New Zealand economy has simillar problems including a weak dairy industry and a bleak RBNZ outlook.

There is also the ‘oil’ factor which will continue to weigh on these currencies especially the CAD, which admittedly has shown recent strength compared to the AUD and the NZD. Monitor the Oil market for this one. Oil has closed down and looks a little precarious, although some improvement;

GBP. Confused somewhat by DR, Carney with his ‘jolt’ tactics, there is a degree of improvement in the UK economy and some argue that rate hikes are very close. They are certainly better placed on the policy curve and thus ahead of the pack with the US in policy terms and in comparative terms, but beware of rhetoric and the Greek situation . Bias is long except against the USD.

USD Is somewhat eclipsed news wise by the EZ but speculation will continue over rate hikes after the GDP result and if sentiment does shift this is a safe haven as well as a the most positive bet for the earliest rate hike. This is another big news week ahead for the US data and we all know how important that will be.

The Week Ahead

Wednesday, CNY manufacturing PMI…This will carry significance globally. , GBP manufacturing PMI, important for rate hike speculation. US ISM PMI is major for the US as is ADP NOn farm as it carries clues for Thursdays NFP (a day earlier because of the July 4th long weekend. Thursday NFP…huge! Also GBP construction, Aussie trade balance

Friday Aussie retail sales (indication of inflation) and GBP services PMI (important as service industry factors large in the UK GDP.,

Even without the Eurozone crises it is a significant news week and plenty to be aware of both for dangers and opportunities!

The calender events and the news that may come out of Europe in the next few days and of course NFP will all factor in the assesment of market risk appetite.

The calender events and the news that may come out of Europe in the next few days and of course NFP will all factor in the assesment of market risk appetite.

Sentiment watch in the aftermath of Chinese and Greek issues is the key to setting the tone going forward.

To monitor what the market is thinking will reap its rewards and provide it’s potential.

In the meantime I will leave you with a little Aristotle (irony intended) …’Democracy is where the indigent and not the men of property are the rulers.’

Just saying.

Judith Waker

0 Comments