Another week of mixed data, mixed signals and mixed messages. Draghi now adopting the Yellen habit of ‘something for everyone’,the USD data continuing to soften and undermining the chance now of even a September hike and the Bond market continuing its sell-off although calming as the week progressed.

There is still little in the way of clarity and any kind of a prediction has joined the ranks of guesswork. The task of the trader is to increase probability. That task has become extremely difficult.

Search for pips; The Euro ; Rally or short squeeze?

Last week it was clear that something other than inflation promises were behind the sell off in the German Bund market. It continued on this week pushing the yields further before pulling back at the end of the week. There is little doubt that optimism is returning with growth in the Eurozone starting to show.

Last week it was clear that something other than inflation promises were behind the sell off in the German Bund market. It continued on this week pushing the yields further before pulling back at the end of the week. There is little doubt that optimism is returning with growth in the Eurozone starting to show.

Mr. Draghi indeed acknowledged it as much and took credit for it. He had two distinct warnings. The first was against risk taking with the amount of cheap credit available and the other was the call again for fiscal restricting across the zone to make the policies even more ‘potent’

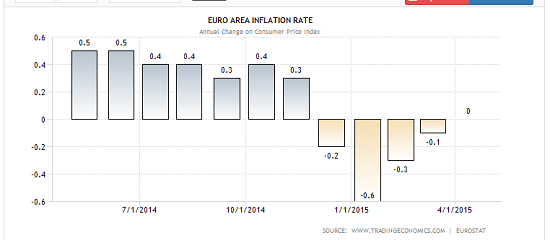

The Euro continued its rally to close out the week 1.1446, but it is the consensus view among analysts that it is a fragile rally and that there is a way to go before recovery is in any way reliable, as Draghi himself put it, ‘while we have seen a substantial effect of our measures on asset prices and economic confidence, what ultimately matters is that we see an equivalent effect on investment, consumption and inflation’ What he is looking for is clear… ‘a sustained adjustment in the path of inflation’. Here it should be noted that although there has been a pic up we cannot lose sight of the fact that the last month registered a zero up from -1. This is an improvement for sure but zero is still zero so Draghi is right to be cautious.GDP growth also missed the number in the EZ as a whole and in Germany, while France and Italy moved ahead. Chart courtesy of tradingeconomics.com;

Greece presents another confusing array of data and conflicting ’news’ . Speculation is rife. While Draghi was heard to utter the ‘irrevocable’ word again in reference to Eurozone membership, Greece continues to head towards the brink and Tsipras confirms there are limits beyond which he will not go and that includes paying public salaries and pensions.

Greece presents another confusing array of data and conflicting ’news’ . Speculation is rife. While Draghi was heard to utter the ‘irrevocable’ word again in reference to Eurozone membership, Greece continues to head towards the brink and Tsipras confirms there are limits beyond which he will not go and that includes paying public salaries and pensions.

The situation is fragile to say the least but it is clear that an agreement is needed in the next few weeks. What seems to be a crowning irony is that despite the recession as judged by GDP (which in fact was better month on month) , Greece actually recorded a surplus this month from reducing spending and increasing tax revenue. This was quitely dealt with by the press. Crunch time is approaching and even if you accept the argument that the Eurozone is pulling out of recession and that the rally has legs of its own, the Greek situation continues to heighten the vulnerability and the sustainability of current Euro ‘strength’.

Much has been made in the press of the meteoric rise of the German yield but a reality check here, (as with inflation numbers above for the EZ) shows the German yield at 0.7 and the US equivalent at 2.2

The distortions at play and the fund positioning triggering an impressive short squeeze may have some distance yet to run but the outlook for the Euro is still to devalue further, especially if Draghi sticks to his plan of QE follow through. This does not have to be related to perceived US weakness. There are quite enough factors involved behind this particular currency shift to not even take that aspect into account.

The search for Pips; The USD, Correction or Trend Change?

The soft data continues to make an appearance. This last week The USD index pulled back further;

The Sand P forged ahead with other US equity markets. Here it is on a daily chart;

It was accepted by the market that the greenback had gone too far too fast and a correction therefore has not been a surprise. It doesn’t take much to trigger such a unstable high. As it is, first quarter GDP was a real concern, and add to that this last week PPI Industrial production , retail and core retail and the empire state manufacturing all missed their expected numbers. Only unemployment kept the hopes alive as numbers dropped again this week. Forecasts have now lowered second quarter estimates. The 10 year yield pulled back as US treasuries advanced.

There is still the prospect of a rate rise, factored in now in December but a real expectation now in the market that whilst this still registers as a USD correction it is not over yet. This week sees the publication of the FOMC minutes which once again , without the forward guidance of last year, will at least lay some clues. Any comments or lowered forecasts for Q2 GDP or inflation would be a shift worth noting and a definite for pushing the rate hike further out. Again. Watching to see how important they regard the soft data and what they will be looking for and focusing on going forward is the best we can hope for. There is still the opportunity to weigh dovishness and hawkishness and language tone, and as always this is full of speculative potential! Be on your guard on Wednesday.

Japenese Abenomics

The Japanese will announce their rate statement on Friday. Another one to watch as speculation grows on more stimulus, an idea the BOJ has rejected ahead of the meeting citing inflation pick up as promising. It may well firm up although the chance of further intervention is still high and the tone has been dovish. The statement will thus again be important .

Commodities and the Chinese effect.

Aluminium, a different component of the index this week was halted in a rally as the Chinese output went up to swell supply. For now the commodity currencies have enjoyed a rally across the board on dollar weakness, oil strength and a recovery from lows in the commodity index. The index is now consolidating after what has to be described at present as a relief

The oil market was volatile this week and resisted its high point in the recent rally;

US inventories were down this week but it failed to reflect in the chart. Many issues surrounding oil leave the next move uncertain. Not only is this market affected by US production numbers and geopolitical risks but it is also a large factor in hedge fund positioning , and thus there is potential here for some moves that can be completely unpredictable as we have seen in the bond market.

Not surprisingly, with its economy sensitive to the gyrations of the oil market, the Canadian dollar also sits on the chart in a key area. It is the bottom of a range and a 200 EMA. Close monitoring once again required of both the oil market and the USD index,

Market Mood Swings

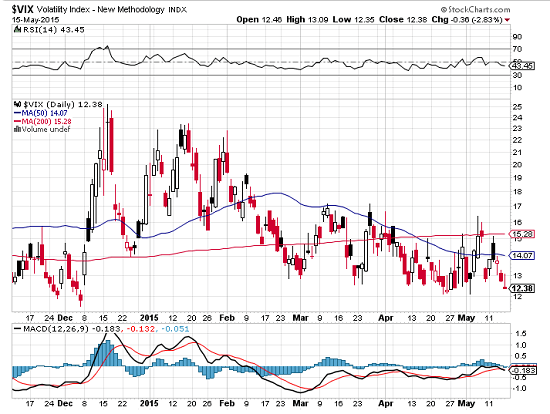

The vix this week dropped to a low, the S and P fear factor dowsed as equities moved up again; chart courtesy of stockcharts.com

Elsewhere, the recent volatility seen in the German bond market, among others, stands in sharp contrast as does the Forex volatility.

In the UK, post election hype has died down but there may be some more room to move ahead. Carney speaks on Friday and the week will include retail stats. This is a big number for the GBP and it has not been all bad news. There is a possibility that the rally in the GBPUSD could continue higher and current USD ‘weakness’ may well give it some room early in the week. We are approaching some interesting levels but of course Carney language as with all central banks will have a significant effect on the short-term outlook. This is a weekly chart of the GBPUSD;

As for the EURGBP, this fundamentally is a short but again it may need a higher level for a short or the EUR to cool off;

Draghi speaks again, this time in a Euro forum and of course we have to stay alert to the Greek news feed which has the potential to cause both volatility and violent swings. The Eurozone has become the mood swing capital!

PMI in the EZ also on Thursday.

The New Zealand economy was boosted last week by retail sales numbers coming in at 2.7 against 1.6. This coming week sees inflation expectations. If that too does well we cam expect some strengthening in the Kiwi.

Canadian retail numbers are on Friday and As discussed earlier the BOJ meeting is on Friday.

There are lots of inflation clues in the data and news ahead of us this week. We need all the clues we can find to navigate the mudded water the market is currently wading through.

Hype, spin tone language and speculation all exert their effects on sentiment, which can easily outweigh obvious underlying fundamentals and should be treated with care and respect. Right now they are changing on a weekly and sometimes daily basis.

Patience and Timing

With the flow of capital out of European Bonds and equities and flows into US equities continuing apace, the environment still favours a return , eventually to dollar strength even if we will not see it for a while.

With the flow of capital out of European Bonds and equities and flows into US equities continuing apace, the environment still favours a return , eventually to dollar strength even if we will not see it for a while.

Confusion increases, analysts are divided, clarity has diminished. Also bear in mind it is not a coincidence that many of the charts we monitor are at critical technical points. Maybe soon there will be a return to some sort of ‘normailty’ and the clarity will start to return. For now the watch continues.

Patience and timing are everything. If you are uncomfortable as a contrarian wait for evidence of turn round in the Euro and the commodity currencies, for the USD to pick up the rally. Wait until the writing is on the wall, many a pro has been wrong-footed in the past few weeks. Better to be on the back foot than the wrong foot!

Judith Waker.

0 Comments