The focus on last week news flow was inevitably on Friday’s NFP and it did not disappoint. We also heard a warning from Draghi at his ECB meeting on Wednesday, of continuing volatility and no intentions to scale back the QE program despite renewed optimism on the back of recent data.

The Bond rout continued on both sides of the Atlantic pushing up yields.

By the weekend tensions between Greece and it’s creditors were growing and continued into the weekend with Juncker getting involved and expressing disappointment with the Greek Prime Minister, Alexis Tsipras.

Volatility can be expected to continue as the trading environment grapples with shifting paradigms of market inter-relationships. Staying aware of the fundamentals that drive the markets and how they directly affect trader sentiment seems to have stepped up a gear in the last month.

NFP and Forex Sentiment

Starting at the end of the week with the NFP data, we saw robust numbers as 280000 jobs were created easily beating the estimate of 222000. Not only creation but wage growth hit a two year high. The press played down the IMF’s Christine Lagarde’s comments earlier in the week that the US should not raise rates until next year as she appeared to enter FOMC territory and was notified very clearly by the US treasury market that they are nor likely to heed the advice.

There may now be a rise of a quarter percent by year end in the rates. It could even be as early as September and that can fire another round of speculation. There is of course another FOMC meeting later this month at its importance cannot be underestimated.

The nearness of a rate hike and the volatility in the bond markets with yields advancing as they are, provide the ingredients for nervousness in the US equity markets which by anyone’s analysis are overvalued. The trend in the S and P has been thought to be vulnerable for about 6 years so it is never wise to call a top! What we can do however is stay on our guard as far as sentiment is concerned on a weekly (sometimes daily) basis to see how the current environment affects equities generally and to watch for any on-set of risk appetite changing towards risk aversion:

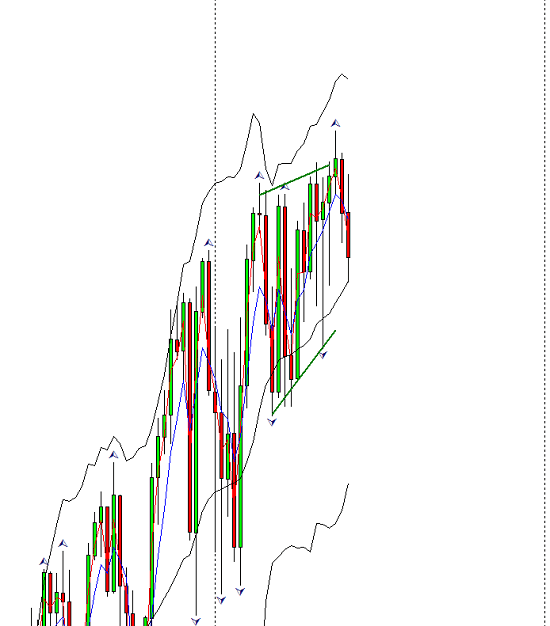

Too early to detect risk appetite changing or a trend change, it seems fair to suggest that the last two weeks trading in the S and P discloses at least some anxiety. These are the weekly candles;

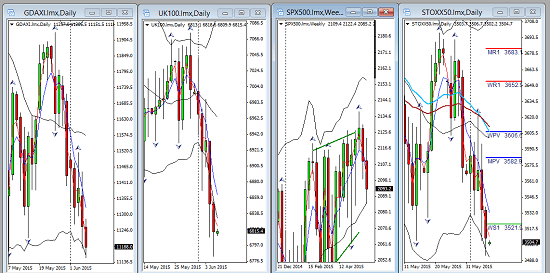

Here is a global equity overview…all pretty negative last week;

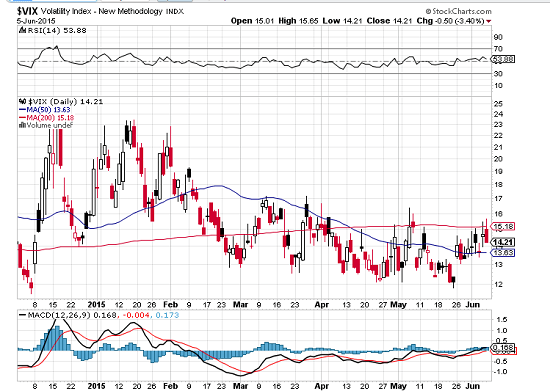

The ViX is in an interesting place, chart courtesy of stockcharts.com

It should be noted that levels here are yet to advance to ‘volatile’ levels but this is S and P volatility and in no way detracts from what we are experiencing in other markets. None the less it is an important indicator of the more broad assessment of risk appetite.

Draghi; Hawk or dove?

The Hawk;

‘Our monetary policy measures have contributed to a broad-based easing in financial conditions, a recovery in inflation expectations and more favourable borrowing conditions for firms and households …the full implementation of all our monetary policy measures will provide the necessary support to the euro area economy, lead to a sustained return of inflation rates towards levels below but close to 2%’

The Dove

‘(we) need to maintain a steady monetary policy course, firmly implementing the Governing Council’s monetary policy decisions.’ The QE program will continue for the full term intended (September 2016)

Rates of course remained unchanged and Mr. Draghi warned of volatility ahead especially in the bond markets which promptly proved him right!

What is clear whether Draghi is a hawk or a dove is that the monetary policy divergence between the EZ and the US just widened further.

The other explosive issue and potentially one inflicting grave harm to the European Union, is the Greek situation. This week the Greek government ‘bundled’ a payment to the IMF. A rare move but a ‘legal’ one deferring payment on a technicality. But the implications are indeed grave.

The other explosive issue and potentially one inflicting grave harm to the European Union, is the Greek situation. This week the Greek government ‘bundled’ a payment to the IMF. A rare move but a ‘legal’ one deferring payment on a technicality. But the implications are indeed grave.

At the group of Seven summit this weekend, the EU commission president Juncker stated ‘ I don’t have a personal problem with Tsipras, but friendship, in order to maintain it, has to observe some minimal rules.’ He refused to take the Greek PM’s telephone call in the absence of more proposals.

Friendship may be an exaggeration from the outset but there is undoubtedly frustration on both sides and compromise seems to get less likely as the days pass. Another volatility ticket and extremely unpredictable. Irremovable object coming up against irresistible force comes to mind. A veritable can of worms for Draghi after such promising data should the dreaded Grexit come to pass.

Commodity Currencies;

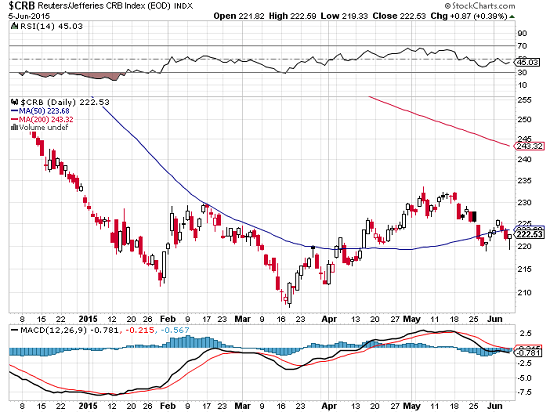

Commodities continue to range; chart courtesy of stockcharts.com

In Australia a shock trade deficit started a sell off which erased gains earlier in the week. US non farm data will likely bring further weakness. Sentiment is negative and it is well documented that Governor Stephens wants a cheaper Aussie dollar and the rally against the Greenback which began in April has almost been eradicated.

The Australian 10 year yield fell back slightly to 3.039 in Friday’s trading after a strong monthly move up.

There is a speech from Mr Stevens on Wednesday which will be critical and Chinese data on Monday.

The Kiwi dollar is also braced for a cut in interest rates and the decision will be on Wednesday. It may well be that any rate cut will be delayed until later in the year, so again language will be an important factor. The yield advanced to 3.862 0n Friday

The State of the Oil market.

The Opec meeting left production targets unchanged. The war between the US and Saudi Arabia goes on. So who is winning?

The Opec meeting left production targets unchanged. The war between the US and Saudi Arabia goes on. So who is winning?

The US fracking rig count has been vastly reduced but production numbers are still sound and despite Opec attempts to undermine their output, they may yet still take the pole position in oil supply.

The Saudis whom front Opec have another problem. Iran, close to a nuclear deal are likely to go to maximum production and add to the ever bulging supply. Few believe that the oil market can sustain a rally.

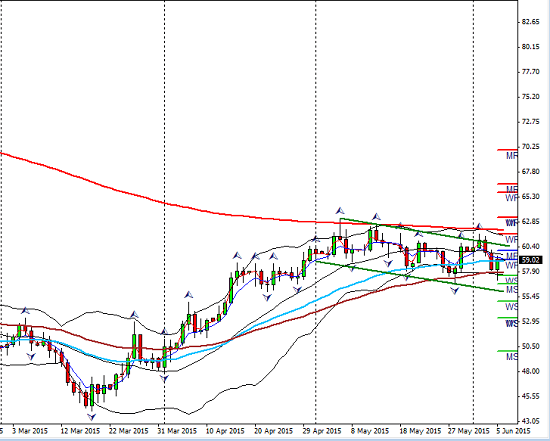

Even if it makes an attempt to advance the US oil rigs will simply restart thus increasing supply again. Technically oil continues in its downward facing channell and finds itself wedged between a daily 55 and 200 EMA

The short term and long term outlook for the commodity currencies is affected but no more so than the CAD. The medium term downward pressure is very evident, though it should be said that Canadian data has been strong of late. It remains vulnerable to the ups and downs of the Oil market.

The winners…the importer economies; the US, the UK, China, India. As for sentiment it is volatile so another market to watch carefully for signs of negativity. The BP boss called this a ’shale revolution’ and it is clear that global strengths have shifted and are unlikely to ever be the same.

The British Scene

Mixed signals as we have come to expect with the economy showing signs of improvement with consumer spending, suffered a disappointment last week with PMI including the services sector which is bound to cause concern. With strength across the pond in the US, there may be further weakening ahead for the GBP.

Dr. Carney speaks and as always policy and accompanying language will be vital to gauge the intentions of the BOE and its effect on trader’s sentiment.

Japan’s ‘Growth Orbit’

Shinzo Abe was very upbeat at the G7 meeting this weekend stating that Japan’s economy is in a ‘growth orbit’ The market is not yet convinced and despite his comments the sentiment continues to be negative this confirmed in the futures market, (the COTT report) and whilst not a major indicator for the Forex it does hold important implications on how sentiment is setting up.

Sentiment Catalysts in The Week Ahead

To stay ahead of the curve, attention has to be paid to the trader’s state of mind. Sentiment is key and the possibilities of risk appetite changing also cannot be discounted. It requires us all to stay aware and read the clues correctly. The week ahead holds many opportunities for sentiment to react;

Monday; Chinese Trade balance ( important for the AUD),

G7 continues

Tuesday, Aussie business confidence and Chinese CPI

Wednesday, RBA’s Stevens speaks GBP manuf. production and Carney also speaking. Today also NZD rate decision. All ears on that one!

Thursday, AUD employment numbers and Chinese Industrial production

USD unemployment figuresand retail sales.

Friday USD PPI and consumer sentiment

Just because NFP is out of the way does not mean any complacency on our part and this week contains plenty of catalysts for changing directions.. Mr Draghi warned of volatility and few doubt the verity of that statement. Remember volatility is ultimately sensitive sentiment and it will mean more monitoring and more understanding. With the information and the right perspectives we will have the tools to increase our probabilities. Combined with effective and disciplined risk management we can approach our markets with confidence.

Stay tuned. Stay informed.

Judith Waker.

0 Comments