If you take the time to listen to an FOMC statement being read and simultaneously watch the financial markets react to it, not to mention the attempts by CNBC to interpret ‘on the hoof’ you will see why it is so much more comfortable to sit on the sidelines and adopt an objective stance. If you do so it can be very amusing.

Last Wednesday saw the market lean to a dovish interpretation but it was short lived and very volatile. They picked up words such as ‘soft’ exports and inflation continued to ‘run below’. Also economic conditions may…’warrant keeping federal funds rate below levels the committee view as normal’.

CNBC chipped in with such rhetoric as a ‘poker-face’ statement and ‘no smoking guns’ They thought that the implication of the statement was that time was running out for data to justify the hike. There was enough to assume that initial dovish take.

But then someone noticed a new word. Solid. That small addition had the hawks jumping , excuse the mixed metaphor! As for labour, the term under-utilisation previously described as ‘somewhat diminished’ had become simply ‘diminished’.

And there was more, declining employment , longer term inflation stable. Of course there is a difference between reaction and response, the former being a potentially expensive option when trading forex. By the time the London session opened it was clear that the US had confirmed that rate hikes are still on the table for 2015 and that September had not been ruled out.

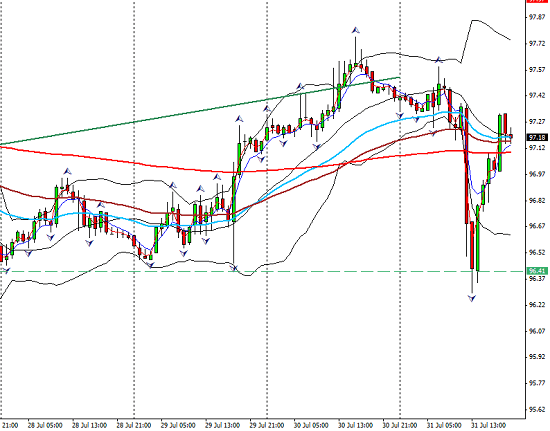

The USD Index tells the story. Shown here on a one hour chart so the volatility is defined;

Of course by Friday a relatively strong core CPI in the Eurozone and a disappointing ECI saw aggressive selling in the USD as the month closed out, though recovering into the close. Employment Cost index measures wage growth and the numbers showed the smallest increase since 1982. The Chicago PMI numbers which beat the expectation did not apparently soften the initial move.

Month end activity also enhances any selling in a currency as strong as the dollar as profits are taken off the table. The fact remains there are but two contenders for the rate hike race (still) and the divergence with the rest of the global economic playing field in policy is growing ever wider and starker.

The big catalyst in the US for the coming week is of course the NFP data.

Profit Search; Super Thursday

So called as the big day for the second contender, the BOE in the UK. Some are even beginning to discuss the possibility of the UK being the first to raise rates. Again this is a data driven decision and it has recently been assumed that the UK is following not leading its friends across the mighty pond.

The GBP has been showing more sustainable strength of late and GDP came in as expected with a 0.7% growth which was healthy enough and something of a bounce. A little research also revealed another interesting perspective. The UK GDP data has seen the 3rd longest period of consecutive quarterly growth since 1963.

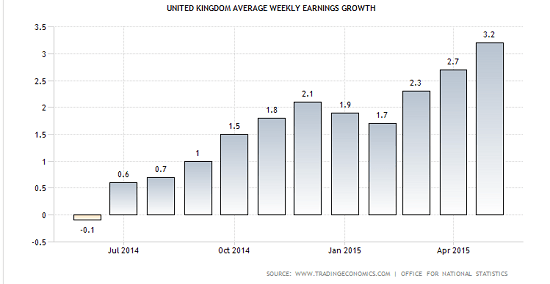

Also causing growing optimism, is wage growth; chart courtesy of tradingeconomics.com

These results and the recent rhetoric coming from the BOE have sparked the new speculation that the UK may be the ones to raise first. Super Thursday is a major catalyst. Policy meeting notes will be published as well as votes (watch for dissenters) and the QIR (quarterly inflation report). All that to be followed by Dr. Carney’s statement. There is a growing expectation of hawkishness especially as we see the Greek risk fade a little, which we may assume has been factored out to an extent from BOE policy, but as always we look to the meeting and the market sentiment towards it to set the tone for the GBP going into the summer period and beyond.

Profit Search:The Usual Suspects;

Oil and Commodities

As Iran comes back onto the Oil scene and the rig count in the US continues to rise there seems to be no respite to the oil price slide.

Commodities are in a serious bear market which will continue to exert pressure on the commodity currencies and on global economic recovery.

Gold too under continuing pressure falling over 6% in one month. Lack of wage growth on Friday in the US at least gave it some relief but the prospect of rate rises still possible by year end will mean the relief is only temporary.

Australia , suffering problems with Iron ore are also negatively affected by Gold as pressure on the Mining Industry builds relentlessly.

This is a big week for The RBA, with a rate statement Tuesday and alongside retail numbers and their trade balance

New Zealand, with dairy sector woes unabated, business confidence falling and even building permits missing a target, it is not a surprise that the RBNZ noted that ‘’every sector apart from retail now has sub-trend expectations’’ With one rate cut already the speculation mounts that another will be necessary and thus the NZD will remain under pressure and that the downtrend will continue. Wednesday gives us about stats which will be watched for signs of growing unemployment.

Canada. Fridays data did nothing to lift the economic outlook in this oil dependant nation. Another contraction in the GDP showing -0.2% missing the modest target of zero.Employment data next week here as well. The CAD continues to look increasingly bearish. It is difficult sometimes to imagine how a rally such as we have seen in the USDCAD and indeed the GBPCAD can be sustained from a technical viewpoint. Understanding the fundamentals shows us that we cannot make any assumptions on sustainability. The bucking of the USD index trend on Friday displays this relative strength and gloomy outlook for the besieged CAD

China, another 8.5% drop in the Shanghai Index, despite all the government efforts to prevent it.

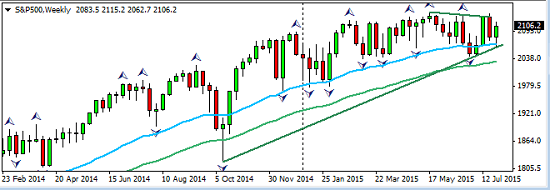

This over leveraged and manipulated market carries wit it a serious warning for increasing risk aversion . The S&P had a relatively strong week is still precarious and itself over leveraged.

The Emerging Markets are threatened not only by Chinese concerns but by a strengthening dollar and it should not be forgotten that raw materials are priced in dollars. Despite a stronger US boosting emerging market exports there seem to be too may negatives for anything to stem the bear market. The dice are loaded. Brazil, Russia, Singapore Malasia, Thailand, Poland Mexico and of course China, to name but a few.

The Question Of Risk

A continuing monitor on trader sentiment shows evidence of appetite and aversion. This is not a black and white area especially if we happen to be in transition. The Equity markets are vulnerable to the Shanghai selling. In the Eurozone Mondays losses were mostly recovered but still looking under pressure;

The Bond Market also revealed buying as the USDX sold off on Friday. In the US, the 10 year note and the rate sensitive 2 year note both advanced leaving the yields on the downside. The EURBUND saw the same as did the Gilts in the UK.

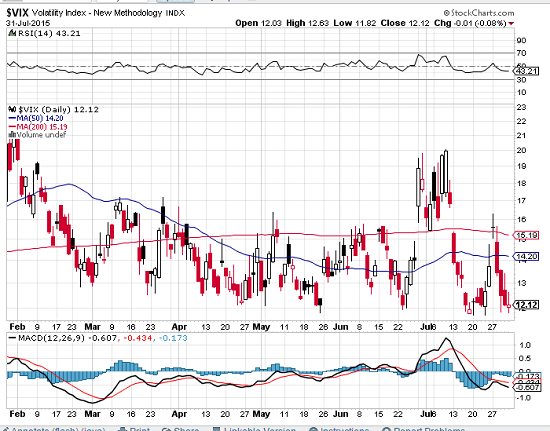

The VIX, remains at a low level and there are analysts who believe that indicates, in a contrarian way, a correction is due. Whether this be valid or not , it is certainly one to watch;

Profit Search; Review of the Week Ahead

Just to re-cap what cannot be missed in the trade plans;

Monday, GBP PMI, and US ISM PMI, AUD retail Trade Balance

Tuesday, AUD rate decision and statement, GBP, construction PMI, Dairy from NZ and their employment stats.

Wednesday, GBP Services PMI (important UK sector) ADP advanced NFP numbers, USD ISM non manuf. PMI and trade balance. AUD employment stats. CAD trade balance

Thursday, GBP super Thursday (enough said!) RBA monetary policy statement , BOJ statement on monetary policy and BOJ press conference.

Friday, NFP! Cad PMI and CAD employment stats.

Saturday (in case you haven’t had enough news….) China trade balance and CPI so beware leaving trades open on the weekend!

The Watch-List

Commodity currency weakness and GBP strength. Of course the USD is all about NFP this coming week

GBPNZD

GBPCAD

USDSGD

USDCAD

GBPAUD

AUDUSD

Timing is all about the news releases and from the list it is important not to be over weighted so 1% in either GBP or the USD. In Summer time it is probably wise to focus on just a few pairs and not over-trade.

Conclusion

August brings us the vacation month. There is the usual anticipation and thus a necessary cautionary note , of the likelihood of low volumes. At the same time there is no break for the news watchers with a massive week ahead. The effects of whipsawing can be increased with thin liquidities. What will be of most importance is how the coming week sets the tone not just for the summer period but for the second half of the year

Monetary policy and the developing polarity we have observed in the Forex will no doubt keep it’s place as a prime theme as we dare to look ahead but always always, this must be seen in the perspective of risk sentiment. Watching the behaviour of the market as a whole will assist the development of a trading edge and thus is paramount in the ever present task of enhancing our probabilities of successful trading.

Judith Waker

0 Comments