Monetary policy ping pong was the game in play last week. With only two economies with any near term hope of seeing inflation targets met, it should not be a surprise that speculation has recently grown as to who will be the first. It is a recent shift from the long held assumption that it would begin in the US. However, a combination of rhetoric and some early signs of inflationary growth led to the idea of the BOE entering the race. There is no doubt that the UK have progressed up the curve towards the US targets, and there has been notable improvements in the data to support a more upbeat outlook and indeed recent strengthening in the currency has been noted. Thus it was that market focus turned towards the words of Marc Carney and the BOE statement on Super Thursday. The other focus of the week was of course on the NFP numbers and the effect that might have on the perceptions of US policy.

Monetary policy ping pong was the game in play last week. With only two economies with any near term hope of seeing inflation targets met, it should not be a surprise that speculation has recently grown as to who will be the first. It is a recent shift from the long held assumption that it would begin in the US. However, a combination of rhetoric and some early signs of inflationary growth led to the idea of the BOE entering the race. There is no doubt that the UK have progressed up the curve towards the US targets, and there has been notable improvements in the data to support a more upbeat outlook and indeed recent strengthening in the currency has been noted. Thus it was that market focus turned towards the words of Marc Carney and the BOE statement on Super Thursday. The other focus of the week was of course on the NFP numbers and the effect that might have on the perceptions of US policy.

As we go forward into the ‘vacation’ period and the next few weeks there are two major themes and how they develop will be crucial in understanding the shifting relationships in the interconnected marketplace. Policy is the current focus and risk is the underlying current. Shifts are being observed and as they occur, they exert their own effect.

Preparing For Profit ; Markets Overview

This is the piece of the risk puzzle that needs to be constantly monitored.

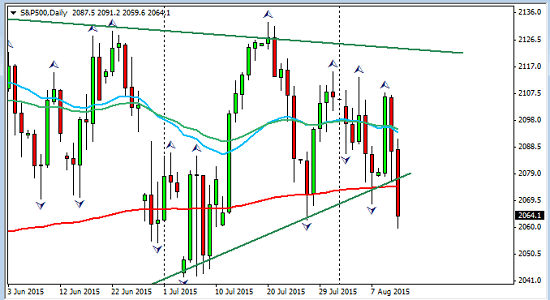

US Equities generally suffered down-moves again this week, The S&P shown here on a daily at the

and the DOW JONES now significantly below its 200 day moving average.

Equities in the Eurozone fared somewhat better but within their weekly down trends;

In the Bond market an interesting schism with bonds advancing in Europe and the UK and the US two year Treasury , which is the more sensitive to rate rises and US policy, falling with the resulting rising yield. This not surprising on the back of the NFP data.

An up week for the Shanghai but continues to look precarious as China continues to cause concern to the global recovery attempts and the dual effect of bubble burst and shrinking demand;

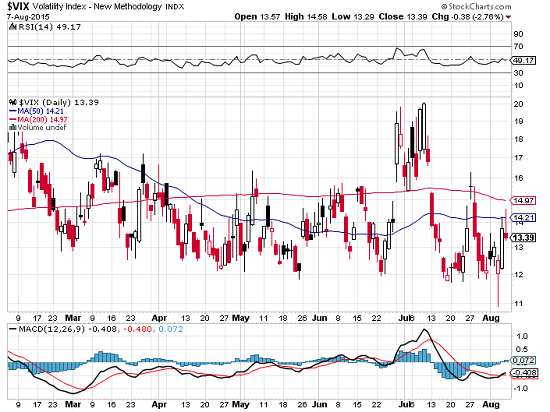

The VIX has moved up once again

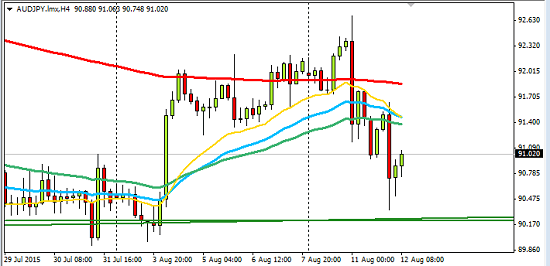

The AUDJPY as the currency pair providing a fear gauge shows another move up but below 200 daily EMA and still in its range;

Preparing For Profit; Policy Considerations

On super Thursday Marc Carney brought to an end, for now, the idea that the UK might win the rate race that has grown of late amongst the speculators. The truth is not much has changed in terms of policy, a point which he made forcefully to a journalist asking why he had changed his views expressed in the Lincoln address. He quite rightly pointed out that he has not, but what has changed is emphasis and thus perception of the market. The votes also changed with one member of the BOE wishing to vote immediately for the rate to be raised. However the rumours had grown to four dissenters and the expectations to at least two, so the result once again leant towards a dovish interpretation.

Like the US, Carney was quick to remind his listeners that the decision is data driven and to that extent it is not possible to predict the timing. Slack in the economy is diminishing, there are early signs of wage pressures returning but there are dis-inflationary headwinds, mainly caused by falls in oil and utilities. Near term inflationary forecasts have been downgraded. Another comment of importance and one to keep in mind as data unfolds is the warning from the BOE chair, that whilst they see the target being met of 2% inflation they also anticipate an overshoot and thus there is a need to control rates at 2% which will have to be incorporated into any tightening policy .

The GBP weakened against all it’s pairings as a result of the perceived ‘disappointment’.

Friday saw the NFP return numbers within expectation including a small step up in wage growth. The implication is that a September hike is still on the table. The jobless numbers fell to a seven year low and Bill Gross immediately opined that ‘September was almost certain’. The bond market didn’t reflect the same confidence.

The global challenges could still derail the September possibility, these are again dis-inflationary headwinds and the strengthening dollar is in itself another. Commodity prices and in particular oil could spell serious deflationary warnings across the global economic communities and threaten the tightening program.

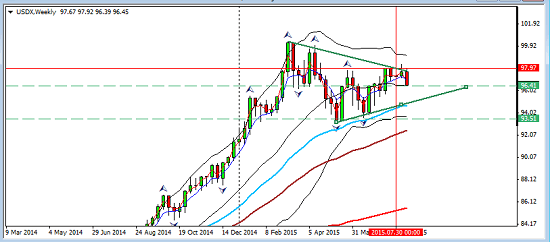

The USD index took off on the news to make 4 month high only to give back the gains and fall back into a consolidation area leaving a small gain on the week. This is a must to follow, even on a weekly chart this has got into a very tight consolidation;

The BOJ had a say also on Friday, following a minor dip in PMI and a rather disturbing drop of -2.4% in average cash earnings. Rates were held and the stimulus program continues. Kuroda sees exports weak but improving along with inflationary tends, but economists perceive something quite different with downwards pressure building on inflation.

The RBA made their own statement on Tuesday. Leaving rates unchanged they were less dovish than expected about growth with the current low rates supporting a pick up down the line. The rhetoric gave a boost to the currency and supported by data which beat expectation with retail sales coming in 0.7%, and even the -2.93B trade balance beating the estimate! This was followed on Wednesday by employment well in excess of the estimate although an increase in unemployment. All in all a strong week for the Aussie dollar. The equity market did not fare as well , however as falling commodities are making an obvious impact.

Preparing For Profit; Reality Check

Australia faces challenges relating mostly to the China effect and to the fall in commodity prices which continue downward. A CPI number from China on Sunday) slightly beating the estimate, but then China has effectively devalued their currency. Additionally any data from the USA could again upset the recent up moves. The bias remains down and the Aussie dollar is still in its range.

The AUD has on many occasions surprised on the upside with it’s resilience.

The USA has re-enforced its place at the head of the rate hike queue so data ahead is critical. It has been noted that the market are still behind the projections of the FOMC thus giving room for further upside potential. this could of course all change if the US decide to leave rates in view of global deflationary concerns. Timing as usual is everything as is the appropriate beneficial pairings.

The commodity currencies and the emerging markets are still facing major deflationary threats from China and oil and commodity declines in general.

Another down week in the crude marketbrought it it to a major support level which has now broken

Brent also fell significantly below $50 per barrel.

The GBP is still in the stronger camp for recovery (group of two!) and despite the dovish twist we have just seen, scope is there on data releases that beat expectation. It still has interest against the commodity set, but beware the extent of the current pullback and the potential of data to move the market in either direction. We are seeing wage pressure on the up so all is not over for the GBP if you can wait and watch!

NZD is struggling with dairy prices amongst other issues with Fonterra now having to offer interest free loans and downgrading the already too low forecasts. This is a big loss to the economy and holds a gloomy picture ahead. There are multiple geopolitical issues that threaten exports.

The environment this week will call for patience and for pullbacks to be given room. Eventually there may be some interesting opportunities; but it may take considerable time,

USDSGD

USDJPY

USDCAD

GBPCAD

NZDUSD

AUDJPY (if risk environment justifies it)

The Catalysts

.

GBP, average earnings on Wednesday together with the claimant count. This will assist measuring the pull back.

The USD has important once again. Retail and core retail on Wednesday and unemployment claims as usual. PPI and consumer sentiment Friday.

NZD retail numbers on Thursday afternoon

In the EZ on Thursday French and German CPI , EZ monetary minutes; preliminary GDP from France and Germany and flash GDP from the EZ on Friday with final CPI

The first day of trading reveals the initial trader sentiment following the big news from the two world leading economies and also now the market must digest the Chinese decision. Both the Fed and the BOE lean ever more on continuing data which will hold the potential drivers to enhance or end those corrections. The break of the USD index balance is key to understanding the timing as is the monitoring of the current level of support in the oil market. We have to also consider the usual August environment of very thin volumes that call for careful handling.

This is a month to monitor developments in policy and how they may affect the markets. There are periods when good opportunities are worth waiting a while for. This may be one of them.

Judith Waker

If you would like to learn how to trade like a pro check out our $1 offer by clicking on the banner below

0 Comments