Another strong week for the Theory Into Practice Team brought us 445 pips, How was it achieved? We start with analysis, all revealed in this blog, …without question the most important factor in our experience is the understanding of what is driving the market and why. So here is a review of last week’s global macro issues and what is ahead this week than can seriously affect your trading health!

Another strong week for the Theory Into Practice Team brought us 445 pips, How was it achieved? We start with analysis, all revealed in this blog, …without question the most important factor in our experience is the understanding of what is driving the market and why. So here is a review of last week’s global macro issues and what is ahead this week than can seriously affect your trading health!

The Week In Review

Equities failed their assualt on the highs in the week past carrying the implication that the risk factor maybe becoming a concern. There is a fine balance between risk and the ever increasing need to find yield especially as funds accrue losses in parts of their portfolio that contain developing markets, gold and falling equity sectors such as energy.

What has manifested in the last week were signs of increasing nervousness. Chinese sinking PMI added to the mood, commodities slid further into what can only be described a a major bear market. Greece and the Eurozone start negotiations on Monday. Again. The IMF have weighed in with their own agenda.

Meanwhile, focus itensifies on the FOMC with a meeting in the week ahead. Oil rests precariously on a monthly low which very few have any faith that it will support it for long, and with all commodities in apparent freefall, the Australian dollar fell to a four year low against the USD the CAD an eleven year low, copper a six year low, gold a five year low. The list goes on.

That leaves us in simple terms with two focal points which cannot be ignored. Sentiment and FOMC policy.

Pips and Insights…Back In the USA

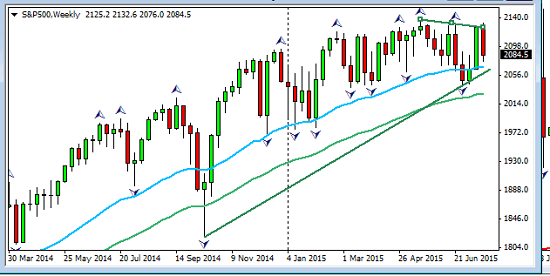

With the inevitable consequence of despondent sentiment, the question for the week ahead will centre around whether the FOMC, upon whose words the trading community are now entirely focused, will reflect this mood and dilute the recent hawkishness. US equities have faltered following the upbeat moves of the previous weeks, the S&P now in a fairly tight weekly range. Any move by the FED in a hawkish direction can send this in a downwards direction. The perspective on the weekly is defining a down slope and what needs watching;

There are other factors also, earnings season is seeing falling revenues and missed targets. We are already aware of the super high valuations. Big names and big losses, Biogen and Capital One. The three major exchanges, all lost ground.

The Fed and the BOE echoing their every move on the other side of the pond are the only economies looking to raise rates, and divergence with the other major economies around the globe has become bi-polar. This paradoxically may cause the FOMC to reassess their policy as the rest of the world seems unable to rid themselves of the spectre of deflation. Unmployment statistics beat the estimate comfortably to say the least, with 255K against 279K but is it enough to maintain the speculation for a 2015 hike?

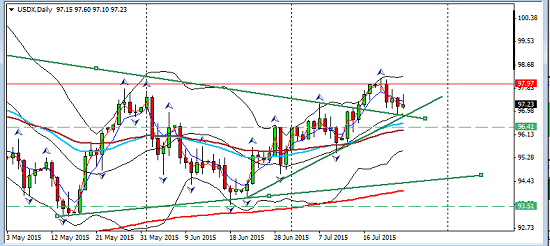

The USD index has consolidated into a tight balance, so this week’s news is critical to see which side it breaks.

Pips and Insights…Sentiment Watch

At times sentiment has long periods of stability, risk appetite or aversion can settle in for a period of months. But much like overextended rallies, there comes a time when instability causes sentiment to shift on a weekly and even daily basis. We have seen evidence of this in the last few months, and certainly since the Swiss debacle back in January.

Under the Sentiment umbrella now, its a constant monitor of equities, bonds, oil, commodities generally, Chinese stats and politics and of course the success or failure of Greek negotiations. Its much like anticipating the liquid ground of an earthquake, when the pundits warn of it’s imminence. Anyone living on the Hayward fault will know just what I mean!

There are many analysts currently considering China as the biggest threat to global economic stability. This week saw the Caixin preliminary PMI falling short by some way of the expected target of 49.7, coming in at 48.32 and well into contracting territory.

Weaker foreign demand was cited. It seems further that rates cuts which are obviously anticipated to proceed into the third quarter, are not being passed on from commercial banks. Corporate earnings cannot grow under these circumstances even with extra liquidity at a government level.

Amongst the Manufacturing data, Chinese shipbuilding orders were 72.6% down in the first half of the year. The outlook is weaker as it is for the commodity currencies.

Oil continues it’s own downpath. with opec increasing output alongside the US adding to their inventories again this week.

And then there is Iran to slip into the new equation.

Pips and Insights…Strong V. Weak

The the UK the BOE of late has made a hawkish stir, firing speculation of a rate rise possibly this year. The data didn’t follow through with the all important inflationary indication of retail sales missing the expectation with a -0.2%. This had chief economist Haldane from the BOE putting the brakes on a rate hike expectation looking at New Zealand and Canadian issues as warning signs. There are plenty closer to home but we can expect the GBP like its sister currency in the US to be increasingly data driven.

The the UK the BOE of late has made a hawkish stir, firing speculation of a rate rise possibly this year. The data didn’t follow through with the all important inflationary indication of retail sales missing the expectation with a -0.2%. This had chief economist Haldane from the BOE putting the brakes on a rate hike expectation looking at New Zealand and Canadian issues as warning signs. There are plenty closer to home but we can expect the GBP like its sister currency in the US to be increasingly data driven.

There is GDP on Tuesday which shed some more light and is an important potential catalyst. The GBP is still strong against the commodity currencies but may see some pullbacks from its recent euphoric moves.

The list of weak and weaker currencies, outweighs by a mile including commodity currencies as discussed and as a result Chinese contraction and USD strength, the emerging markets continue to weaken. Not only will a rate hike attract money away from developing economies but when they those rates rise, the outlook for commodities is only further downward pressure.

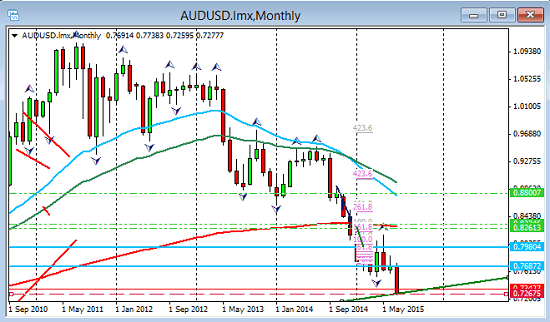

A note on the Aussie dollar as Mr. Stevens has the habit of confusing the market. This last week he admitted further rate cuts were likely and yet he also surmised that lower rates have risks. New lows against the USD and a missed CPI lean into the theory of more downside action. This of course on hold for a possible pullback on another statement from Stevens on Thursday. Maybe he will give us some clarification on policy .

This is another precarious technical chart showing a monthly support level;

And if it breaks this level there is plenty of room beneath it.

The outlook means short opportunities only against either the GBP or the USD.

The Euro has benefited from the recent optimism surrounding a Greek deal but therei s a long way still to go. The IMF have made decision to renegotiate their own deal with Greece once the EZ has an agreement in place with obvious pressure now exerted on the Europeans to seriously restructure the debt which the IMF feel is unsustainable. There is surely some room there for further upset in the German quarter.

Of course QE advances apace within it’s monthly targets and with bonds in Europe advancing during the week the pressure has once again been on the yield. The following example is the German Bund

The outlook therefore remains bearish but there may be further room to pull back against the USD. Wednesday will hopefully provide some clarity and hopefully some shorting opportunities.

The Week ahead

Monday, USD core durable goods (all US main indicators are important and being watched)

Monday, USD core durable goods (all US main indicators are important and being watched)

Tuesday, GBP GDP…big number. US consumer confidence

Wednesday; FOMC Fed Funds rate and statement. Attention please!

Thursday, RBA Stevens statement

Friday Canadian GDP and Chinese PMI and non manufacturing PMI.

The Week’s Watchlist/Trading Suggestions

Some strong catalysts revealed by that calender so timing is everything!

After Tuesday’s GBP data, GBPCAD for long opportunities.

After FOMC, longs on USDSGD, GBPAUD and shorts on EURUSD and AUDUSD. USDCAD is also on the radar but needs a healthy pullback, also one to watch after the FOMC.

If sentiment does shift to a more risk averse climate, then the AUDJPY and the EURJPY will hit the radar.

In conclusion, the week’s events, in the perspective of the two focal points of US policy and sentiment will no doubt bring opportunities. Sentiment is a must to monitor . China may well be in a classic bust phase, but no-one knows for how long or just how bad it can get.

This affects not just the commodity and emerging currencies who may be the fastest to feel it, but in the big picture global economic stability, recovery and policy. Perhaps even more importantly it is how these effects are perceived, that will give us the guidance as traders that is essential for both profit and protection.

Judith Waker

If you would like to learn how to trade like a pro check out our $1 offer by clicking on the banner below

0 Comments