No one needs to be reminded that the focus this week, not to mention the speculation rests on the decision of the FOMC. Ladies and Gentlemen, place your bets. Yes indeed a lottery to be avoided. Markets are in a state of balance and the camps are equally strong on both sides of the speculative divide and then some who occupy the middle ground, the ‘too close to call camp’. The decision will not be known until Thursday so ahead of us , with a couple of exceptions, we have a side-line week and a chance of the USD sinking a little as more positions are closed ahead of the meeting.

No one needs to be reminded that the focus this week, not to mention the speculation rests on the decision of the FOMC. Ladies and Gentlemen, place your bets. Yes indeed a lottery to be avoided. Markets are in a state of balance and the camps are equally strong on both sides of the speculative divide and then some who occupy the middle ground, the ‘too close to call camp’. The decision will not be known until Thursday so ahead of us , with a couple of exceptions, we have a side-line week and a chance of the USD sinking a little as more positions are closed ahead of the meeting.

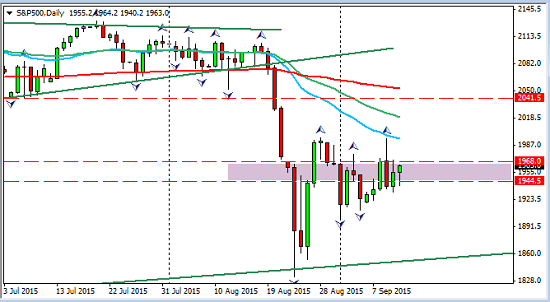

What has been obvious is the formation of ranges as the markets now lay in wait. Even the risk climate seems to have consolidated to a range where break-out either side is possible.

Here is the S&P.

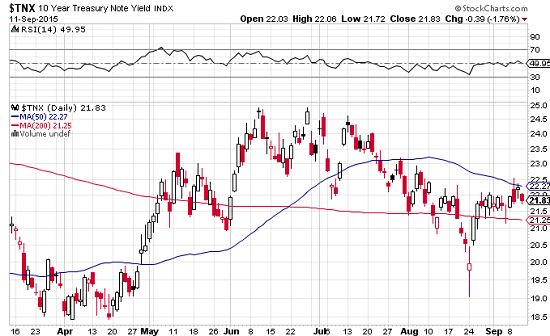

The 10yr yield, chart courtesy of stockcharts.com

the list goes on, the CRB, the Vix, Eurostoxx etc etc

The FOMC will contain implications on risk tolerance but there are other factors now threatening this with the obvious focus in China and more confusing data this past week. Of course implicit also is the perception of the FOMC committee of the state of global play as well as domestic. And then there is the interpretation of the perception! It is little wonder that uncertainty reigns and that volatility is on the rise in all sectors, currencies, bonds and equities.

On the subject of risk, it should be noted that there is disagreement on that also and there are analysts reporting this weekend on both aversion and appetite going into next week. The truth is if you look far enough you will find of evidence of both and can justify either position, which obviously leads to the possibility of either outcome. There is a much more sensitive and fragile environment and thus perhaps a slight negative bias at least one we have to watch for and seek the appropriate opportunities should the risk -off camp re-group. More of that later.

Markets In Waiting: To Raise or Not to Raise

With most if not all the arguments expressed for and against there is little point (although no slow down in the publishing of opinions) in making a case either way as we look for the opportunities ahead. Except perhaps to briefly review the scenarios.

- Rate rise, dovish tone. The language will be important as always and any strength in the USD could be watered down in the statement.

- No rate rise but indications of commencement in October, or December. Both will carry different weights and again the statement will carry even more.

- Global issues too grave, no rise and stay accommodative. The US would in those circumstance still remain ahead of the pack in the policy curve but the divergence will be narrowed, the message sent of disinflationary gloom. At the moment in the Global economy ‘betting office’ this is the least likely outcome.

There is apparently a 28% chance of the hike this coming week. Post -meeting will bring some clarity back (we hope) and with it some longer term opportunities.

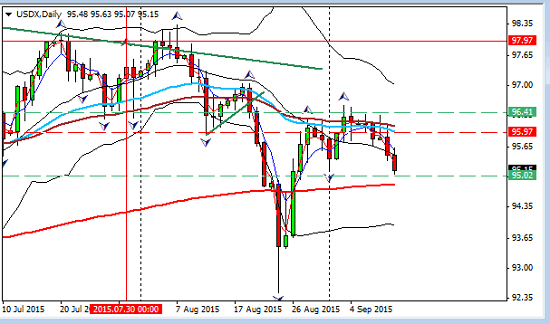

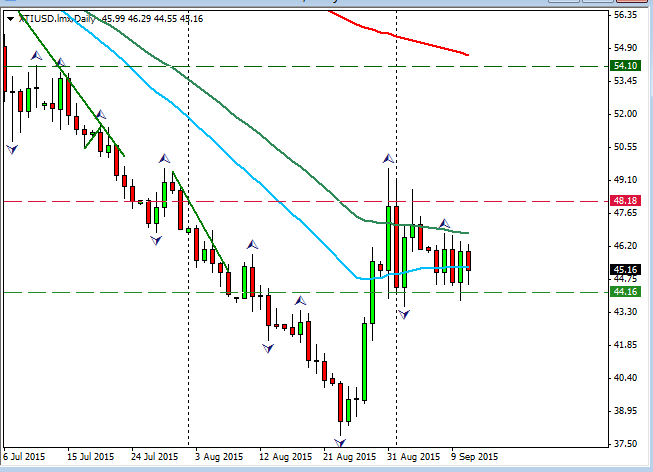

The USD index shows the same ranging behaviour but with a downside this week indicative of moves onto the sideline and the closing of trades; its also very interestingly placed for a set-up…

When China Sneezes.

We all know the old saying that when the US Sneezes, Europe catches cold but economically we have a wider zone of influences and influencers . The result could well be influenza! But as we know, it is not the US that we are worried about but the Chinese crisis. Is there a Chinese driven global recession on the horizon? This week saw exports falling 5.5% and imports by a wapping 15% . It beat the expectation but the numbers are of great concern and of course the ‘knock-on’ effects are indeed global, from Asian emerging markets all the way to German auto-manufacturers. Yes they have been hit and exports to China are significant enough to cause concern.

We all know the old saying that when the US Sneezes, Europe catches cold but economically we have a wider zone of influences and influencers . The result could well be influenza! But as we know, it is not the US that we are worried about but the Chinese crisis. Is there a Chinese driven global recession on the horizon? This week saw exports falling 5.5% and imports by a wapping 15% . It beat the expectation but the numbers are of great concern and of course the ‘knock-on’ effects are indeed global, from Asian emerging markets all the way to German auto-manufacturers. Yes they have been hit and exports to China are significant enough to cause concern.

Just to take one example, 20% of Australian imports are from China. Then there is the continuing pressure of emerging markets. Any Fed decision can damage this but there is little that can change its direction. This is not about lack of inflation but debt and its sustainability or more accurately its un-sustainability. A spill over from Brazil could hurt others as downgrades to junk status, as we witnessed there this week, put yields under pressure as bonds are sold. Turkey is on the hit list, so is South Africa as are some of the ex-Japan Asian bloc. Money continues to flow from these economies and that is another factor evidencing a shift in sentiment.

There was one number during the week that on first blush should have brought some optimism of it’s own, CPI came in at 2.0% beating the expectation. Unfortunately it presents a problem and was seasonal number raised by the prices of pork. The factory prices, PPI, are deflationary and deepening with a resulting divergence. That is a problem that will make profitability even harder to maintain, let alone improve.

Markets In Waiting:Monetary Policy and Divergence

There are still only two players on the tightening end of the scale. This week we saw a number of economies on rate hold, whatever their stance, excepting of course the RBNZ. They not only cut the rate but gave a dovish forward guidance that ‘’ at this point some further easing seems likely’’. As they expressed ‘further depreciation is appropriate. Citing global circumstances and commodity declines growth was downgraded. Their exports have been significantly damaged.

Goldman Sachs made a bee-line for Australia , giving them a 1 in 3 chance of recession within a year. The language and tone of the RBA again will be carefully watched for signs of dovishness and the possibility of rate cuts down the road.

In the UK, the BOE referred to the Chinese fall out as ‘headwinds’ which at present are not seen as blowing them off the course of tightening, ‘Global developments do not as yet appear sufficient to alter materially the central outlook described in the August Report, but the greater downside risks to the global environment merit close monitoring for any impact on domestic economic activity.”

The committee did downgrade growth forecasts from 0.7 to 0.6, votes remained at 8-1. Economists are looking at the first half of 2016 for the first rate rise in the UK.

Wages have been edging up and there is more data on Wednesday will be carefully watched, courtesy of tradingeconomics.com;

The market is looking for 2.5%.

A mixed bag of data but some signs of underpinning might mean that following some nice pullbacks there may be some long opportunities in the week ahead. This economy is best paired with commodity currencies as it still shows weakness against the USD and as we are all too well aware, that arena is too tricky this week.

The Oil Market, another market in waiting;

More from Goldman Sachs this week , included warnings of oil as low as 20USD a barrel. On the other side of the picture, The IEA (international energy agency) are predicting oil production in the US will collapse next year as a result of the low prices. There is little doubt that rig closures have suffered the impacts but there is still a supply side issue and no signs of abatement from Opec on production. There is also diminishing storage facility and falling demand. It may take more than US production suffocation to lift the oil market and of course as we know already it is not difficult for the Rigs to re-open if prices do manage to rise. This is something of a vicious cycle as China a major importer of crude slows growth and decreases demand. Deflation imported and exported. Just try to throw the Fed decision into that equation!

The Week Ahead; All About The FED!

There is other news,

Tues, GBP CPI, US core retail, German economic sentiment.

Wed; GBP Average earnings, USD CPI, CAD Manufacturing.

Thurs …FED!! Also GBP retail, USD manufacturing,

Fri, RBA statement Cad core CPI

Its a watershed week. No predictions, no gambling but a few pairs to watch;

GBPNZD, short

GBPAUD, short

EURGBP, short

AUDJPY, short ( sentiment related)

Post Fed; looking for some long term opportunities

USDNZD

USDTRY

USDSGD

EURUSD (for the brave)

Safety First

The reality for this week is this; bonds balanced, US equities balanced, risk balanced, commodities balanced, oil balanced. You get the picture. The USD index will be on the watch list after the Fed decision and after weighing up the risk climate. So will the S&P 500. All bets are off until then. The Jury is out so we have to wait the verdict and keep the powder dry. Now that may well be a mixed metaphor, but I hope my meaning is clear!

Judith Waker

If you would like to learn how to trade like a professional check out our 5* rated forex mentor program, RISK FREE; by clicking on the “Get Started Today” Button below

0 Comments