Viktor Frankl once famously said that “Between stimulus and response, there is a space. In that space is our power to choose our response. In our response lies our growth and our freedom.”

Viktor Frankl once famously said that “Between stimulus and response, there is a space. In that space is our power to choose our response. In our response lies our growth and our freedom.”

In his extraordinary circumstances as a holocaust survivor, this is a profound philosophical truth but like all universal truths and laws it has a more mundane and every day application, including in the world of economics, as they play out on micro as well as macro levels.

Take the business cycle. Knowing where we are in this cycle is critical to trading decisions. If you are not aware of that you may just as well be playing poker. The economic expansion, peak, contraction and trough are all part of the ebb and flow which permeates everything we see and understand.

As hard as central banks of late have tried to manipulate and control the downwards part of the cycle and manage the trough, they cannot change it, only shift it. In all economies around the globe excluding just one, the US, the role of the central banks is currently and somewhat anxiously, to prevent the ’trough’ becoming deflationary.

In the US they now have to manage their way out of a long and massive QE program without making waves. A self inflicted problem but one eventually, which the current ailing economies will also have to face once recovery is stimulated.

In a financial context, the ‘space’ shows itself as the decision gap between cause and effect and just how the trading community perceive the ‘causes’ does indeed determine the outcome, the ‘effects’.

Sentiment on lower time-frames is noise, on a higher time-frame it is an ongoing assessment and prediction of monetary policy. At the quietest macro level, sentiment is dominated by this.

To understand the sentiment of those big market players in the gap is to increase our probabilities of accurate prediction and there are tools available to help us.

Forex Pro Chart analysis

All financial charts display human behaviour, to a greater or lesser degree and whether we are aware of it or not. When a technical analyst measures stochastic or momentum what he is really looking for is how the traders are behaving in an effort to predict their next move.

What is even more interesting is when they take a fib measurement they are actually expecting the involvement of those universal laws (fibs are all based in the golden mean)

This week in our pro site, we saw how the market profile chart shows elements of market behaviour that can’t be seen in other more traditional charting methods.

This is an accurate gauge of what I like to call ‘gap sentiment’ and it can be looked at on a weekly perspective to gain an even further out view.

The Causes

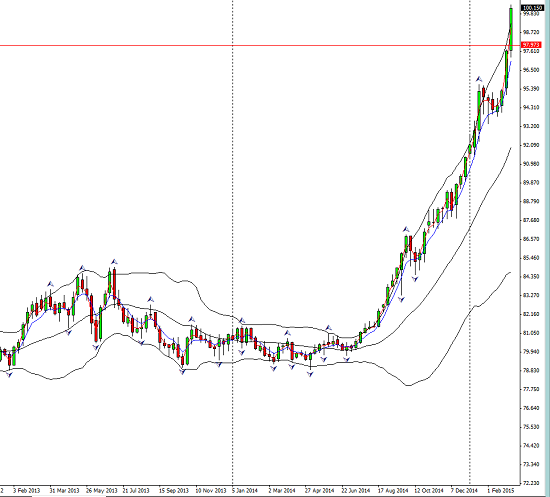

The USD index has been in a steep uptrend since June last year, having taken a pause in February and it only took an NFP announcement to relaunch it to a new 12 year high. Here is the weekly chart showing just how strong this last few weeks have been;

The market appeared to disregard the missed retail numbers from the US on Thursday and the disappointing consumer index on Friday and powered into the close as the index above showed clearly. There is the FOMC meeting this week and they may not have missed it and may well start to factor in the less than impressive data that is coming out on a regular basis. The employment side is where the strength of the recovery is showing. Their interpretation of the latest round of results is a potential market mover and will give further insight into the possibility of the June rate hike.

For that they may need more proof of signs of inflation or at least a stabilisation. Yellen has repeatedly stated that inflation challenges are an obvious consequence of oil price falls but she will probably need at least, some evidence of firming. There is also the issue of that inocuous word, patience. The market is expecting it to be dropped so expect a reaction if remains. It may at least offer a buying opportunity on a pullback.

For that they may need more proof of signs of inflation or at least a stabilisation. Yellen has repeatedly stated that inflation challenges are an obvious consequence of oil price falls but she will probably need at least, some evidence of firming. There is also the issue of that inocuous word, patience. The market is expecting it to be dropped so expect a reaction if remains. It may at least offer a buying opportunity on a pullback.

Monetary policy and US strength has been the catalyst for weakness elsewhere, but the ‘other’ major economies, contain a list of their own causes. It really has become the US v. the rest. Elswhere, it is monetary policy again that remains the focus and the stark comparative. Plenty of causes here; QE in the Eurozone, the most recent, Japans ongoing liquidation program and then there is the deliberate lowering of rates, aka the currency war.

In total 24 economies around the globe have lowered rates this year, including Australia, Canada, Denmark, Switzerland Sweden and this week the latest additions are Russia and South Korea.

Watching Forex Sentiment

To consider what is happening in the decision arena we turn again to familiar sentiment indicators. These are already on our weekly radar and as always with measuring sentiment there are no blacks and whites (well rarely) and subtle shifts and transitions between the polar environments of risk-on and risk-off can always be found. With deflationary threats and monetary stimuli on the rise, oil and commodities still falling, the possibility of tightening in the US combined with a dollar that is strong enough to dent US equities, we have an incredibly complex and distorted mix. The current risk-on environment is indeed fragile.

The Vix, our old friend measuring Sand P volatility, affectionately known as the fear index. This week fell back and does not cause warning bells until above 20 and holds or advances;

The Bond Market

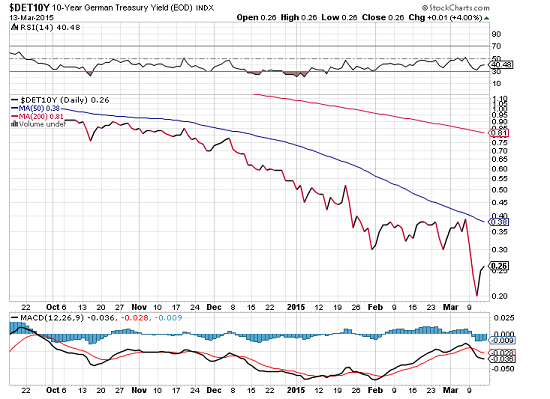

Last week we took a look at how bond yield’s reveal information that is predictive. So what can we glean from the bond market this week? The US 10 yr note gave back the value added last Friday as NFP numbers were announced, settling at 21.42 denoting more caution this week ahead of the FOMC meeting;

Meanwhile in Germany the comparative 10 yr bond fell to o.2 and the nearer term bonds falling further into negative territory. This was to be expected as the ECB started their QE purchases of German and Italian debt;

Of course Greece bucked the trend as the yield advanced. No ECB buying there. There are a mass of hurdles to negotiate in the months ahead as the Greek’s face the threat of bankruptcy. This is another red flag for the Euro and the four month reprieve is just that, it is not a log term solution and the Greek balance sheet may not last that long;

Equities

The Sand P had a second down week. Not a confirmed sign of risk aversion but surely one to watch. As the USD gts stronger there is reason to think that equities will suffer and no doubts that the energy sector already is. Here is the daily chart;

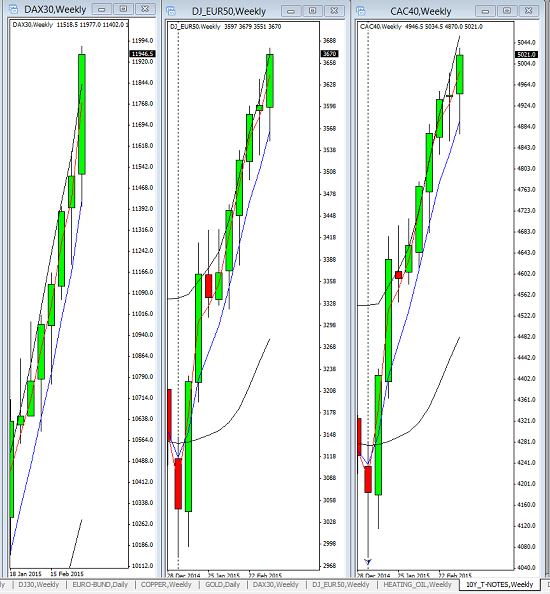

In the European bourses all systems are go as QE brings money into the economy. Here is a chart of the DAX, CAC and Euro 50 on weekly time frames.

A clear investing switch from US to European equities.

Gold

The advancing dollar did nothing to help our safe haven metal. The closer US interest rate rises are perceived the more pressure on the downside. This is a non interest producing investment and we are in an environment of yield hunt. There my be further room on the downside with some analysts eyeing 1000. Here is the monthly chart;

The Effects

A few weeks ago when the USD seemed to be on a break, careful selection of pairs was required. This last week the USD trampled on every one. The charts speak for themselves,

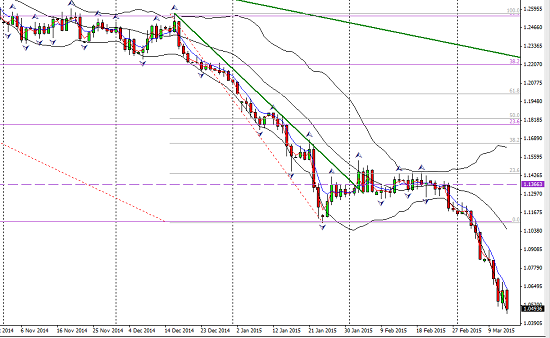

Here is the monthly EURUSD, a double cause of QE commencement and US strength;

The inevitable talk of parity continues almost to the point of a self fulfilling prophecy and there is no doubt that the EZ could benefit from a devalued currency. It is export oriented and Germany its best example with a maufacturing reliance that needs the current stimulus.

The Forex Opportunities

The news and event to watch for of course primarily revolve around the US and the awaited decision not to mention language of the FOMC on Wednesday. Also to watch will be the minutes from the RBA released Tuesday, Draghi speaks again on Monday at a finance summit in Germany. There is consumer confidence in Germany, an important piece of wages data in the UK on Wednesday also being the day that votes in the BOE are disclosed. On Thursday and Friday an economic summit takes place in the Eurozone, details of LTRO’s the same day. Thursday also will include Swiss monetary policy so steer clear of that one! The week concludes with inflation data in the form of CPI in Canada. Another calender with plenty of catalysts.

The news and event to watch for of course primarily revolve around the US and the awaited decision not to mention language of the FOMC on Wednesday. Also to watch will be the minutes from the RBA released Tuesday, Draghi speaks again on Monday at a finance summit in Germany. There is consumer confidence in Germany, an important piece of wages data in the UK on Wednesday also being the day that votes in the BOE are disclosed. On Thursday and Friday an economic summit takes place in the Eurozone, details of LTRO’s the same day. Thursday also will include Swiss monetary policy so steer clear of that one! The week concludes with inflation data in the form of CPI in Canada. Another calender with plenty of catalysts.

Currency pairs on the radar this week, fall into two groups, long positions in the USD, I prefer to select the weakest economies against the USD and buy on pullback;

For cross pairs, its a question of looking for shorting opportunities in the EUR, again allowing for pullbacks.

There is a further decline in commodities which will affect the commodity currencies. Here is the CRB on a daily chart;

The oil market dropped again and some analysts believe it may have further downside. The oil inventories are growing, although in-line with expectations, and as we expected in their inverse relationship, as the USD advanced early in the week, oil prices moved down.

In conclusion, staying with the biggest picture for long term trades is the quietest way to trade. Watching the news may give opportunities but understanding the basic concepts of monetary policy and the current differentials is key, as is understanding the effects of those decisions on trader sentiment. For that there is no replacement; no Holy Grail, no quick fix indicator . This is the macro edge.

If you are interested in our pro site please press the link below.

Judith Waker

0 Comments