The confusion that has gripped the markets in the last few weeks has shown no sign of abating. But why? This week we will look at the bond market in more depth for clues; a market which has caught even seasoned traders off balance and rushing for an exit from portfolios of ‘safe’ euro bonds triggered by the commencement of the QE program in the Eurozone. Recent speculation about recovery and the reappearance or at least early signs of inflation followed the meteoric rise of the German Bund in the last two weeks. It however appears to have little fundamentally to back it and warnings continue about serious distortions as a result of unprecedented central bank manipulations. Maybe what we have seen this week is a ‘not so mini’ euro taper tantrum.

The confusion that has gripped the markets in the last few weeks has shown no sign of abating. But why? This week we will look at the bond market in more depth for clues; a market which has caught even seasoned traders off balance and rushing for an exit from portfolios of ‘safe’ euro bonds triggered by the commencement of the QE program in the Eurozone. Recent speculation about recovery and the reappearance or at least early signs of inflation followed the meteoric rise of the German Bund in the last two weeks. It however appears to have little fundamentally to back it and warnings continue about serious distortions as a result of unprecedented central bank manipulations. Maybe what we have seen this week is a ‘not so mini’ euro taper tantrum.

One of the two main events of the week saw the NFP data release which brought mild optimism of recovery slowed down but still tangible.

This week’s other focal point, saw a shock majority win in the UK for the conservative party which pushed the GBP into a fresh rally against the USD as the uncertainty of election outcome was against all predictions (including mine) not replaced by the uncertainty of a hung parliament but replaced with a clear majority government, albeit not a particularly strong one. To remind ourselves that one should never make assumptions in the financial markets might seem like locking the stable door after the horse has bolted, but worth the reminder as every week seems to bring another surprise. It is that kind of market.

How Bond Selling Shook the Forex

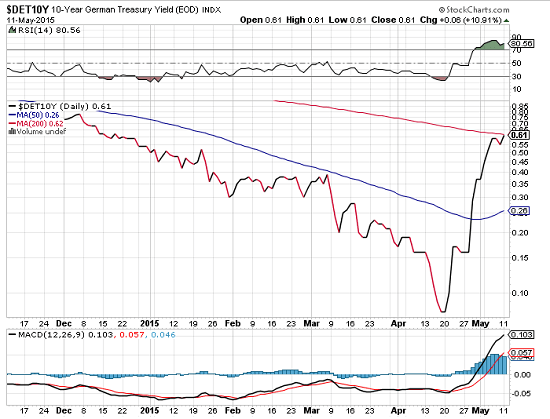

There is not much doubt that major positions have been closing out what is known as the QE trade, the bond buying spree in anticipation of monthly liquidity from the ECB. There was among the funds an anticipation of profit as the ECB’s buying targets gobble up the supply side on a monthly basis pushing up values. Their intention is for QE to continue at least 18months from its commencement. The resulting yield drops have been dramatic to say the least as we watched the German 10 yr yield fall towards the negative side. What has happened in the last two weeks wrong footed some of the most seasoned professionals. Chart courtesy of stockcharts.com;

A fast and furious reversal in the Bund market has left us with even more confusion as higher yields and lower bonds usually imply inflation expectations are growing. The recent oil rally would support that theory. As for data there is not much to support that view, with retail sales and German PMI disappointing this week.It is early days to declare deflation a conquered enemy but there is no doubt that sentiment has made a u-turn whatever the reason. Even in the US economy there is only the shallowest signs of inflation gaining traction and there are many of the view that oil prices rises are unsustainable as the US starts to increase output in improved conditions in the second half of the year.

So if it isn’t inflation what is it? Well Bill Gross called it the sale of a lifetime with yields touching zero and beyond. As the Euro rises it is less attractive as a funding currency, and buying back euros to close out these carry trades may well have added to the effect. Liquidity is another issue in the rush for the exit which has driven the yield.

US Policy expectations and the NFP

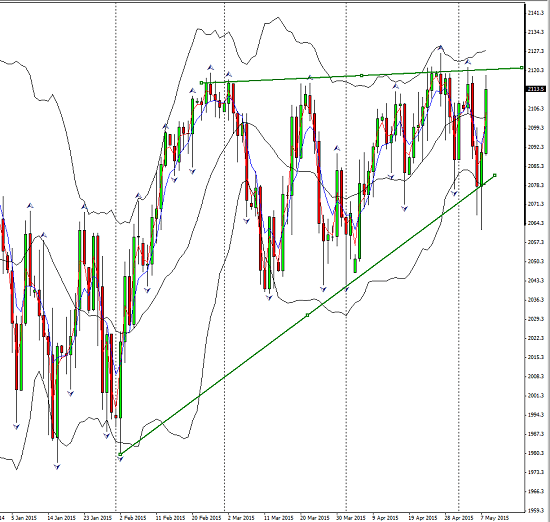

Last weeks NFP numbers prompted a rally in the S and P on the last day of the trading week. Here is the Daily chart;

The US equities are wary of interest rate hikes but the numbers came in just right. The FT referred to it as the ‘goldilocks’ report! Not too high to give the Fed cause to move in June and not too low to spook the recovery projection, however slow it seems to be. After March’s number this was a step in the right direction. Unemployment fell but wage growth was unimpressive and that is a big factor in weighing inflation expectations as the FOMC know well. 0.1% for the month and 2.2% year on year. The consensus view now is that June is almost certainly out of the picture but September is still a possibility . There are many who see the progress slow enough for the rates to be left until December or early 2016. There is a long way to go and plenty more in the way of speculation and potential sentiment shifts.

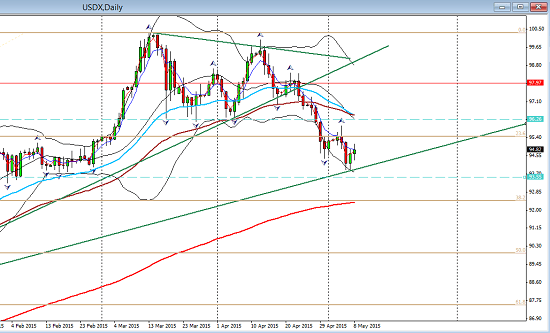

As for the USD the index was little changed by NFP

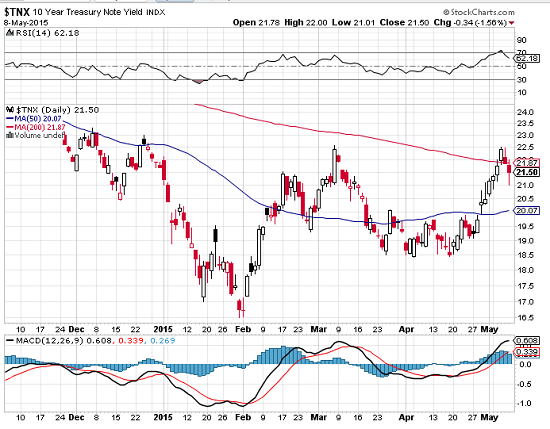

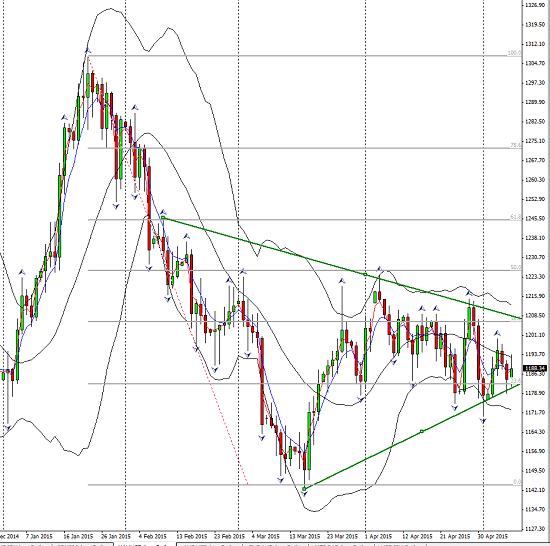

The story of the US 10 year yield continues to develop as its counterpart in the Germany was sent into the stratosphere. Here is the US 10 year on a daily chart; chart courtesy of stockcharts.com

As the chart shows the yield has itself seen a significant rise advancing effortlessly through 2% to 22.5 settling back 4 basis points on Friday after NFP to 21.50

The UK Political Upheaval

A shock result in the UK elections pleased the market with rallies in the GBP and the FTSE. There were few who thought a majority government was a possibility

Here is the daily GBPUSD;

The political map has been re-drawn with Ed Milliband’s party severely punished by the Scots vote and the Lib Dems all but annihalated. Three leaders resigned by the end of the day. It was an extraordinary event. The elected party however have a slim majority a huge deficit and an angry Scotland divided from the rest of the UK not by the independence vote which failed last year but by a total dominance of the Scottish National Party north of the border. The new government without a healthy majority is holding a veritable Pandora’s box. They also have a mandate to hold a European referendum within their five year term and the risk of a Brexit. How this plays out is as unpredictable as anything else Global macro is revealing but it has begun by lending some strength to the GBP rally and however short lived that may be, remains to be seen.

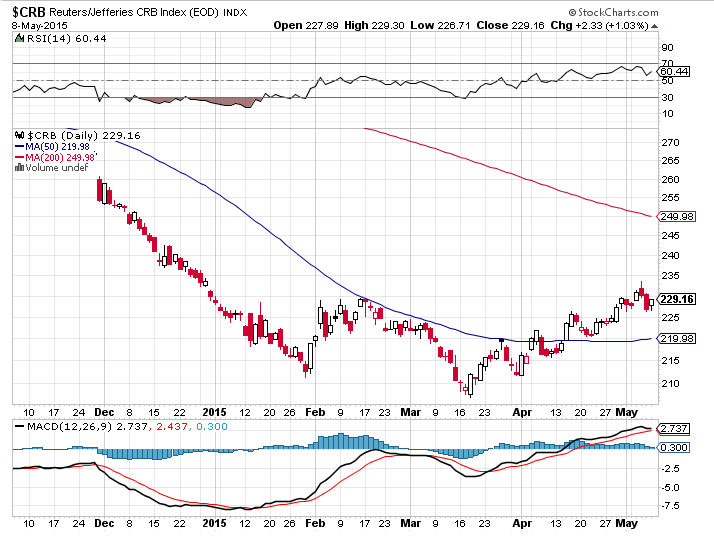

Commodities

With the index weighted towards oil the rally has continued since the middle of March with a small pullback this week. Iron ore and copper have rallied with the oil market. But a word of caution; as with oil there would seem to be a requirement now for solid global growth and demand to sustain this rally and there are not too many signs of that yet. We cannot yet say this is more than a correction in the drastic down-move that preceded it;

As for gold, it seems to wait and watch and continue it’s consolidation;

Next Week’s Event’s Calendar

There is a lot of GBP focus in the coming week with Bank rate Monday, manufacturing Tuesday, average earnings a Carney speech and an inflation report Wednesday. These events will give some insight into the sustainability of a GBP rally.

In the US, retail sales will be one to watch on Wednesday and PPI and unemployment Thursday.

In New Zealand retail numbers will also appear Wednesday.

With the risk of short covering and bond ‘fall-out’ in the Euro, predicting its path has become extremely difficult. The rally continues to mask underlying weakness and now this apparently false illusion of inflation brought on by mass restructuring of funds has clouded the outlook further. Watch for the catalysts that can expose these weaknesses and wait for alignment of fundamental and technical confirmations. Patience is key. There are Eurogroup meetings this week and German GDP. Whatever the fundamentals may reveal the sentiment change cannot be either ignored or fought.

The Cad had a mixed bag of data last week with disappointments in employment and trade balance but a strong PMI at 58.2. It is vulnerable to oil risk and once again needs a close monitoring of the crude chart and the USD index. It should be noted that the BOC take a careful note of the jobs market.

The JPY continues to look weak with continuing need for liquidity to give any chance to inflation expectations. The futures market also showing bearish sentiment. USDJPY on the radar this week.

There may be some potential to long the GBP after the major news events and if they signal follow through. It is a wait and see scenario.

RBNZ reports and retail numbers may give some clues for the Kiwi dollar.

The markets have truly been shaken and stirred. Challenging times, unpredictable events and lack of ’normal’ interpretations and guidance from the Bond market have left traders without their usual map for negotiating the way forward. The territory has become extremely alien.

No doubt opportunities will rise but they will require careful handling, measured and conservative risk control and a continuous watch on the shifting sentiment.

Judith Waker.

0 Comments