The focus of the last few days and the biggest factor affecting trader sentiment globally is the continuing and seemingly endless drama playing out between the European Troika and the Greek government. News releases are made, denied and retracted leaving the market to second guess the next step.

The risk of Grexit is growing and the answer to the age old conundrum of what happens when the irresistible force meets the irremovable object might well be solved in the next week. Sentiment is the traders watchword and no-one can afford to take their eye off the ball in case one of them blinks.

There are other major issues including an antipodean rate cut, a Kuroda driven rally in the Yen, some pleasing data for the Fed to chew on next week and a warning from Merkel that re-stirs the currency wars. An echo was heard in the US as, unusually for a politician, Barach Obama weighed in with some maybe careless remarks about the dangers of a strong dollar. We have entered an era where all currencies want to weaken against each other. That presents a problem! There is a fine economic balancing act performing in full view. We will do well to understand at all times how the market perceives it.

Forex Know-How: Euro/Greek Crises

Brinkmanship on Both Sides

We will start in the Eurozone. Merkel has professed and committed, at least in word, to a solution with Greece, ‘where there is a will, there is a way’ The Troika has a line in the sand, austerity and controlling Greek policy. This is not even a purely political issue as I would venture to suggest that the majority of economic experts and analysts will agree that austerity simply does not work in a country struggling with (somebody else’s) debt. The brackets contain the political angle!

We will start in the Eurozone. Merkel has professed and committed, at least in word, to a solution with Greece, ‘where there is a will, there is a way’ The Troika has a line in the sand, austerity and controlling Greek policy. This is not even a purely political issue as I would venture to suggest that the majority of economic experts and analysts will agree that austerity simply does not work in a country struggling with (somebody else’s) debt. The brackets contain the political angle!

And that is Mr Tsipras’ line in the sand….he will not refuse to pay his own people pensions and wages. There is the head-on conflict. What, you may ask, is left to negotiate? Both sides are pushing each other to the limit, but who is set to lose the most should Greece exit the EZ? The answer is that no-ones knows and uncertainty is something the market detests. Brinkmanship is a dangerous game with the fragile beginnings of a Eurozone recovery at stake, maybe even the Union.

On the policy side, despite a more upbeat prognosis for the economic and inflationary recovery in Europe, Merkel warned against the strength of the Euro damaging the possibility of structural room in some of the member states including Spain and Italy and many of the peripherals. The chance of economic growth gaining traction without secure infra structure on a national basis is akin to building a house on sand.

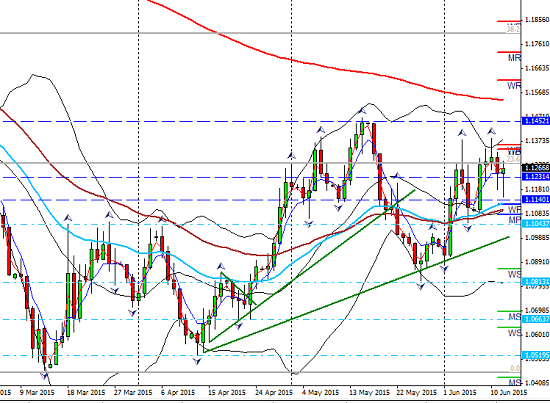

Expect monetary policy and the Greek crises to weigh on the currency which has failed to break the 1.15 level, stalling at 1.1452

The Bond markets again have been volatile with the German 10 yr note approaching the 1% level but closing back at the end of the week and finishing where it started on Monday.

Watching the Bund particularly will give some insight on sentiment as we look forward to the FOMC this week. The divergence between these two giant economies is a stark contrast despite recent Bund strength.

Forex Know-How: US Policy

To Raise or Not to Raise?

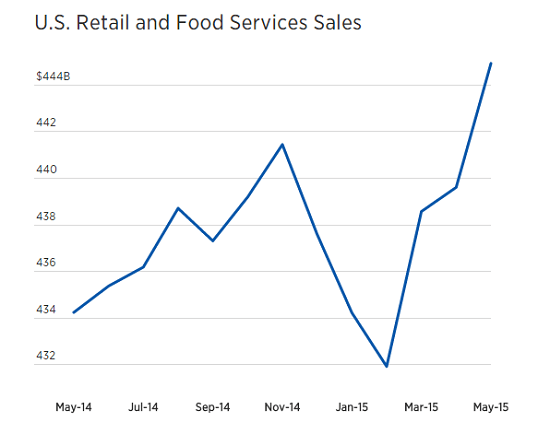

This is just one of the charts the FOMC have been looking at ahead of their meeting on Wednesday. Retail numbers up on expectations and even with energy ripped out the core number came in at 1%

Also the Jolts number (job openings, and a favourite of Janet Yellen) beat expectations as did PPI and unemployment data came in on the number. So the speculation rises on a September hike and thus once again FOMC ‘speak’ will be closely followed and will set the tone for the Forex summer. There is evidence now that the US economy has got some real traction.

There is even a chance that GDP for Q1 which caused a great deal of concern for Ms. Yellen will be revised upwards. This on the back of last week’s strong NFP data will certainly give fuel to the rate hike speculation and the potential reaction to the policy decisions. There are very few that think the rate will change this week but this could be the most important meeting pre hike.

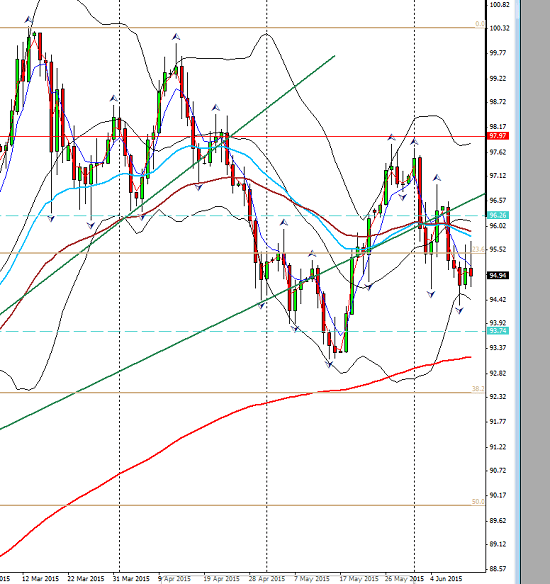

The US 10yr note has steadily tracked up all month pulling back Thursday and Friday. Again this is a market to watch closely to assess sentiment both prior to and after the meeting;

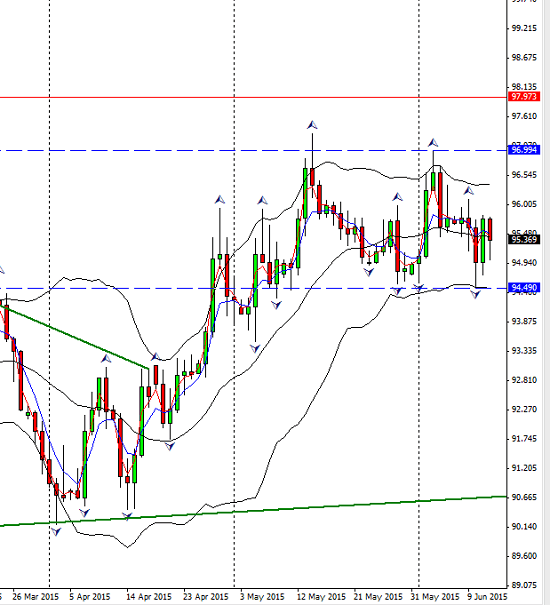

As for the Index, it has seen a two week pullback even after the FOMC but for mush of this week has shown signs of indecision no doubt sourced by the uncertainty around FOMC policy. Technically it is less than 100 pips above a big area of weekly support around 94.

Forex Know-How: Commodities

Antipodean Policy and Commodity prices

There were certainly split views on the Kiwi decision this week , so volatility was a cert when the rate was cut on Wednesday.

There were certainly split views on the Kiwi decision this week , so volatility was a cert when the rate was cut on Wednesday.

Overlooking the housing bubble and focusing rather on domestic difficulties and a GDP severely damaged by the rout in dairy prices the RBNZ not only reduced the rate but warned of at least one more cut this year to protect their economy.

Like their Australian counter-part, they believe their currency is too strong and like many other global currencies are intent on their attempt to establish inflationary pressure. It is not apparent yet. Bias is down so I will be looking for shorting opportunities.

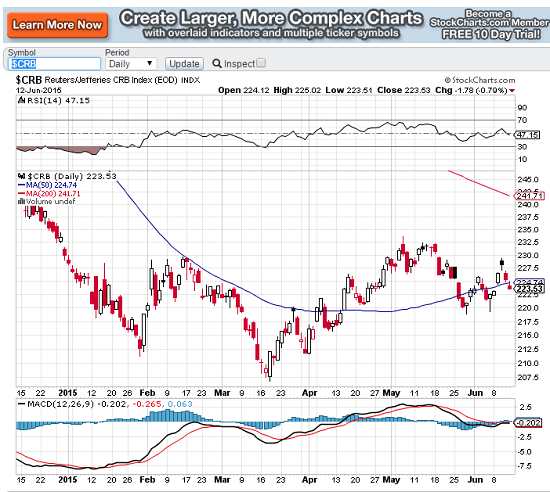

In China, slowing growth and another problem with low inflation has already brought an easing cycle which is likely to continue. Low oil prices have not helped here. CPI fell last week and missed it’s number. The copper market fell on Chinese news as it is it’s biggest consumer. The commodities index fell again on the week after the period of stability. This of course negatively affects all the commodity currencies. Chart couresy of stockcharts.com;

Mr Stevens in Australia asserted his opinion that the Aussie dollar is still too high. Whilst the rate held, it remains to be seen if the policy will continue through the year especially in view of the low iron-ore prices and perhaps also in the wake of the New Zealand policy change.

Black Gold and the CAD

There is no doubt that US production has been affected with falling numbers and significant rig closures. On the other hand the drop has to this point been less than a pro-rata number based on those closures. Add to this the factor that the Opec countries are producing more than their quota, a ceiling of 30 million barrels a day. Oil futures were lower by week end.

On a technical level, crude is resisting the 200EMA and held for now at least, by it’s current $5 range

For the Cad, it has seen a sound rally. It is vulnerable to the oil market and the effect of the original rout may not yet be fully felt. Despite upbeat comments and a holding of the rate there was a contraction in Q1.

Emerging Gloom

Thrust into global growth by US QE (cheap money) export demand and high commodity prices, emerging economies have experienced the decline in global growth more than most. The IMF have referred to ‘uneven global economic growth’.

Thrust into global growth by US QE (cheap money) export demand and high commodity prices, emerging economies have experienced the decline in global growth more than most. The IMF have referred to ‘uneven global economic growth’.

Falling commodities and now the threat of rate hikes in the US further endanger these economies. Exports have dangerously weakened such countries as Singapore, Thailand and South Korea.

This week the world bank cut its growth forecasts with this warning from it’s president, ‘’ developing countries were an engine of global growth following the financial crises, but now they face a more difficult economic environment’’

He added that the developing countries which include India (the shining star) Turkey and South Africa should all ‘prepare for the worst’

The Singapore dollar has been buoyed of late by its monetary policy but with the big picture in mind the rally may soon be over and the downward bias resume. It will be important to wait for signs of rejection and it may have a way to go ;

The UK

Another warning of credit rating doubt on the decision to hold a European membership referendum. A lot is at stake and uncertainty once again will return to the GBP.

Mixed results and no clues from Carney last week so we must wait for some guidance this coming week. There is a deal of confusion and mixed signals where the GBP is concerned and may well in comparative terms, not quite so weak as some of its counterparts. A bit of a grey area for the Forex trader.

Risk Aversion

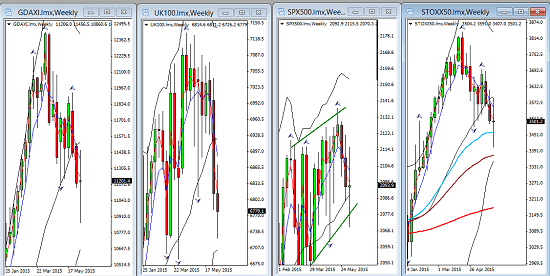

Equities remained very indecisive is this weekly comparative is anything to go by. This is the weekly perspective at the end of last week’s trading;

The jury as they say is out. One of the sentiment monitors commonly used in the market as a fear barometer is the AUDJPY, showing a similar tight range;

There are two factors to consider with the JPY. Underlying fundamentals are still weak despite Kuroda suggesting the currency was cheap enough. The policy is very likely to stay accommodative. However, there is also the factor of risk aversion. If the Greek crises unravels into Grexit then there may be a search for safe havens and that makes the JPY vulnerable to volatile strengthening moves.

The Week Ahead

Well the big one is the FOMC meeting from our global reserve currency and remains the only economy showing any sustained growth. This could prove to be the meeting of the year so it demands close and careful attention. Monetary policy, especially from the US continues to be at the root of the market moves and the driver of drivers!

Well the big one is the FOMC meeting from our global reserve currency and remains the only economy showing any sustained growth. This could prove to be the meeting of the year so it demands close and careful attention. Monetary policy, especially from the US continues to be at the root of the market moves and the driver of drivers!

June 18th appears to be D day for the Greek crises and the ‘final meeting’ so fasten your seatbelt for that one.

Also in the mix,

Tuesday, minutes from the RBA (language and tone again!) NZD Dairy, German Sentiment, GBP CPI

Wednesday; GBP Average earnings, rate vote, FOMC 6pm GMT.

Thursday; GBP retail sales, USD CPI (and the Eurozone meeting!)

Friday; BOJ, Canadian retailing CPI

In Chinese, the word crises is the same as the word opportunity.

There are catalysts this week that can not only exacerbate volatility and provide strong moves but also lay the path for many ‘post-meeting’ opportunities .

There will have to be informed and careful selection. As always the first step is strict disciplined risk control.

The other essential is to stay informed and aware and trade like a pro.

Judith Waker

0 Comments