Indecision doubt confusion, these are the characteristics of the current financial markets.

Indecision doubt confusion, these are the characteristics of the current financial markets.

Speculation is rife, forward guidance non-existent and then there are a number of young swans with the potential of more than one maturing into black plumage.

There are intense political issues, the pressure building in Greece and the risk of default growing with all the consequences that may bring, the potential mis-management of tightening in the US , global stagnation warnings from the IMF.

Unchartered Waters

To say that our financial markets are on the choppy side, pun intended, might be stating the obvious but take a look at the fundamentals that drive it and it should hardly come as a surprise.

With the speculation on US rates waxing and waning on data on an almost almost daily basis, UK elections and the never ending Greek crises undermining the whole philosophy of democracy and even a bloomberg outage thrown in last Friday, it has become an unnerving environment for the the most sanguine of traders.

Sentiment is one of those ‘must haves’ on a traders watch list. Risk on and Risk off have a generic quality and hard to assess as a definition of the overall environment as we shift around the edges of both depending on the daily events calendar.

Pulling together all the strands is becoming increasingly difficult and the more so as a result of Central Banks skewing the business cycle with as yet, unknown consequences.

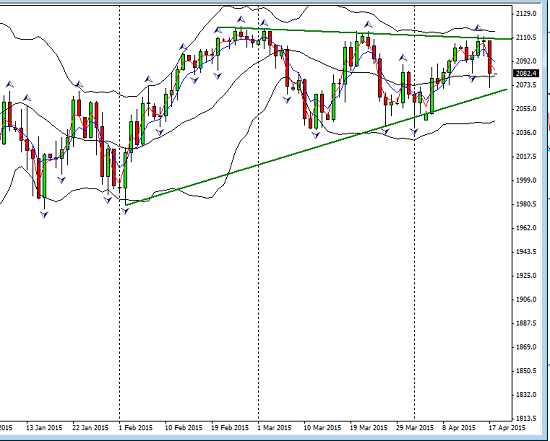

Equities in the US and the EZ had nervous down days on Friday,

Here is the S&P daily chart showing its boundaries to monitor;

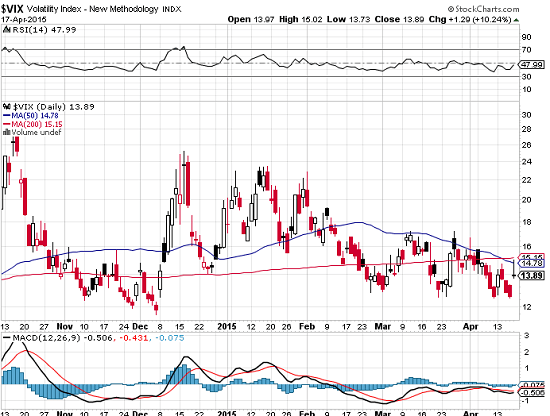

Volatility in the S&P whilst still at low levels also jumped up Friday

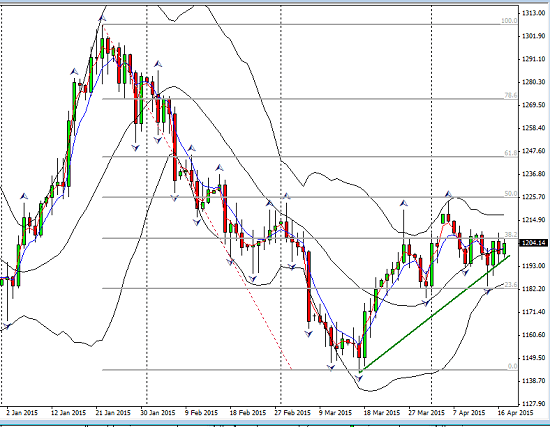

Gold was slightly down on the week, but still enjoying the daily uptrend and gave a pop of $6 on Friday;

To Raise or Not to Raise

Not so much a question, as a play for time from the FOMC. Unchartered waters for sure, three rounds of QE, and enormous amounts of liquidity raise the problem of how to unravel it without, as the IMF warned this week, a ‘stampede for the exit’. Bond funds, hedge funds and investors looking for Treasury safety face risk of losses as soon as yields start to advance.

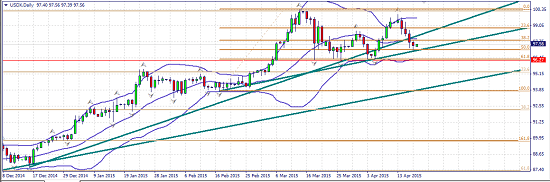

The USD index has pulled back but with all the various interpretations of every piece of data that crosses the wire, there is no sense of how deep that correction could be. Without forward guidance the market is left to speculate react and sometime overreact. The consequent volatility is the new norm in the Forex.

The USD did get a reprieve towards the end of the week as Manufacturing numbers beat the expectation as did consumer sentiment. Core Inflation (CPI) came in at the expected number, but even so it was a solid 0.2% increase.

Welcome Respite for Commodities

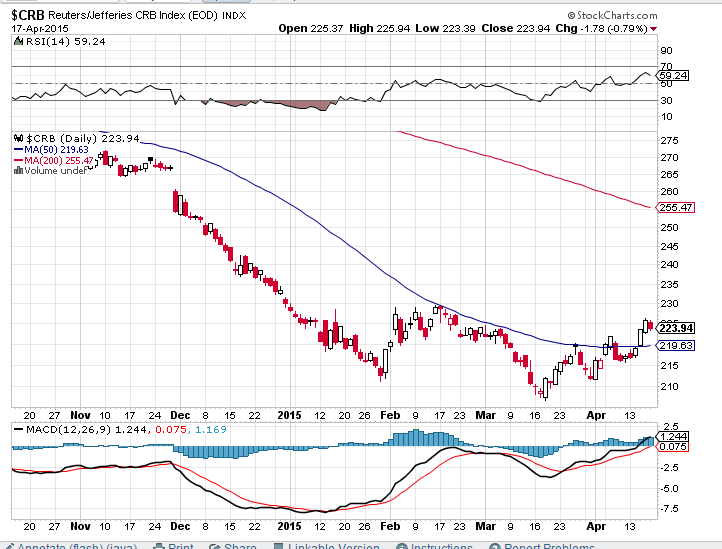

Improving commodity prices and the recent oil rally has seen the commodity currencies do well against the Greenback but the fundamentals haven’t changed significantly.

Take oil, currently trading at 57.61 , helped significantly by the first noticeable fall in inventories in the US this week. It has broken the daily range and now sits neatly on the weekly 23rd Fib. An important level to watch and the high of the larger weekly range.

The prospects of maintaining the rally are still low. Despite acceleration of US rig closures, the supply continues to build from the OPEC countries. In the US many of the rigs have been capped and any increase in price will bring them back into production very quickly and with little expense. The sector most affected by the declining price has been the deep sea drilling but without a major impact to the supply. In addition any Iran agreement will swell the reserves again.

Iron Ore has to be mentioned here. The highest levels seen in a year and as a result of increased demand. However the exuberance may not be long lived as Chinese growth slows further and iron ore production increases. The commodity has already lost 30% of its value since the beginning of this year.

European ‘Dick-Tators’ and volatile optimism.

Not a misspelling but a reminder that even Draghi is not immune from political attack as he began speaking on Tuesday afternoon. The protestor accused him and his fellow eurocrats of dictatorship , the attack akin to being flogged with a feather duster (the young lady used confetti) I am not sure what Draghi had to recover from. Maybe his conscience. The speech was seen as rather upbeat as far as hopes of recovery are concerned but with little doubt of QE continuing on a long term basis until recovery and inflation on track. He also confirmed that emergency funding will continue to support the Greeks.

It is true that Europe has seen some improved data. But there is a long way to go before that can be used to identify a recovery. The IMF have warned of stagnation. GDP speaks for itself despite recent enthusiasm.

Add to this the continuing decline of the German Bund. Not much sign there of optimism.

Did the ECB Chairman Blink?

At the IMF meeting Draghi has this weekend made another speech confirming that the Euro is a one way process and that there is no exit for any member country.

At the IMF meeting Draghi has this weekend made another speech confirming that the Euro is a one way process and that there is no exit for any member country.

This will no doubt bring even more confusion to a market place trying to factor in the effect of this possible black swans.

And what is Mr. Draghi’s strategy?

Can not now the Greeks default without exit?

Endless decisions stretch out to the Greek government. Pensions and wages have to be paid and another IMF instalment will quickly come due in early May. The pressure is growing as Obama joins the ranks (clearly concerned with a growing interest from Russia) calling for the Greeks to come to terms with their ECB partners. So far they stand firm in trying to honour their election promises as they see it.

Marc Faber, editor of the Doom Boom and Gloom report (more doom and gloom than boom) and a respected Swiss economist, invited them to default. As he points out, ‘’even if Greece grows at 10 percent per annum for the next ten years, it will not be able to pay its debts back,”

The IMF forecast this year was 2.5% and then on Friday they warned of a significant downgrade.

The poetic epithet of the great Greek hero Ulysses (Odysseus) was in the words of Tennyson, ‘to strive, to seek , to find and not to yield’. Oh how they need him now there is another Trojan horse to tackle.

Democracy redefined

Politics has become complicated thread in the economic fundamentals. The European Troika are dictating the policy for its periphery members, is at best a dilution of democracy and at worst an imposition. There is small wonder that extreme parties are appearing in all the member countries of the EU. It has Mr. Cameron, the PM in the UK offering a referendum on European membership and the UK are not even members of the the Eurozone, only of the Union.

In the UK as we approach an election another perspective of the democratic system is unfolding. And one which could do significant damage to the economy. The old favoured 2-party system is simply not functioning. The party who wins, and by all projections it will be a very close run decision, will not have a majority big enough to execute a mandate and will be forced to coalition with another party. All the options are extreme, with the centre Liberal party unlikely to return many members. One of those extremes is the SNP having lost the independence vote now looks well placed to ‘break’ the union another way. After the last election and the Conservative/ Liberal coalition, the GBP strengthened. There is not much chance of this happening after May 7th.

What to look for in The Week Ahead

It is still a question of Euro weakness, sentiment remains bearish and there are some levels to watch.

During the weekend the Chinese cut the reserve requirement, a liquidity tool which will bring 1.2 trillion Yuan into their ailing economy. Expect the Aussie to strengthen on this news.

The commodity currencies are benefiting from the correction in the index

In this context we also have to watch the Oil market

The USD is still a long but we need to know the correction is over, so it is now vital to watch the index

Pairs on the Radar

EURNZD holding with profit locked in

EURAUD, , short

EURCAD short but watch oil!!

The watch and wait list. (USDX Correction completion)

GBPUSD, Short

EURUSD, higher level short (1.10)

USDSGD long at lower level

Watch and wait (oil index reversal )

USDCAD , lower buy

NZDCAD long

This Week’s Calendar;

NZD CPI just after market open

AUD monetary policy minutes, Tuesday

German Economic Sentiment

Chinese and European PMI and GBP retail sales on Thursday

USD durable goods on Friday

There are meetings in Europe to look out for including a meeting to discuss Greece and always worth watching the crude oil inventory numbers from the US every Wednesday.

And as for those grey ugly ducklings , watch how they grow …

And as for those grey ugly ducklings , watch how they grow …

and they are swimming on choppy waters.

Judith Waker

0 Comments