As we awaited the decision of the Greek people on Sunday,we may have pondered the outcome and attempted to predict the consequences of the either/or decision. But it was never as simple as that; which is why this week ahead is a real step into the unknown.

As we awaited the decision of the Greek people on Sunday,we may have pondered the outcome and attempted to predict the consequences of the either/or decision. But it was never as simple as that; which is why this week ahead is a real step into the unknown.

The only thing we can prepare for is a black-swan event but what havoc it may reek is unforeseeable.

One thing is sure, it is politics that will ultimately define European recovery or its failure. So too will it decide the same on a global level. Western politics are driven by democracy….supposedly. Sometimes we see the thin veil exposing something very different. Democracy has been the cause of war, lost life, atrocities in it’s own name and of inspiration and courage.

Definitions continue to blur as vast corporations increase their control in the larger western democracies and now in Europe the manoeuvrings of our unelected gang of three has brought about an inevitable national stand-off. Whether or not the people of Greece submit to the European sentence of unsustainable debt and increasing ramifications of austerity (slow death) or stand with their government on the principle, and the hope for a new agreement with the ECB (or potential sudden death) the stage has been set for further tragedies including the EZ itself.

The ironies and the hypocrisies continue to build. The IMF (quickly alighted on by the Greek Finance minister, Varafoukis) this week admitted that the debt was unsustainable and that debt reduction was necessary if Greece was ever to recover.

‘’ Given the fragile debt dynamics further concessions are necessary to restore debt sustainability”.

Did you hear that Mr. Juncker, Schauble…anyone ? They are not willing however to transfer the debt ‘back’ to the private sector. Well thats hardly a surprise but a confession of sorts.

Global Forex; A European House of Cards

In 2010, an IMF working paper on public debt (Kumar and Woo, 2010) talked of ‘’ the potential risk of higher long term debts may discourage capital accumulation and reduce economic growth… they underline the need to take measures to not just stabilise public debts but to place them on a downward trajectory in the medium and long term’’

Also in 2010 the ECB itself weighed in with a working paper on the ‘Impact of High and Growing debt on Economic Growth, ‘’ This analysis…unveils a relationship between public debt and the economic growth rates at debt levels above the range of 90% -100% of GDP”

Here is a current European list of countries with a debt to GDP ratios over 100% and the inherent warning that Greece will not be the last of the EZ problems;

Portugal

Spain

Italy

Solvenia

Belgium

Ireland

Cyprus

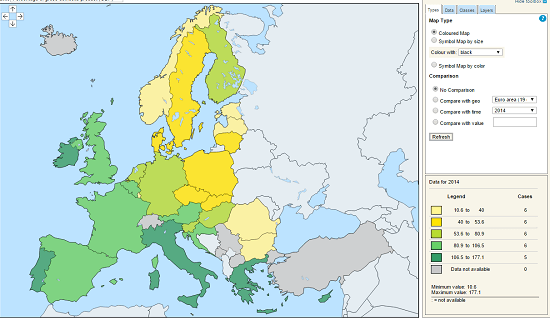

Here is a debt map published by the Eurozone’s Eurostat the dark green areas exceed the 100% level, thje light green 90-100%,

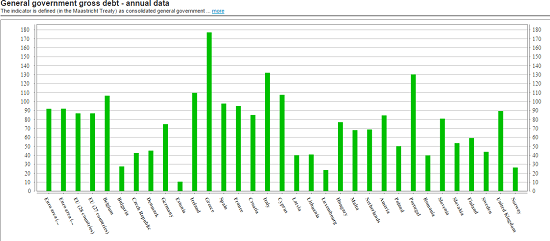

And this is how the EU stacks up in terms of debt to GDP;

In the Maastricht treaty of 1991, government debt to GDP was limited to 60 % . Some applicants did not qualify but were admitted if they were reducing the debt.

And then there is the debt per capita, that is the amount of public debt by population… this a global comparative

Japan, 99725

Ireland 60356

US 58604

Singapore 56980

Belgium 47749

Italy 46757

Canada 45454

France 42397

UK 38938

Switzerland 38639

These are the top ten, in fact Germany is at number 14 with 35881

The US numbers show that despite growing populations the debt levels are out pacing at an alarming level with 12000 per capita in 1990.

Of the G20 nations the Eurozone has a public debt of 14.8 trillion , the largest with the US second with 12 trillion.

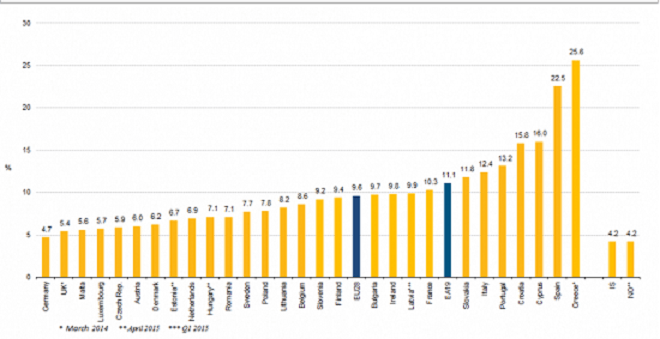

And more on the subject of why austerity cannot help as now the IMF have rather belatedly admitted; Eurozone unemployment stats as at May 2015;

Even if somehow a deal can be forged following the referendum in Greece, it is simply pushing the problem another 6 months down the line. The people of Greece will suffer either way. And the next? Spain Italy and Portugal ready in the wings.

Global Forex; Bad News, Worse News

China. Yes a severe fall in the Shanghai and Shenzhen equity markets which are still overvalued. More master manipulation here as the Chinese government have appealed via media and every means possible for its population to use savings or worse raise loans to patriotically support the country by buying into equities thus extending the wealth illusion. Result , a bubble which is bursting. Underlying growth is not evident. Last week the Manufactureng PMI advanced slightly on the month before but remains below the magic 50 level that divides economic growth from economic contraction.

A staggering 2.8 trillion USD has been wiped off the Chinese equity market in under two weeks.

The Chinese authority have blamed foreign intervention and short selling for the collapse and are searching for means to prop it up, including state owned pensions buying up swathes of shares but with no signs of underlying fundamental growth and over valued and over-leveraged markets it seems like just a matter of time before the next layer collapses.

The global effect of a Chinese tumble needs hardly to be stated . Emerging markets have the greatest vulnerability, especially the SGD. Commodity countries will also suffer the effects and this quite apart from any assessment of the risk appetite in the global context.

Global Forex ;Sentiment Watch

This week has seen a further descent into a risk-off environment which should not surprise us. Whether this establishes itself is what we should now monitor;

1: Equities

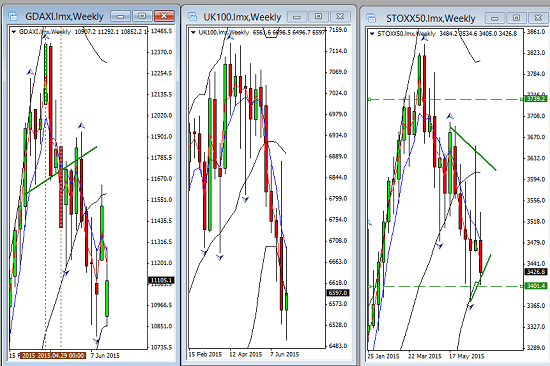

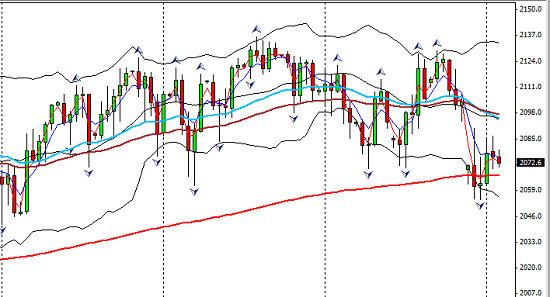

In Europe the equities showed the nerves starting as they did with the opening gaps last week following the enforced closure of the Greek Banks. These are on a weekly chart so as to remove some of the volatility noise;

In the US the same phenomenon, this time a daily chart of the S & P;

The market is toying with the 200EMA

- The Bond Markets

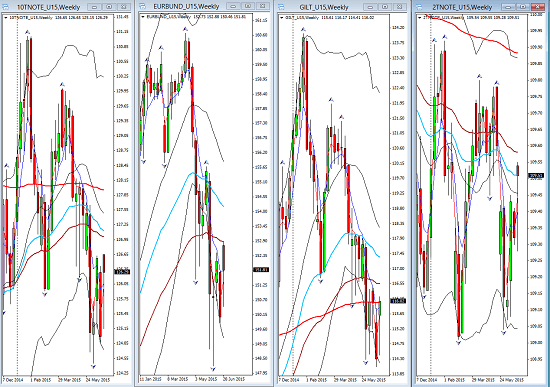

In the Eurozone, bond buying led to a contraction in the yields,

Here is the comparison which includes the UK gilts, again on the weekly perspective;

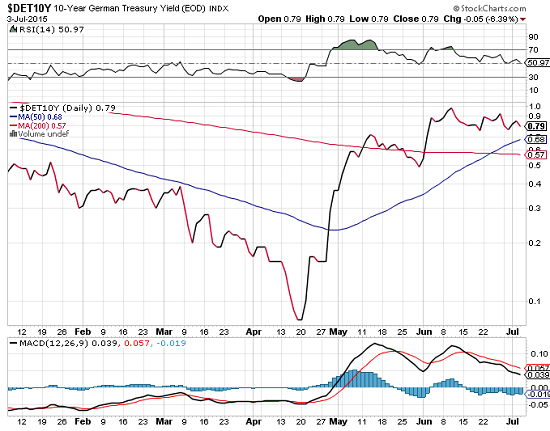

And the German 10 yr yield, chart courtesy of stockcharts.com;

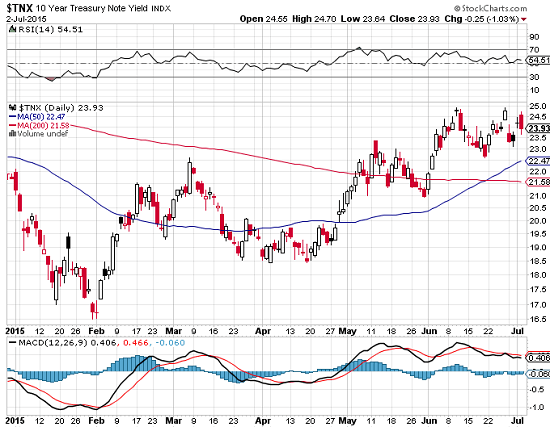

In the US treasuries, again yields gapped downed recovered somewhat but closing down on the week;

The recovery was no doubt affected by the disappointments brought by NFP employment change missing the number even though unemployment showed improvement. Consumer confidence also returned a good number, so it wasn’t all bad news. The rate hike anticipation will have been dulled and the data watch will continue as will the speculation.

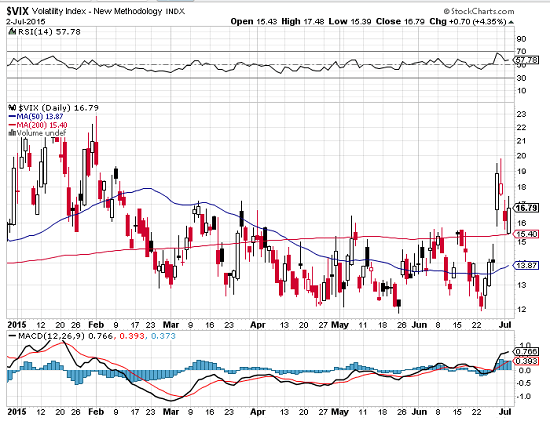

- The VIX and VSTOXX

Another gap for the S & P fear index closing above the 200EMA

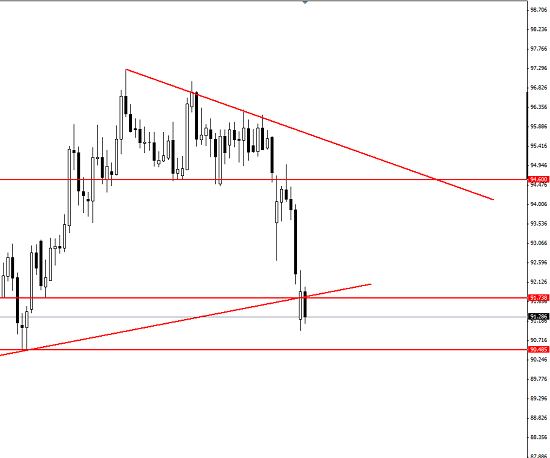

The Euro version, Vstoxx, looks even more nervous;

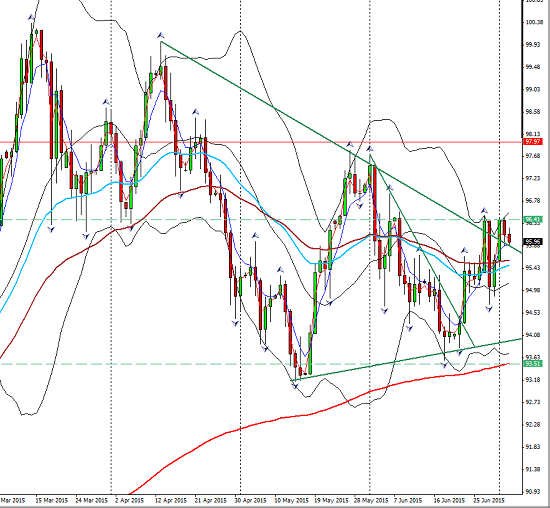

- AUDJPY

The sentiment pair;

Technically a very bearish scenario, and not a surprise in the light of shocks from Greece and particularly China.

The Global Economies in Review

The USD

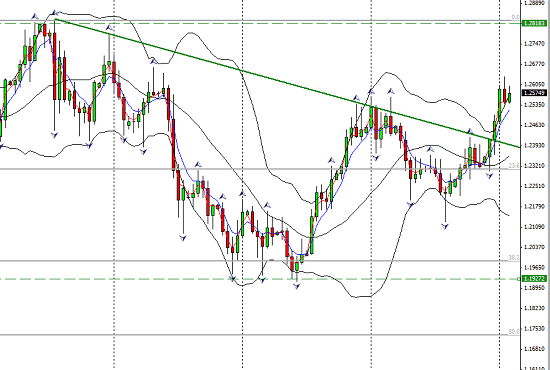

I have already reviewed last week’s calendar above. The rallies seen of late were halted on the NFP news including the Canadian dollar and the Singapore dollar. The Euro also advanced. The index pulled back to an interesting level;

There are many factors to account for in terms of USD recovery and it’s standing going forward. The USD is, as we know well, the leader of the rate hike pack with the UK behind it. The risk environment will lend strength if risk aversion sets in and it is seen once again as a safe haven. It is also true conversely that the European crises could undermine it, but that does little to change the comparatives. There will be opportunities for longs as pullbacks materialise on any weakness from the US data.

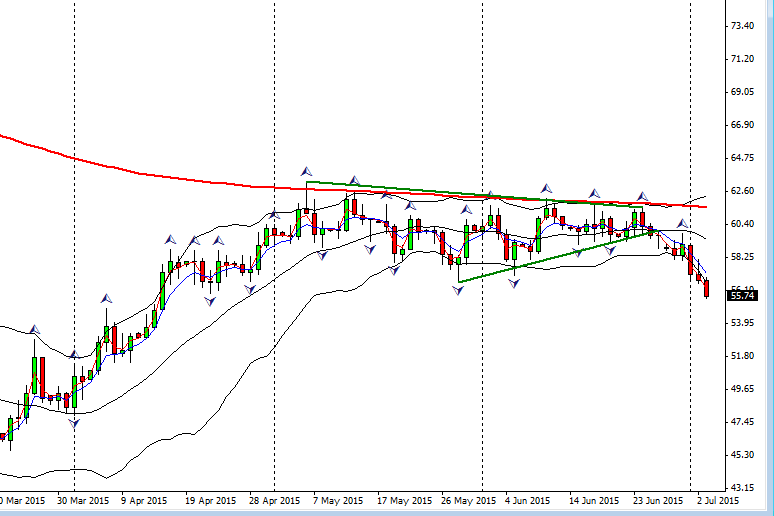

The Aussie Dollar

Sharp declines on Friday were apparent as retail sales and trade balance piled on top of concern over the Chinese rout and new lows in iron ore prices which has dropped 11% in one week. With a changing risk environment the slide could continue. This will be good news to the RBA who have long since shared the opinion that the Aussie is too strong.

On a technical level a head and shoulders broken Friday on any interpretation!

The NZD Dollar

Another bad dairy number for this commodity currency also under pressure. Prices further slid a surprising 10.8%,with speculation of rate cuts enhanced. This remains bearish but somewhat overextended.

The Canadian Dollar and the Oil market

Not a good week for crude but it did attempt a brief rally on Friday following the NFP numbers, but did not disturb the recent downtrend;

The outlook is unsettling to say the least. Quietly this week, oil rig counts in the US increased again. The fall earlier in the year did not greatly impact the recovery in oil prices though certainly buoyed them up a while.

Also significant is the low point in the rig count was as early as February;

For the Canadian dollar, weakness has been apparent especially against the USD and the GBP. NFP halted the move against the greenback as one would expect. The prognosis going forward remains bearish.

The UK

A week of PMI results, with manufacturing missing the number, improved on Thursday and Friday with up beat numbers in construction and service PMI . Marc Carney this week spoke of risks spilling over from the Greek crisis, and possible contagion in the financial markets. He also said protections had been put in place to cushion the UK economy. A warning was added, that if the EZ did not create a firm monetary union after this crisis, whatever the outcome, then UK exports would be sapped.

That may be some time off but the markets aware of the medium term downside will affect the GBP with the same uncertainty that all markets are currently exposed to. The GBP has its best strengths against the commodity currencies and long opportunities continue there.

The Week Ahead

A week destined to be dominated by the Greek referendum, there will be opportunities to so exposed to the volatility that we may expect to experience at least in the first half go the week. The other possible catalysts are;

A week destined to be dominated by the Greek referendum, there will be opportunities to so exposed to the volatility that we may expect to experience at least in the first half go the week. The other possible catalysts are;

Monday; CAD PMI, ISM US Manuf. PMI (very big number for the rate hike speculators)

Tuesday; AUD rate decision and statement from the RBA Watch out for this in the light of recent news flow! , also CAD and US trade balance

Wednesday;

The UK budget, US FOMC minutes (always illuminating!)

Thursday; Australian employment data. Chinese CPI (inflation indicator) UK bank rate and statement, US unemployment claims

Friday; CAD employment numbers and a speech from Yellen, the FOMC chair, with expected economic projections at a Cleveland Forum.

In Conclusion, a Red Flag Week Ahead

The Decision in Greece looms large and much more at stake than one European nation. Whatever it is the uncertainty is not set to end anytime soon either for Greece , the EZ or the global financial community. A tidal wave takes time.

The Decision in Greece looms large and much more at stake than one European nation. Whatever it is the uncertainty is not set to end anytime soon either for Greece , the EZ or the global financial community. A tidal wave takes time.

There was time when only those reading the ‘conspiracy theory’ press would be expressing alarm at what the consequences may be to the ramifications of the Euro-Greek crisis, ‘ Doom and Gloom’ is fast spreading to more conventional circles.

The days of boom and bust economic swings have morphed into unpredictability and uncertainty thanks in large part to central bank intervention and a growing global public debt.

Volatility will most likely continue for some time yet and we should look for increased signs of risk aversion, be prepared for them, and trade appropriately and profitably with them.

This is a red flag week like no other, which could lead us to many more unless we can begin the arduous task of eradicating the hypocrisy, loosening the grip of corporate manipulation and once again seek the democracy that was born to serve us all.

Judith Waker

0 Comments