While Draghi’s was announcing the late arrival of QE to bring the Eurozone back from the brink of its deflationary trajectory, Christine Lagarde was in Davos preparing her speech notes for the World Economic Forum warning that this is the year ‘to strive for economic growth or accept stagnation; to work to improve stability or risk succumbing to fragility; and to cooperate or go it alone’.

And her answer? Global cooperation overseen by institutions such as the IMF and fiscal reform country by country, with policy ‘focused on promoting growth and creating jobs’, including closing the gender gap.

And here is her warning if we mess up; ‘The global economy risks getting stuck in a “new mediocre” – a prolonged period of slow growth and feeble job creation’.

Lagarde continues to see the US as the bright spark in an otherwise lacklustre outlook for the global economy and included her own expectation that the US is more likely than not to raise rates by the summer of this year. She gave praise to Yellen for communicating with the market (still probably bemused by recent lack of transparency shown by the SNB), and for a terrific job as FOMC chairwoman , with some infant signs of inflation and a strengthening jobs market.

The QE Potential for the Eurozone

Ironically for Legarde, the ink was barely dry before the pre-QE tensions between Germany’s Merkel and the ECB chairman started spilling into the press. Draghi did please the market with the amount of the liquidity announced on Thursday which amounted to 60 billion per month for at least 18 months. There is, however, a lot of confusion as to the mechanics and whether it can even be effective in such a disparate union.

Ironically for Legarde, the ink was barely dry before the pre-QE tensions between Germany’s Merkel and the ECB chairman started spilling into the press. Draghi did please the market with the amount of the liquidity announced on Thursday which amounted to 60 billion per month for at least 18 months. There is, however, a lot of confusion as to the mechanics and whether it can even be effective in such a disparate union.

Germany’s concern remains; structural reform is necessary to support the monetary policy. And, indeed Draghi himself is only too aware of this as he expressed it ‘monitory policy can create a basis for growth, but for growth to pick up you need investment and for investment you need confidence and for confidence you need structural reform’.

The Germans have their issues with Draghi and the QE debate which the Greek situation is not helping. The new government may be demanding debt forgiveness and Germany is their biggest creditor. The German press have already referred to Merkel’s preference for Grexit rather than concessions to the debt.

There is a growing feeling that the German stance can derail or at least undermine the momentum that QE was intended to bring to a zone perilously close to deflation with a chairman intent on deflecting it.

Forex Outlook for the Euro:

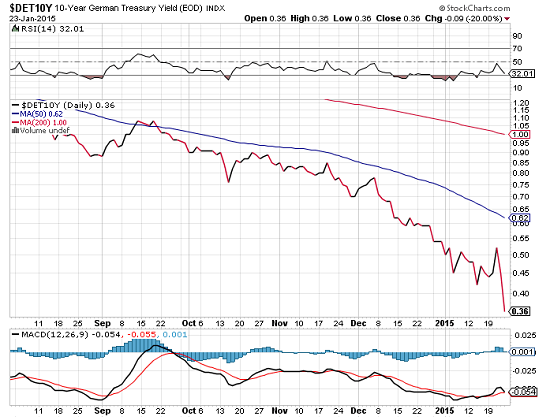

As the ECB are now planning to buy bonds from Eurozone countries, the effect will be for bond yields to fall. They are already at record lows . The following chart is the German 10yr Bund yield in what is now a steep descent;

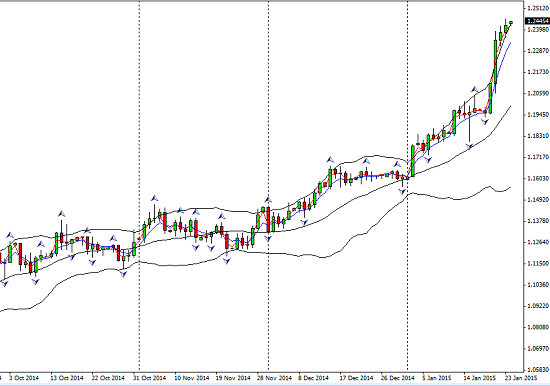

The effect may be for the Euro to continue its descent maybe to parity with the USD. Bear in mind that the inflation target which is currently negative has a very long journey to reach Draghi’s 2% target . The chart shows the gap on Sunday’s open ;

Beneficiary Markets of ECB QE

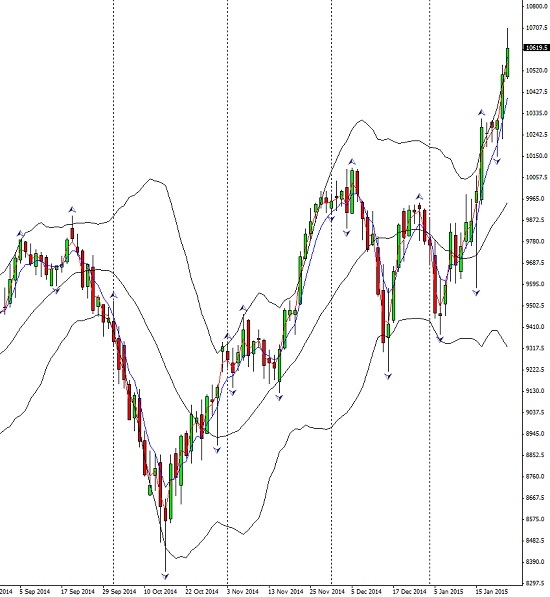

European equities will benefit from the available liquidity the Central Bank is providing. This has already been seen in all the European bourses. Here is the Dax:

The FTSE had a strong week, pulling back slightly on Friday.

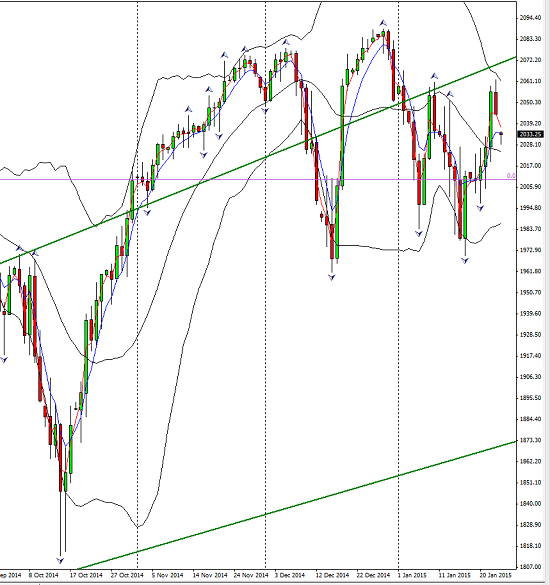

US equities should also benefit. Here is the S&P on a daily chart again showing the Sunday gap on Greek news;

With bond yields in the Eurozone so low the comparative yields in the US will attract US Treasury buyers and that in turn will bring US yields down.

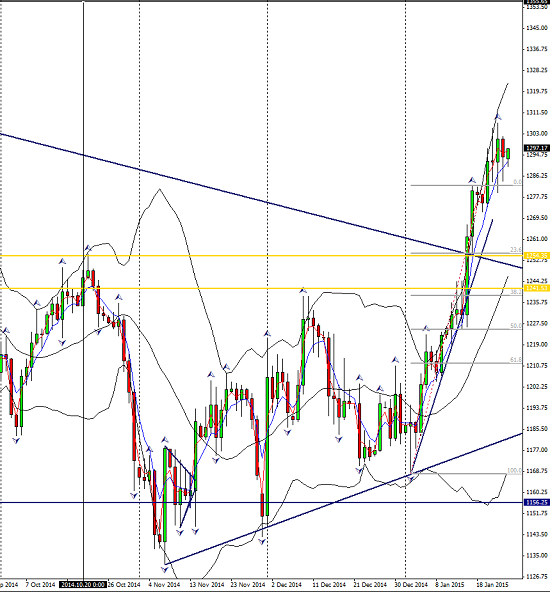

Gold has had 2 strong weeks and although it has not been as reliable as a safe haven, it is certainly showing renewed strength and a return to its old status. Another chart with Sunday’s open;

A USD update

We have been aware of late of a more dovish tone in the FOMC , of talk of putting back the rate hike which is anticipated as monetary policy is tightened and as recovery begins to build momentum. It is early days and data has shown some delay particularly in the arena of wages and thus the reticence can be understood.

As we have seen, Christine Lagarde has optimistically predicted the summer as was the original goal. Data this week again was disappointing with building permits down (although housing starts were up) Employment numbers missed their target as did flash PMI.

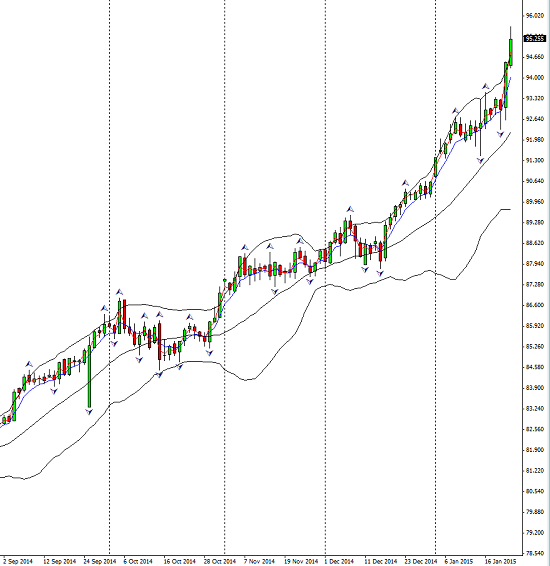

The USD forged ahead this week on the ECB news; the chart is the daily USD index;

There is an all important FOMC meeting on Wednesday evening in the trading week ahead. Also from the US, consumer confidence GDP, unemployment claims and durable goods, but the catalyst is the FOMC and thus the focus for the week.

How Monetary Policy effects Forex

Dovish Tendancies

We saw last week the BOC make a surprise decision lowering the rate to 0.75%. This surprised many and showed another central bank without forward guidance. The Canadians have a potential housing bubble which the rate cut will exacerbate if the retail banks follow with a cut in the prime rate.

Here is the USDCAD chart;

Was there justification when their core inflation rate is above 2%? Oil is the issue and oil companies have already suffered but the Canadians do benefit in many other sectors from low oil prices. The double edged sword again.

This week it is the turn of New Zealand to take the policy stage. Let us watch to see if the trend continues.

In Australia the important CPI number and PPI this week . These numbers will affect their policy decision

Sentiment and Volatility.

The VIX is an index of S&P 500 volatility and fell back this week to 16.03, a comparatively low level. Here is the daily chart courtesy of stockcharts.com

However , this is just one equity market and volatility has been increasing elsewhere and likely to continue . There have been some dramatic events already this year and this week was no exception. Furthermore that the market liquidity once on offer from the Federal reserve and the BOE is now in the hands of the ECB which has inherent unpredictabilities. We have discussed before the possibility of QE having very different mechanics in the complex structure that is the Eurozone. Uncertainty there for sure.

Greek election results gave the left a ‘win’ but a whisker short of a majority and holding hands with the extreme right! The whole question of debt (which between the ECB in 2010/2011 and the IMF loans amounts to 350 billion) will be the next major European issue, both in economic and political terms. We know the opinion in Germany and the ECB but just how it will play out, remains another factor giving rise to yet more uncertainty.

It should be noted that Mr. Draghi made a condition in the new round of ECB bond buying, that it will not apply to Greece unless they pay the 2010 loan of around 27 billion euros.

The other significant news for the week was the death of the Saudi Arabian King, at first giving rise to a brief rally in the crude oil price, as speculation started as to the Saudi heir’s potential to change the policy. The considered view is that he won’t. Oil has fallen to fresh lows ;

The commodities Index also continued its decline; (Stockcharts.com)

Proceed with Caution;

Geopolitical concerns continue to rear their heads, with the French attacks, the Jihads back in the news, the Greek election and Ukraine unrest (again) which has done nothing to calm Angela Merkel, we can and should expect volatility to rise and sentiment to shift.

Geopolitical concerns continue to rear their heads, with the French attacks, the Jihads back in the news, the Greek election and Ukraine unrest (again) which has done nothing to calm Angela Merkel, we can and should expect volatility to rise and sentiment to shift.

Equities for the moment have reacted and benefited from the ECB, regarded as a conservative Central Bank, casting caution aside and entering the realms of QE following in the foot steps of many other global economies.

However, the growing sense of risk aversion becoming apparent may end that party at any time . If geopolitical events continue to increase or worsen, beware. They along with loosening and tightening monetary policy are the catalysts but sentiment is the test tube environment in which ultimately all market experiences are measured.

Traders dislike uncertainty and uncertainty breeds volatility. Every news release from Lagarde and the IMF to the FOMC, from Merkel to Draghi, to politics and war creates that little more . To paraphrase the great Bette Davies ‘ fasten your seat belts, its going to be a bumpy year’!

Judith Waker

0 Comments