There have been two main themes for a while now; The US rate hike speculation and the economic situation in China. So that is what we will focus on today.

We had our answer from the Fed and it presented somewhat weaker projections for the USD, but this was followed by hawkish statements led by Janet Yellen. Then NFP data burst their bubble. The major theme of US tightening took the limelight again last week as the market awaited the Friday labour statistics from NFP monthly numbers. Always data that can move markets and cause caution and volatility, it presented itself this month as a catalyst in what has become a nervous and uncertain marketplace. Of course the two on-going themes in global macro cannot be separated and in considering the implications of the data we saw on Friday, the Chinese economy has to be part of the equation in any predictions from here, either of direction or more importantly sentiment. The brief part of the week left for reaction to the numbers was unambiguous in terms of the Bond market but less so in Equities and we saw again, familiar whipsaws as the post announcement gave way to digestion of the data and its implications. .

We had our answer from the Fed and it presented somewhat weaker projections for the USD, but this was followed by hawkish statements led by Janet Yellen. Then NFP data burst their bubble. The major theme of US tightening took the limelight again last week as the market awaited the Friday labour statistics from NFP monthly numbers. Always data that can move markets and cause caution and volatility, it presented itself this month as a catalyst in what has become a nervous and uncertain marketplace. Of course the two on-going themes in global macro cannot be separated and in considering the implications of the data we saw on Friday, the Chinese economy has to be part of the equation in any predictions from here, either of direction or more importantly sentiment. The brief part of the week left for reaction to the numbers was unambiguous in terms of the Bond market but less so in Equities and we saw again, familiar whipsaws as the post announcement gave way to digestion of the data and its implications. .

Profit From Knowledge:Lift Off From Zero

The market now accepts the likelihood of US policy changing before year end as moving from doubtful to implausible. To consider dates in 2016 is to get ahead of ourselves even if the speculation will develop as time unfolds, but now for many the spectre of deflation is haunting the trading places. There is a growing awareness that monetary policy simply hasn’t or isn’t doing its job. The Eurozone statistics on Wednesday saw inflation fall to minus 0.1%, the first negative result for six months, the ECB citing energy as the negative influence.

The market now accepts the likelihood of US policy changing before year end as moving from doubtful to implausible. To consider dates in 2016 is to get ahead of ourselves even if the speculation will develop as time unfolds, but now for many the spectre of deflation is haunting the trading places. There is a growing awareness that monetary policy simply hasn’t or isn’t doing its job. The Eurozone statistics on Wednesday saw inflation fall to minus 0.1%, the first negative result for six months, the ECB citing energy as the negative influence.

More worryingly with their emphasis on the manufacturing sector, not to mention the Volkswagen scandal, Germany posted consumer prices that failed to rise. Ironically the US delay on rate hikes and the confirmation this time in the data rather than the rhetoric that this may well occur again makes it more likely that both the ECB and the BOJ will soon be forced into more easing. The daunting possibility of monetary policy failure and its implications is a concern we have to kick down the road with the Fed interest rate ‘can’, but the risk in terms of sentiment for the medium and long term cannot be denied and certainly should not be overlooked.

A Closer Look at The Numbers

The underlying growth is still there in the US, with jobs being added. The problem is that it is without any doubt slowing and once again falls in energy prices have been the major culprit. The number was not a slight miss of the expectation, it was a significant one. Add to this the downwards revision of July and August numbers which is against historic trends, and the ramifications come into focus. Furthermore wage growth was zero and stagnation evident. There has to be growth here before the Fed can reconsider the tightening cycle Finally in the US this past week, we should not ignore the all important ISM manufacturing number that came out on Tuesday was also below expectation and at 50.2 dangerously close to that magic 50 benchmark. It doesn’t help. The USD has somewhat got ahead of itself this reflected in the Index drops on Friday

;The Market Interpretation

There is a difference between reaction and response, and Friday was all about the former, of course the weekend will bring reflection and the early week sessions will provide a clearer picture.

The Bond market had its own very clear statement; here is the 10 Yr bond down 8 basis points on the day, 13 on the week although it has to be said that it recovered from it’s lows late in the session;

Bonds globally rallied into the close. Equities started with a hefty move down which reversed in the afternoon and closed on highs,The S&P is back inside the daily range (see chart below) , and It took euro stocks with it. Gold enjoyed the news;

Oil remains in a tight consolidation;

The Commodities index shows little reaction, copper slid on the news but recovered in late trading and the index remains tightly bound in a range which begs the question what next? It is difficult to see how any rally can be sustained in an environment of global deflationary headwinds, but for now and the short term we may see a move higher.

In The week ahead we know what we have to watch, the commodities the emerging markets, the Vix the Oil market and the USD Index, but what should we expect?

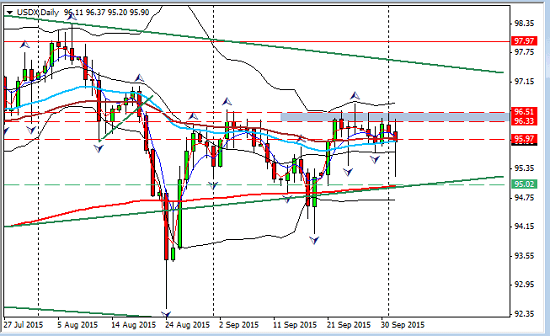

The USD index fell as one would expect;

Profit From Knowledge : The Calendar and Opportunities

A quick word about the GBP. With a solid construction PMI number and an acceptable manufacturing one (in line with expectations) we can look forward to the services PMI first thing on Monday morning (London session). A large part of GBP GDP is reliant now on the service industry so in comparative terms this is an important piece in the puzzle. It has had a downward bias and the news from the US may prolong this so the meeting on Thursday and Mr. Carney’s language is all important. There may be some rallies to be had in the GBPUSD, but beware of the BOE on Thursday. It is unlikely to move on rates but the monitoring of its dovish/hawkish tone is essential and no guessing allowed! It could pave the way for a bullish or bearish run so watch this one carefully.

The RBA on Monday left rates unchanged and did not change their view that it was appropriate. The market saw this a bullish for the Aussie dollar. We have the BOJ on Wednesday. Another potential language week. There is reason to look for shorts in the USD index whilst it re-adjusts to a less optimistic outlook on growth and rate prospects but with sentiment capable and justified to swing into aversion this has to be very cautious.

The USD index of course took it’s ‘hit’ on Friday as one would expect and Monday should reveal the potential of any downside activity that could be exploited in the near term.

The main focus this week is to watch for weakness in the Euro. The EURUSD, needs pullbacks for shorts, the EURAUD is the preferred candidate against the commodity currencies as they continue to improve whether or not the ‘bottom is in or they are simply in a relief rally.

Gold moved up in the wake of US disappointment, so that is one to watch alongside the USDX and the Oil market will offer positions when it breaks from its range. Oil is always a necessary part of the monitoring process and risk on is very reliant on nothing negative appearing in these very sensitive markets.

I will continue to look for shorts in the S&P 500, although how it behaves in the first part of the week will show if the rally from Friday has legs; and shorts also against the USD (temporary) trend, again I prefer to trade the index. , the exception is longs in the USDSGD, although there may be some advantageous pullbacks if weakness in the dollar follows through.

For currency traders volatility both provides dangers and opportunities in equal measure. I prefer to see the dust settle and to gather some additional perspective. That is my preference every week but NFP has increased this necessity, of course with a keen eye on the Vix to see if volatility is building again. It has already dropped this week below that 20 average.

For currency traders volatility both provides dangers and opportunities in equal measure. I prefer to see the dust settle and to gather some additional perspective. That is my preference every week but NFP has increased this necessity, of course with a keen eye on the Vix to see if volatility is building again. It has already dropped this week below that 20 average.

Despite the easing of worries in China, the data we have seen just in the last trading week is enough to remind us that deflation is still the danger and the black cloud that hovers above the fragile recoveries in the US and the UK and continues to undermine them. If that continues to infiltrate the US statistics, it will become harder to sustain any optimism for quantitative easing guiding us back to an inflationary environment. Whilst the USD has to take its medicine, in the bigger picture the consequences for the emerging markets and the commodity currencies is much more concerning. For the moment we can trade the relative calm and the improved sentiment. How long it lasts is another issue I am sure we will be debating!

Judith Waker

If you would like to learn how to trade like a professional check out our 5* rated forex mentor program, RISK FREE; by clicking on the “Get Started Today” Button below

0 Comments