As we moved through yet another week of volatility and increasing unpredictability, the contrast between the US and its steady even if not impressive progress towards recovery and that of the world economies becomes more defined than ever.

Speculation on the commencement of the US tightening cycle continues apace and following Fischer’s comments last weekend at Jackson Hole, there were indeed further signs of improvement. It was data bag with enough mix to entertain doubts for the decision to be made at the upcoming September meeting. But its not just about data anymore and imperceptibly we have slipped from data dependence to global economic impact considerations. At least as far as the speculators are concerned. .

Speculation on the commencement of the US tightening cycle continues apace and following Fischer’s comments last weekend at Jackson Hole, there were indeed further signs of improvement. It was data bag with enough mix to entertain doubts for the decision to be made at the upcoming September meeting. But its not just about data anymore and imperceptibly we have slipped from data dependence to global economic impact considerations. At least as far as the speculators are concerned. .

There have been encouraging signs, from the EZ in particular but as we have discussed here, the ECB who can not afford to let the Euro become too strong and compromise what one can only describe as fragile beginnings, stepped in on cue. The UK has taken a backward step and certainly has evidence of downward inflationary pressure from outside forces.

So in truth the economy on the ‘other-side of the divide is China, whose recent problems affect not only those close neighbours who represent some of the many ailing emerging markets and the commodity currencies such as Australia but the precarious state of global inflation.

So in truth the economy on the ‘other-side of the divide is China, whose recent problems affect not only those close neighbours who represent some of the many ailing emerging markets and the commodity currencies such as Australia but the precarious state of global inflation.

The two are now so intertwined that considering Fed policy without the ‘great fall of China’ is folly. If your crops are improving on an annual basis you still have to watch the weather cycles or as John Authors quipped in the FT, they are not so much data dependant now as market dependant.

Finding An Edge: The Week’s round-up

Duality and ironies abound. The IMF weighed in again this week and are proposing to lower global rate forecasts.

The G20 are however upbeat in their statement, seemingly shrugging off the IMF fears and the BOJ going as far as to say that a rate rise sends a normalisation to the market place and will be a positive for the world economies.

Bearing in mind that the state of play in Japan rests on a continuing QE, at first blush, that seems a little unexpected. Maybe one can see that the failure of the US to follow through sends a big global warning that dissinflationary forces are threatening the global recovery which may sink us further into a risk off environment. The Japanese are also aware that the JPY has been strengthening as it will in a fear based environment which doesn’t help their cause just as it doesn’t help Mr Draghi.

Drastic Draghi;

The Chairman of the ECB stepped up to the plate last Thursday, sparking another volatile session for the EURO. There was an anticipation that he was capable of taking measures to prevent the strengthening of the Euro but the extent of the dovish stance took the market by surprise. He is indeed prepared to do what it takes specifically with, ‘’size,composition and duration’’ of the current QE program. He could not have been clearer. The fragile growth in the zone is not to be put in jeopardy under his watch.

The Euro plunged;

The German 10 year bond fell back again as did the 2yr.

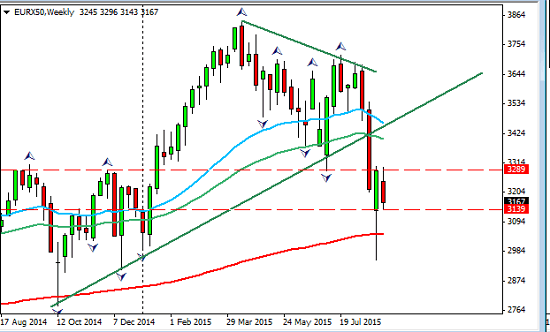

As for equities another risk averse week here illustrated in the Eurostoxx 50 using a weekly perspective;

Worth noting and no doubt reflected by Draghi’s rhetoric that the three EZ countries most affected by Chinese woes are Germany France and Finland; in that order and it includes their two biggest.

Damned If They Do and Damned If They Don’t?

The US rate hike ‘GPS’ is currently recalculating, so to speak. The labour numbers giving no clear direction. Not bad enough and not solid enough for a clear picture of the September meeting projections. So with these dichotomies and uncertainties we can continue to expect more volatility and unpredictability. That makes the market once again very difficult to handle this side of the Fed meeting on 17th. H

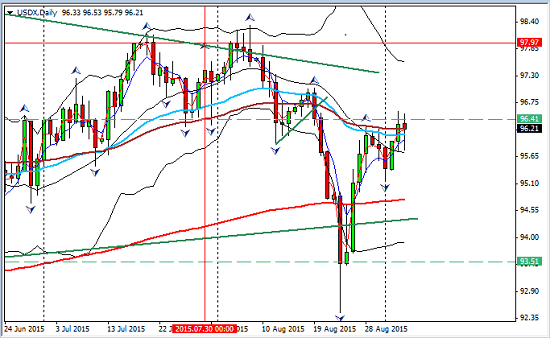

The effect of the numbers on the USDX was to strengthen initially but looking indecisive on the close. It faired better against the weaker currencies and already had a strong weak due to Euro Draghi-related weakness;

Of course the data gives justifications for viewpoints on either side of the bird pens (hawks and doves that is) and there are many examples. With the dollar strengthening over the week, we saw some optimism not only for the hike but for the general state of improving economic conditions in the US.

There are a few points to make. The wage data did edge up. And whilst the expectation was missed,, there was a net upwards revision of previous month’s numbers so reading the data immediately and the ‘reaction’ to it is not so easy. Furthermore the polling estimates on local returns of data of which the NFP number comprises was around 70% and thus open to future revisions itself. This is a vacation factor. All in all slow but sound progress was made.

There are still areas of concern including manufacturing PMI,

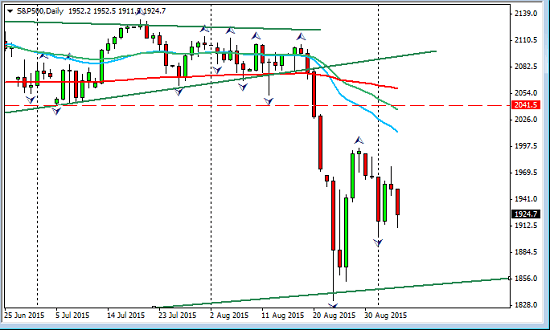

It is not all about the data as we have now seen. The SandP 500 had this to say;

So what are the prospects? Volatility looks set to continue with the meeting on the 17th September and we have a guessing game going on. It does seem that the equity markets are not just factoring in a rate rise which would normally be expected to cause a correction. It seems much more sensitive than that and a growing sense of risk aversion is emerging. What is interesting as far as US equities is concerned is that if the FED raise rates this month, they will exacerbate an emerging market crises, send a signal to the market that they are ok whatever happens elsewhere which has the potential to turn risk aversion into panic. If they don’t raise rates they are undermining the only confident economic recovery in the world… which sends out a similarly bleak message for global recovery. That keeps me on the short side of equities and the downside of the risk debate.

Ifs and Buts

The China effect, now dubbed ‘’the great fall of China’’ is still at the forefront of all these frantic projections as to how much stress this market can handle. There is an on-going concern that the Chinese manipulate their numbers (and have done so for a while) , in other words the situation could be even worse than feared. Here is an interesting stat; the World Bank estimate that a 1% percent decline in Chinese growth = 1/2 percent drop in global growth. Thus if as some researching economists estimate, China has overstated growth by 3% then the IMF’s reduced growth estimate globally of 3.5% would be reduced by 1.5% . Thats enough to spook any market. Of course that view has a lot of ‘ifs’ but as we are beginning to realise this current grossly distorted market place is awash with ‘ifs’ and ’buts’.

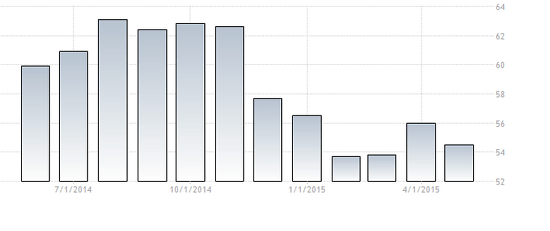

This is what Caixin PMI looks like on the numbers we have;

Risk is more on than off, volatility of volatility (what next you may ask?) is rising. Here is the VIX, well above the 20 historical average and very different from 6 months ago;

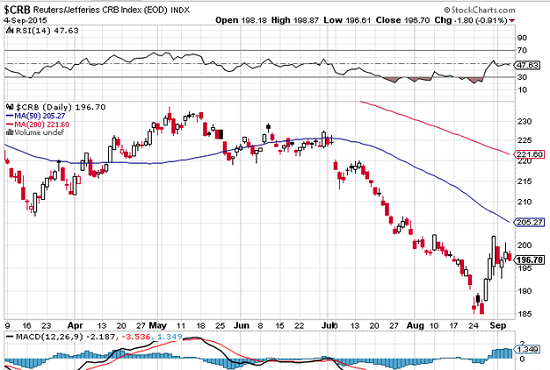

Commodities and Oil

Volatility also seen during the balancing of these markets as weary to ascertain if the low is in; here are commodities;

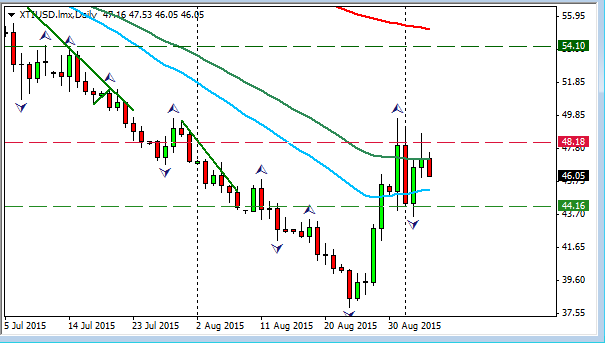

The oil market shows the same inclinations;

Finding An Edge:The Week Ahead;

Monday, a bank holiday in the US and Canada

Tuesday; China, trade balance

Wednesday; Manufacturing UK, CAD and NZD rates and statement.

Thursday ; AUD labour stats, China CPI. GBP rates and statement , USD unemployment, PPI and prelim conumer confidence

Finding An Edge:

It is a lighter week but do not under-estimate its potential. Rate announcements and the language of the statement can always move markets, and in such a nervous environment expect plenty of that. Dovishness is anticipated from the Brits this week so care advised! All indicators point to continuing unpredictability and swings. Once again I shall turn my attention to the indexes, S and P 500 for shorts and USDX for longs and will continue to look for long entries in the USDSGD which still trends upwards post NFP. Emerging markets continue to look threatened whatever happens. The equation of opposing forces+conflicting opinions+bi-polar monetary policy all adds up to more of the same, leaving long term plays much more attractive that the inevitable lottery of the shorter term time-frames.

In the meantime there is a distinct feeling now in the inter-connected market place that one straw is all it may take to break the global camel’s back. Deliberate interventions on a world-wide scale has left it very vulnerable.

Judith Waker

If you would like to learn how to trade like a pro check out our $1 offer by clicking on the banner below

0 Comments