Another week or market swings saw big drops and equally big corrections, risk-on disappeared on Monday to produce the biggest down day in the US equity market since August 2011. Come Thursday it swung back to risk-on as the markets regained their appetite. From optimism to pessimism and back again by week-end, from Fed hype to Fed doubt and back again, the scenarios played out repetitively. The volatility continued to weave its way through every financial market and is a factor we may expect to be around for a while whilst uncertainty and unpredictability co-exist.

Another week or market swings saw big drops and equally big corrections, risk-on disappeared on Monday to produce the biggest down day in the US equity market since August 2011. Come Thursday it swung back to risk-on as the markets regained their appetite. From optimism to pessimism and back again by week-end, from Fed hype to Fed doubt and back again, the scenarios played out repetitively. The volatility continued to weave its way through every financial market and is a factor we may expect to be around for a while whilst uncertainty and unpredictability co-exist.

So where does that leave us as traders? It does seem to be the case that short term trading is becoming something of a lottery. Many commentators have offered a variety of explanations including the reminder that the environment we find ourselves in is not so much about economic foundations but of central bank control and manipulation of the forces those foundations produce. As we become more data dependent and vulnerable to monetary policy and government interventions any element of modest predictability we may have had would by necessity, wane.

For all the above reasons, this week we will take a longer look at the USA the most liquid currency in the world, how it is faring and how it is perceived and also how it may take on board the global issues and politics that may intentionally or otherwise derail it’s recovery.

Forex Risks: What’s Up In the US of A?

There are three broad categories to consider when it comes to speculation about the strength of the USD and the recovery of the country’s economy and how should be handled. The first is Domestic Results, the labour market data (fasten seat belts again for NFP week) wage growth and fundamental improvements. The second is the question of Global Issues and how the unravelling in China may have effects across the entire globe that must include the US. The third is something of an add-on. The Effects of Zero Interest Rates may be seen as holding the economy back and the skewing of allocation of capital towards riskier assets. The FOMC might well be concerned with global issues but it may also not wish the uncertainty to continue.

There are three broad categories to consider when it comes to speculation about the strength of the USD and the recovery of the country’s economy and how should be handled. The first is Domestic Results, the labour market data (fasten seat belts again for NFP week) wage growth and fundamental improvements. The second is the question of Global Issues and how the unravelling in China may have effects across the entire globe that must include the US. The third is something of an add-on. The Effects of Zero Interest Rates may be seen as holding the economy back and the skewing of allocation of capital towards riskier assets. The FOMC might well be concerned with global issues but it may also not wish the uncertainty to continue.

We saw a robust 2nd quarter GDP last week and that was a major factor in the second half of the week recovery. Between April and June the economy grew at a rate of 3.7% against the estimate of 3.2%. In fact the first estimate was as low as 2.3%. So it seems the economy is growing faster than anyone thought. Add to this the core durable goods data which also beat the expectation at 0.6% and it was an optimistic week as far as growth was concerned. This had the naysayers reconsidering the September meeting as the first move on rates.

The jury is still out, the opinions very divided and strong in both camps and thus the speculation will continue until the 17th September. At least.

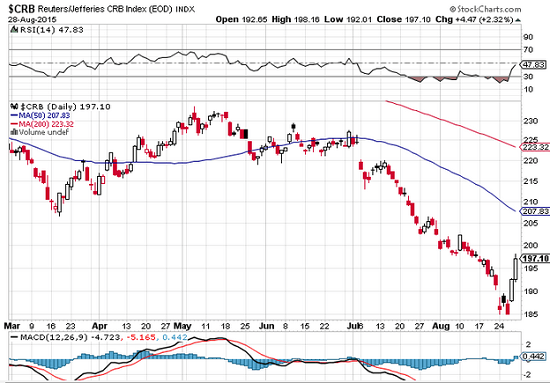

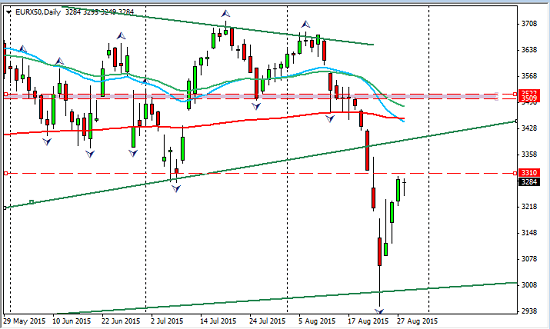

As for the threat of the Chinese, as sentiment shifted back the Shanghai index started to recover from Tuesday but still closing down on the week. Another rate cut was thrown onto the pot to help stem the flow with little initial effect but of course improvement followed .This month’s action still gives the speculators cause for concern; chart courtesy of stockcharts.com

The news from Jackson Hole centered around Fed reserve vice chairman Stanley Fischer as Janet Yellen was absent. It was clear from his address that despite the issues such as falling oil prices, global weaknesses and a strengthening dollar, there was no special concern about low inflation. On the contrary, he argued that the economy was still growing even with all these pressure weighing down upon it which showed resilience and contextual strength…”given the apparent stability of inflation expectations, there is good reason to believe that inflation will move higher as the forces holding down inflation dissipate further….’’ Neither, according to Fischer, should the FOMC be prepared to wait for inflation to hit 2% before they move. That is a stance reflected recently by Marc Carney in the UK.

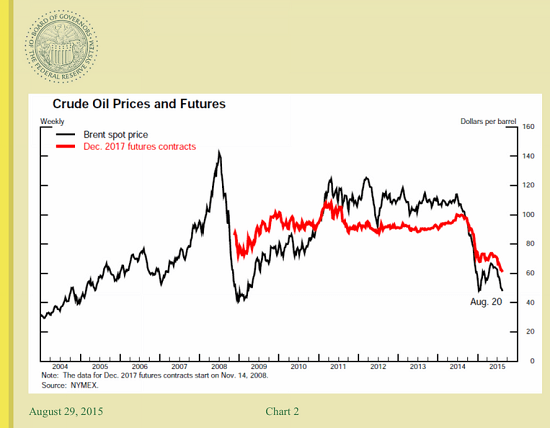

On the subject of oil, he isn’t the only observer that believes this to be a one off event. There is a consensus that the bottom has been found and whilst the ongoing supply/demand environment is likely to limit any rally many now anticipate a range developing with a bottom in place. Here is the official government chart of December crude futures against spot;

With the dollar strengthening as it has, consequences could be felt in the next two years via GDP and is expected by the Fed to affect the growth rates. Fischer sees that factor as one which will fade over time and furthermore he sees the current inflation status as stable and is not inherently a reason to delay. Sounds like he is ready. September is back on. Speculatively!

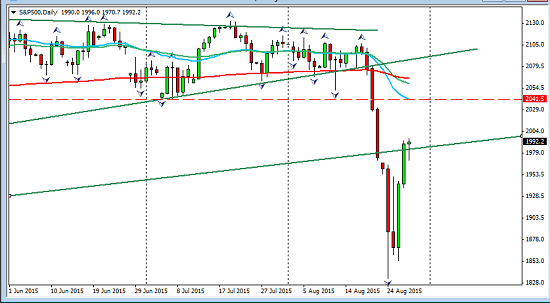

By Friday afternoon, the S&P had recovered Mondays downdraft and closed up for the week. It was however quite a ride;

Where from here? Well of course no-one knows, however the correction may yet have further downward points and at very least must pause to test some of the recent levels. If the Fed do indeed move this is a negative for the equities, if it is too nervous to move due to global insecurities then we may see bounces back to risk off fear and more selling. We would do well to remember that values have been considered to be over-stretched and that equity growth rates are not increasing as they once were.

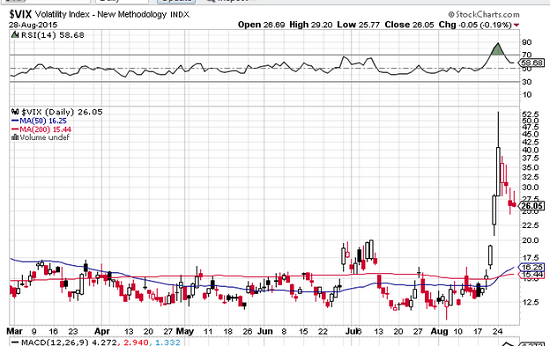

The VIX displayed the fear factor but settled back also during the week; chart courtesy of stockcharts.com;

So whilst fear was stirred, panic did not ensue, for now The US equity markets were calmed within a few days.

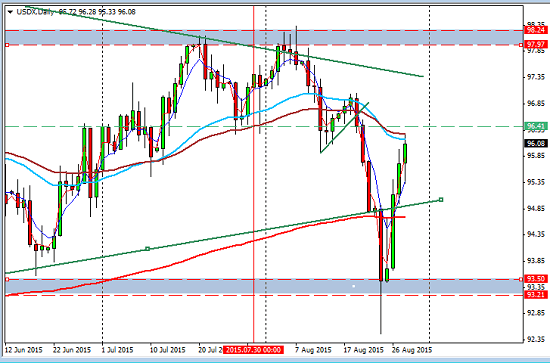

The USD index depicts the re-strengthening in the currency, well beyond Sunday’s open;

Forex Risks: Relief in Commodities

The rally was not just in the oil market but in copper, metals generally and the Index; chart courtesy of stocktraders.com

As with oil, we now have to monitor any potential range to develop and see if the market bottom is now in place. That means caution in the commodity related pairs which I shall be leaving alone for the coming few weeks. With Chinese issues still paying out there is possibility of further downside.

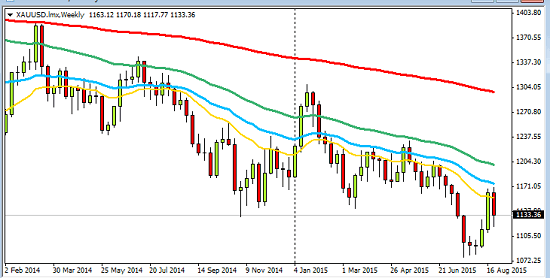

The Gold rally started three weeks ago and gave back ground as sentiment started to shift back. Shown here on a weekly chart;

As Commodities take a break the emerging markets remain under pressure. Continuing gloom in China will exacerbate the situation. The outlook for them remains weak.

Forex Risks: Europe and The UK

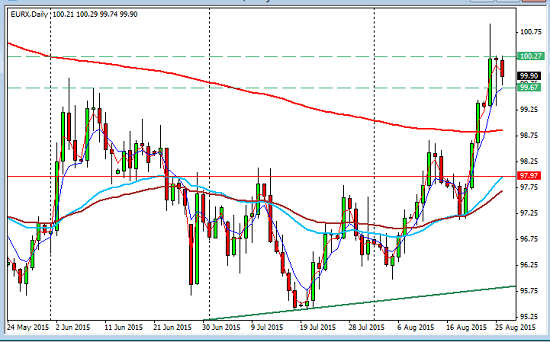

A brief review reveals a few problems. The Euro has seen strength as the index shows but it looks precarious;

The reason may well lie behind the concerns the ECB have on the Euro gaining too much strength. QE was designed to raise the equity market and stimulate the economy. Still in it’s fledgling stage we can expect the ECB to continue the policy of sustaining a cheap currency . This is how the Eurostoxx 50 behaved this week;

In the UK , things have looked a little less reliable than of late. There has been a feeling that the current account deficit ran by the UK government is not harmful unless there is a shock in the economy. Additionally, opinion as to the prospect of reducing it has deteriorated since December of last year.

We may have come close to such a shock last Monday. For now the sighs have been released (no, we didn’t hear them) and Marc Carney continues his more upbeat message at Jackson Hole…’’recent events do not yet, in my mind, merit changing the MPC’s strategy fr returning inflation to target….’’ he did add cautionary notes of the risk of ‘higher global risk aversion’ and spoke in terms of possibilities not certainties. All exits covered he left uncertainty in the air.

The Coming Week

Monday is a bank holiday in the UK . NZD business confidence.

Monday is a bank holiday in the UK . NZD business confidence.

Tuesday; MAJOR day, gives us PMI s from China UK , GDP from Canada, Aussie rate statement and the all important ISM US PMI. A market rocker day!

Wednesday ; Australian GDP , UK construction PMI, advanced Non Farm (yes its that time already!)

Thursday is Australia again, retail and trade balance, services PMI from the UK trade balance from the US and Canada and the big ECB meeting (watch out for that)

also included ISM non-manufacturing and unemployment as usual from the USA

Friday , Employment stats from Canada, PMI and of course the big one, Non farm and wage growth in the US.

Opportunity will need space. Focus for me is on the USDSGD, and the USD index, and an assessment (on-going) of the development of ranges at least until the Fed decision. Weakness in China has shown us the potential for shorting equity indexes and on bigger pullbacks these will become attractive.

First week back is massive on news, vulnerable to sentiment shifts and capable of sustaining the volatility that has become all too familiar. This past week should have prepared us for more uncertainty at least until the FOMC meet later next month. As Friday closed and a sense of calm returned, fear was replaced with hope. If these two concepts of sentiment find balance then we can look to some ranges developing across the markets. Even if they do, the potential remains for wild swings. Opportunities may be less stressful on the longer term trades and there is wisdom in waiting for a little more clarity from the US. One thing is for sure, sentiment is set to be fickle in nature and the only certainty there is, is further uncertainty.

Judith Waker

If you would like to learn how to trade like a pro check out our $1 offer by clicking on the banner below

0 Comments