What we have witnessed this past week may well prove to be the calm before the storm. The Greek debacle wends its way to an uncertain conclusion with at least the framework agreed..

What we have witnessed this past week may well prove to be the calm before the storm. The Greek debacle wends its way to an uncertain conclusion with at least the framework agreed..

For the Greeks, lured as they were into the shackles of a once private debt burden, both deal or no deal give them little optimism for the future.

The Troika insist on their pound of Greek flesh by way of austerity measures ensuring a further drop of Greek GDP even if the bail-out monies are ‘allowed’ .

This despite a unequivocal admittance from both Schauble and Lagarde that debt reduction and restructure is the only way for the Greek economy to survive. Its a no win for them whatever the outcome of this binary saga. In the UK Guardian, Varoufakis, from his now more objective stance coined it perfectly, ‘’It takes the mathematical expertise of a smart eight year old to know this process could not end well.’

There are nearly 3 million, a quarter of the Greek population living below the poverty line, another 4 million are close. They have 25% unemployed. Hard to see how this will not deteriorate.

As for the market, its fickle nature welcomed the prospect of Greece staying in the Euro as it seemed during the week that proposals were nearing the ECB requirements. It reversed to an extent the earlier warning signs of dwindling risk appetite, but even in the event of an agreement is unlikely to be of long duration.

The Chinese authorities added to the bubble of enthusiasm as they administered a band-aid to what may well turn out to be a severed limb of their illusiory wealthy healthy economy.

The allure of yield also plays its part as it becomes increasingly difficult to find it in the ‘safer’ options But cracks are appearing as fear is starting to creep into the framework of greed.

The Forex Sentiment Environment.

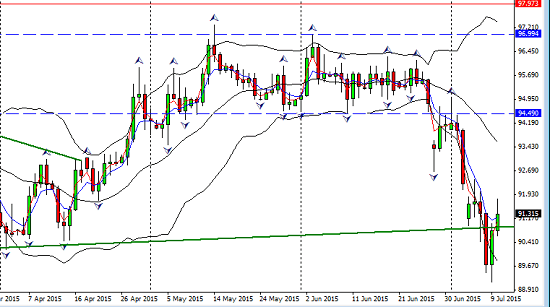

The S and P Index is the first risk check.

The S and P Index is the first risk check.

The fear element may well have taken it beneath the 200 day moving average as Chinese equities tumbled but the rally has shown relief from the ‘agreement’ as well as intervention from the Chinese government and a shift back to risk appetite. For now. The markets are politically vulnerable with so many issues, so wise to monitor.

If events favour a return to risk then there may be another leg but whether any additional rally is sustainable remains to be seen. Valuations are extraordinarily high and, risk discussion on one side, European equities are more attractive in terms of p/e ratios and there may well be a swap as Eurozone QE powers on.

Of course any shift out of the S & P for whatever reason can reverberate through trader sentiment.

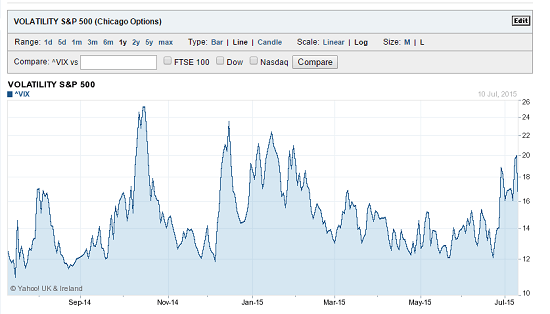

The Vix, the chart of the fear factor exclusively in the S & P showed signs of definite up moves though still not technically in ‘danger’ territory and with an expected pull-back in the latter part of the week,

Our sentiment pair the AUDJPY on the daily chart;

The was a recommended short last week and the time to close it was before the Australian data. It too reversed on Wednesday. The jury is definitely out on this one but a short opportunity again both fundamentally and technically if the risk environment confirms it.

The Big Red Bubble

Sentiment turned on a dime on Wednesday as the Chinese authorities intervened to prop up their stock market. That intervention showed a level of alarm that of itself can cause concern in the market place even if not immediately.

Sentiment turned on a dime on Wednesday as the Chinese authorities intervened to prop up their stock market. That intervention showed a level of alarm that of itself can cause concern in the market place even if not immediately.

Here is just how the authorities interfered with the market forces they have little faith in.

Firstly they manipulated the margins, both by decrease and increase which displays their own confusion. Secondly, they restricted short selling, with companies’ major shareholders banned from selling for six months.

Finally and perhaps most worrying from any economist’s viewpoint, the central bank moved in with significant equity purchases.

Add to this the fact that 1400 companies halted trading showing some distrust of their governments moves.

The problem with this is the delay of the risk factor, and of the fear factor. Preventing short selling is hardly going to entice international investment and the Chinese population are unlikely to be so gullible in future to the advice of the ruling party.

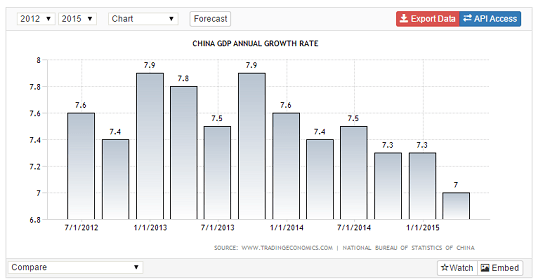

The Chinese second quarter results are published on Wednesday and the world will be watching. The concern for the global economy is obvious, charts courtesy of tradingeconomics.com

Here is the Manufacturing PMI index with 50 as the line between growth and decline;

And not surprisingly Chinese imports have been declining as a direct result. This affects all the countries which export raw material to the Chinese with an obvious focal point being Australia;

Singapore is another where a 1% drop in Chinese GDP transmutes into 1.6% drop in the Singapore GDP

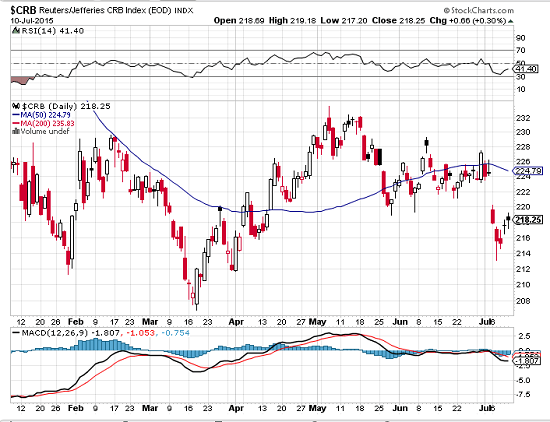

The commodity index looks troubled, with two gaps opening as the Shanghai index fell and an attempt to recover has not made a major impact, chart courtesy of stockcharts.com

Specifically on the Oil front, last week we discussed the opening of rigs in the US and this has increased again in the last week. A nasty drop last week is likely to see follow through and now the Iran deal has been sealed more supply will add to the glut. There is no sign that this will change in the near future with a further drop in prices anticipated in the futures market. This does not help the commodity currencies especially the Canadian dollar. It should be noted here that the recent Chinese equity rout also brought warnings of decreasing demand.

Monetary Policy

With the perspective that monitoring risk is the prime concern for the week ahead, it is important also to keep in mind monetary policies global comparatives and of course where exactly we are with the timing of the rate hikes in the US. The gaps in the TNX chart display more of the shifts in sentiment of late than they reveal clues for interest rate rises as the safety buying into treasuries lowers the yield and then reverses.

The FOMC minutes were somewhat buried in the dramatic events of the week, but due in some part to the fudging we are becoming more accustomed to. The truth is that there are very divided opinions and there are concerns from the global macro issues which the FOMC are watching unfold, as we all are;

Yellen talks of ‘approaching conditions’ that will warrant the first hike. Its all about data of course and the watch will be kept but there are other factors now and it all has to be considered in perspective . As it is, there was a dovish undercurrant and the speculation continues.

Of course, If risk aversion sets in again for any of the reasons above, then the US is well placed for further advances particularly against commodity currencies and the emerging markets. The usual suspects. Even if we see a shift back, it does seem that these two categories will remain under pressure.

As for the Euro, without the completion of negotiations the near term is unpredictable. Longer term it is a little clearer with QE continuing apace there will be opportunities to short the Euro. If there is a Grexit, Grexodus or a Grexaccident or whatever other terminology this crisis gives birth to, the shorting might be noticeably faster. There are two hurdles, The Greek parliament and the negotiations which will resume if passed.

Catalysts in the Week Ahead

It is another monumental week with all eyes on the EZ. But that isn’t all! Its policy week with statements from Japan, Bank of Canada and a couple of Yellen speeches.

Monday ,Chinese trade balance

Tuesday GBP CPI (inflation gauge) and Aussie business confidence. and also US retail sales, another inflation biggie.

Wednesday brings the all important Chinese Q2 data Japanese statement employment stats from GB, CAD manufacturing , rates and policy and the Fed chair testimony and NZD dairy prices and CPI. This is a big day and the New Zealand data

Thursday, no respite…more from Yellen’s testimony , unemployment claims in the US, and a US manufacturing index and an ECB press conference.

Friday will critical CPI numbers from the Us and from Canada.

Game Set and Mismatch

Power plays continue as I write. No-one should underestimate the political tensions within the EU let alone just the German / Greek enmity and not knowing the outcome, or indeed the outcome of the outcome second guessing is not an option. A deal could be doomed to fail within 6 months. Sentiment is now on daily watch and will dictate the direction of the global currencies.

The German camp continues to represent the biggest opposition to the Greeks with Merkel in the unenviable position of losing credit with either outcome. There are some Greek allies appearing including M. Holland and other members that wish to see Greek remain. We are very aware of the pro-exit camp who have even suggested a temporary version. Schauble again

As the weekend meetings conclude Mr Tsipras faces another deadline to get the austerity measures passed through the Greek Parliament. And then if they do, yet more negotiations. The meeting to discuss the Greek Exit planned Sunday and how it should be handled was cancelled. Small consolation for Mr. Tsipras but it is stay of execution. Then there is the alternative… a life sentence for the Greek in debtor’s prison and the promise of more austerity and more hardship.

The outcome of the Chinese manipulation of both market forces and their own people may take time to reveal itself. Niether can that be predicted.

Geopolitics have taken centre stage and demand our full attention. So too does the sentiment it provokes among the trading community. There are plenty of catalysts and therefore opportunities but they will be potentially dangerous unless the environment is closely observed and understood.

Judith Waker

0 Comments