That is the stark reality for the Greek government. There are cries from the world ‘order’ that they accept the loans and the conditions. Deeply political as this state of affairs is, it will require a political solution.

That is the stark reality for the Greek government. There are cries from the world ‘order’ that they accept the loans and the conditions. Deeply political as this state of affairs is, it will require a political solution.

There is a chasm between the two sides and for the Greeks if they keep the Euro, they know austerity will bring more hardship lower incomes and pensions and no prospect of improving GDP. That is to say…more of the same . That maybe an over-simplification but there is a real feeling of ‘damned if they do and damned if they don’t.’ It is no wonder a stalemate has been reached.

There was an anticipation this last week for the possibility for a change in risk appetite in the market. Had the Fed turned hawkish together with the looming Grexit risk there would have been plenty of reason for a change in attitude and some fear to creep in. It did not, and shows that the market were much more focused on the Fed, which was decisively dovish and cautious and not too much concerned with the crisis in the Eurozone. Not yet anyway.

There has been something of an assumption that an agreement would be reached and that could all change and rather quickly. All eyes focused therefore on what comes out of the Euro emergency meetings.

Christine Lagarde, only a week ago warned America not to raise their rates this year. I probably wasn’t alone in enjoying Janet Yellen’s calm but firm rebuff of Lagarde’s interference in her FOMC address on Wednesday.

Much more on that in a moment, but staying on the Greek issue Madame Lagarde didn’t help euro relations this week by suggesting that to make progress she wants to talk to adults. She acts for creditors and they want their repayments and their interest.

Much more on that in a moment, but staying on the Greek issue Madame Lagarde didn’t help euro relations this week by suggesting that to make progress she wants to talk to adults. She acts for creditors and they want their repayments and their interest.

It is a complex issue but really difficult to see the logic of lending more to enable the repayments and difficult to believe that this organisation thinks such a policy will bring any benefit to the Greek GDP and to their people. For the Troika it is rinse and repeat.

This is an intensely political fight. For the Eurozone, a lot is at stake with the peripheral bond yields edging up, showing us that a ‘Grexit’ will stir up anti-European rhetoric in their strengthening extreme parties.

Then there is Britain; with a referendum ahead on whether to continue membership of the EU and another negotiation under way for better terms. They also jealously guard their democratic sovereign nation.

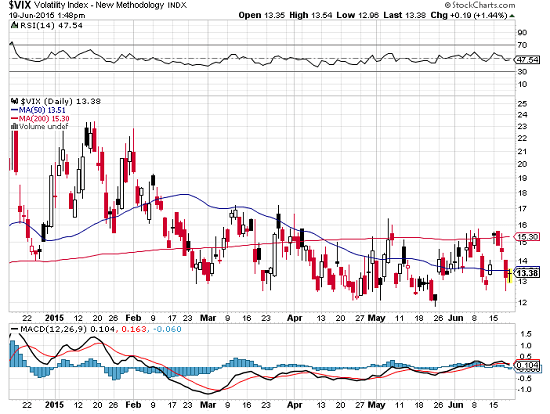

It is clear that time is running out for a deal between Greece and the EZ and it is very much a binary event and with the stakes so high it is a little surprising that the market is so calm. Its resilience this week has been seen in the decreasing VIX, chart courtesy of stockcharts.com

And also in the VSTOXX, the European version, which on the rise , in relative terms doesn’t seem to be factoring in a black swan

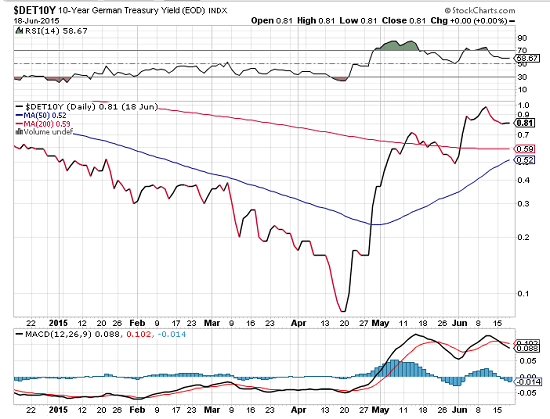

The German bund yield corrected this week after its uptrend briefly flirted the 1% level;, courtesy of stockcharts .com

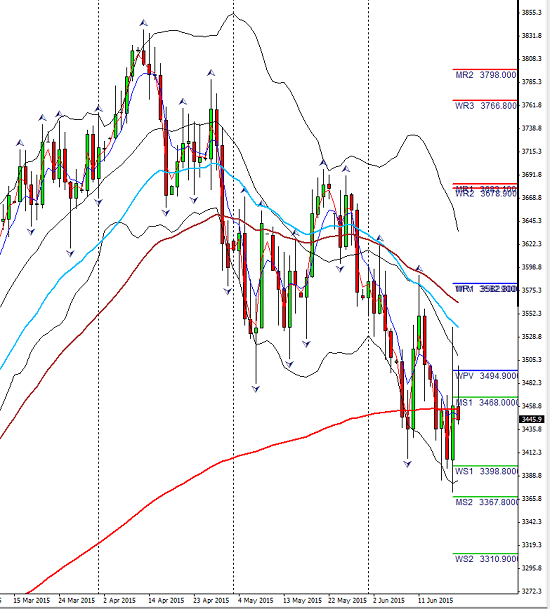

and here is the state of the Euro Stoxx 50…a technically critical place but by no means indicative of a fear-ridden market;

Is the market is expecting a deal? Complacency is dangerous and sentiment can turn on a dime. We need only look at China this week to understand that. If the deal is struck, then we can expect a volatility surge and an up-move in the Euro and the cross pairs. It may also be short lived. The data is improving but it is slow. As Draghi himself has stated, we can expect further volatility in the bond market but if yields continue to advance that leaves companies and households with increasing costs. If there is no deal then we can expect the yields to rise in the peripheries, Spain Portugal and Italy.

There was no major data from the EZ this week but of course no shortage of news releases. The ECB did purchase another 74 billion bonds above the monthly target so any improvement economically is clearly not translating to the ECB as a reason to slow the QE process down.

Forex Fundamentals; FOMC…Behind The Numbers

The unexpected extent of dovishness in the language of the FOMC chairwoman caught the market off-guard again. With recent strong data particularly in the last NFP but also in core retail and PPI and improving sentiment we were ready for the dot-plotters to show their hand. Actually they did, and their hand was something of a contradiction to their words. 10 members think the rate will increase to 0.63 by the end of this year, 15 members think it will increase to 0.38.

The unexpected extent of dovishness in the language of the FOMC chairwoman caught the market off-guard again. With recent strong data particularly in the last NFP but also in core retail and PPI and improving sentiment we were ready for the dot-plotters to show their hand. Actually they did, and their hand was something of a contradiction to their words. 10 members think the rate will increase to 0.63 by the end of this year, 15 members think it will increase to 0.38.

That means that there will be a rate hike this year…they all agree on that. It also means that since rates have to be raised in small degrees to avoid taper tantrums, the other 10 are envisaging 2 rises. That means September will be the first. It is a minority view but 10/25 is still significant.

Yellen accepted the improvements in the labour market but retained concerns about the inflation target and wants to see further evidence before setting hikes into motion. It was a ‘could do better’ attitude. Her view was to stay accommodative ‘for quite some time’ . She rebuked the market for paying too much attention to the timing of the first hike and not enough to the trajectory of the raising schedule which will be slow and gentle. She also made it clear , in very subtle ways, that whilst the IMF played ‘a useful role’ policy in the US was for the Fed and was completely data dependant.

Yellen also was asked about Greece and warned that a Grexit would cause a global reaction and negatively affect all economies including the US.

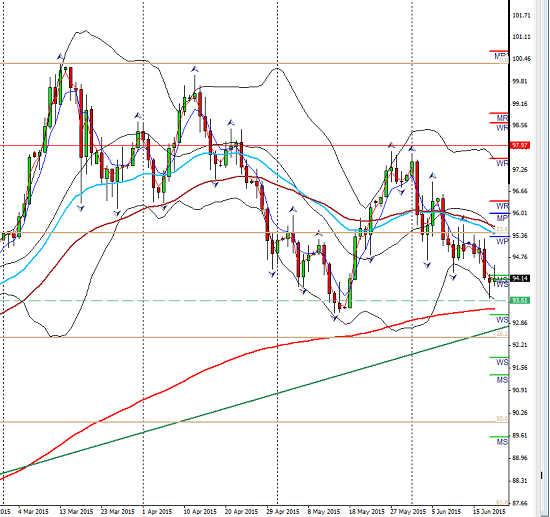

The USDX lost ground following the softening tones of the Fed

This is currently sitting on monthly support and has a daily bullish candle and of course there is a 200 EMA below.

Forex Fundamentals: UK Economy

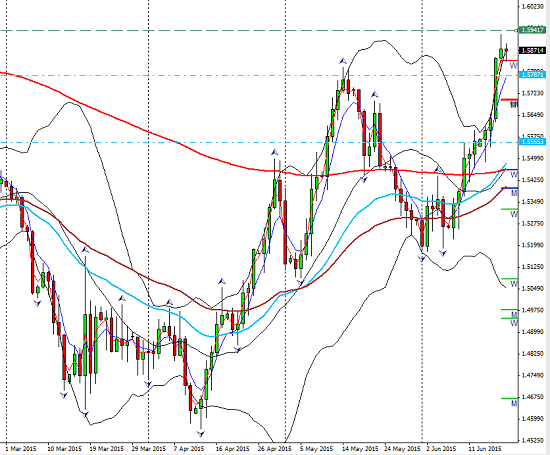

Average earnings on Wednesday indicated another step towards inflation, despite the unemployment numbers disappointing. Later in the week retail sales also showed the same evidence comfortably beating the number. Mr. Carney confirmed that the next step will be a rate rise, not a cut but he did add a note of caution that a strong pound will be likely to delay the hikes. This is the chart of the strengthening at the end of the week’s trading, that may cause a little concern; The dotted green line is major weekly resistance and not surprisingly close to 1.60;

The trend was overextended, outside the bollingers at the end of last week and technically dangerous and has corrected in the first day of the trading week.

Forex Fundamentals; China and the Antipodes

The bubble in the Chinese equity market discussed a few weeks ago has lost air and is deep in correction territory;

The Chinese economy is either changing drastically in its area of focus and structure of it’s GDP, or is failing. Either way the decreasing demand for raw materials has the potential to devastate the emerging markets and of course the commodity currencies most particularly the Aussie dollar.

The CRB has been in decline although consolidated its lows recently, there is no sign of further improvement as demand dwindles.

The minutes of the RBA monetary statement showed the committee will stay accommodative and Mr. Stevens views on the Aussie dollar being too strong are well reported. The bias is bearish on the Aussie dollar.

In New Zealand another lowering of dairy prices and worries about GDP not to mention the recent rate cut and the forecast of more to come has meant a decline in the NZD across the pairs. It remains bearish but the trends also may also be a little overstretched so expect some pullbacks.

Oil on Troubled Waters

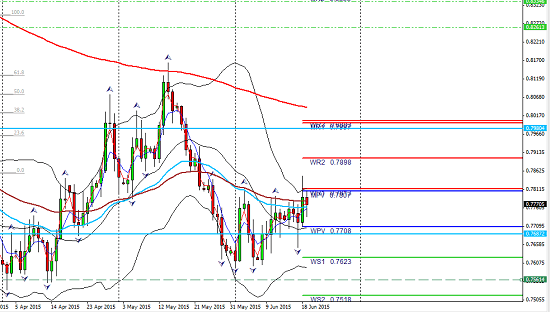

The good old ‘loonie’ has showed some strength of late due in part to an oil price which has held through a consolidation of the correction highs and because of its own strong data. This is another currency to be wary of . This is the USDCAD , weekly perspective;

Oil has seen additional supply from the North Sea as well as the Middle east so the glut continues as inventories continue to swell. The price dropped towards the end of last week and this will affect the Cad dollar if it continues downward. At present it remains in a very tight range so we need to monitor this one.

On a technical note. The 200 EMA has been tested (and failed) 5 times and there is no fundamental backing to the prospect of a break higher….yet!

In Canada a mixed bag as manufacturing numbers missed their mark and core CPI came in a little higher. However core retail missed as well.

Kuroda Back-Peddles

Also in the news, Kuoda stepped up again earlier in the week to (not so subtly) change his view and that weakness will not harm the recovery of the economy. This from FX Street ”Kuroda said those comments were unrelated from the nominal exchange rate, and that as long as FX moved in a stable manner the level of Japanese currency was not of concern.”

This rather softer tone had the expected effect although it did re-strengthen later in the week for different reasons.

With the anticipated risk aversion not manifesting this last week as explained above, this also weighs on the Yen which will be a candidate for strengthening should fear enter the market. For no it has not but it is an environment to closely monitor in the days ahead as Europe tries to solve its issues.

What to Watch for In The Week Ahead;

Not a huge calender, but of course major potentially game changing events in Europe will take centre stage with the summit on Monday. No-one understands the consequences.

Not a huge calender, but of course major potentially game changing events in Europe will take centre stage with the summit on Monday. No-one understands the consequences.

Tuesday, USD core durable goods, Euro PMI , JPY monetary policy minutes

Wednesday, USD GDP (this one is very important as the FOMC keep reminding us we are data driven!)

Thursday, USD unemployment, NZD trade balance

Friday Dr. Carney again!

Conclusion

Whatever the calming tones of the Fed chair this week, the hawkish outlook remains. The US will raise rates this year unless there is a drastic change in the data . That makes Wednesdays news critical. There is another factor. If the Greek crises transmutes into that black swan or if the Chinese equity correction becomes a major sell-off then market sentiment could change drastically. The US woud be considered as one of the safe havens and this could potentially give it a clear edge.

Wait and watch what the market are looking for and what they are looking at, how they have digested the Fed stance and of course the outcome of the meetings in Europe. There will be huge pitfalls to avoid, which includes unpredictable volatility, potentially on a big scale if things go badly for Greece but with them could be some profitable opportunities. Be very careful and best advice is to avoid the market until the European decision is made. Whenever that may be!

Stay tuned!

Judith Waker

0 Comments