It was another of those weeks. All the major equity markets saw strong down weeks, there was manic German Bund selling, yields popping and the VIX jumping from 12 to 15 at its high point, though retreating at close. As if the mix wasn’t confusing enough The US double whammy on Wednesday confused us a little more. As GDP points to slowing growth and downgraded forecasts for the next quarter, the FOMC bounced back with a comparatively upbeat dismissal of the softer data, a refusal to let the June rate option go completely, although the market has discounted it, and a view that the current conditions are ‘transitory’. Seasoned pro traders took forex losses as the Euro steamed ahead on Wednesday, and on a bank holiday in many parts of Europe the USD reversed suddenly to pare some of its losses. Head-spinning stuff.

As the week closed there is a real sense of TGIF and the weekend has given a chance for re-grouping and preparing for the next round.

Is Euro Euphoria over

The stock buying in the wake of QE in the Eurozone may have got ahead of itself as the charts the DAX implies.

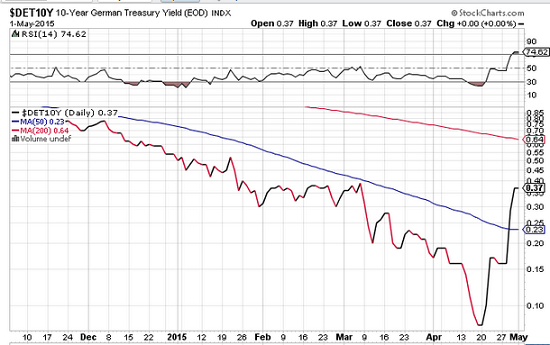

Of course the ECB have announced the intention to continue throwing 60 billion into the market every month for at least a year so it may be too early to consider the equity buying over. As for bunds, few expected the pop seen in the German 10 year yield particularly this week. Creeping closer to negative territory, it was seen as Bill Gross put it as ‘the sell of a lifetime’. The sale was on a big enough scale to send the yield 20 basis points to 0.37 as funds sold in favour of US treasuries, in a safer search for yield.

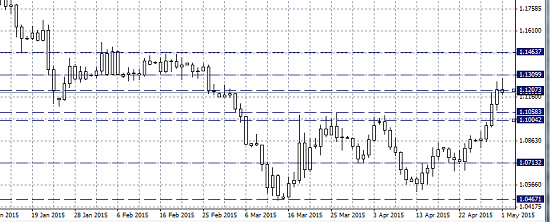

The effect in the Forex was just as dramatic with the Euro sent into a powerful up move that left a lot of surprised shorts at 1.10 and then 1.11., 1.12. It came close to 1.13 before closing back off its highs.

This was little to do with the US and the continuing soft data. This was all to do with the selling in the Bund. The volatility in the Forex market makes playing probabilities that much harder and little has changed with the European underlying fundamentals. With QE continuing there are issues which are unlikely to be resolved anytime soon, if ever, with fiscal structures in the Eurozone countries, and whilst growth prospects are a lot more optimistic than they were, they are still fragile. It is also true that inflation data looks more promising but there is a long way to go to sustain the first signs of improvement.

There is also the question of Greece, despite renewed hope of a bailout and more compromises coming from the Greek government it remains a loose canon in the zone and the bank balance continues to reduce.

The last shall be first

In the US the final pieces of data confirmed the softening trend. ISM PMI missed the expectation and came closer to the 50 danger level at 51.5. Consumer confidence was close to the number. Earlier in the week GDP in the first quarter was a miserable 0.2% .

In the US the final pieces of data confirmed the softening trend. ISM PMI missed the expectation and came closer to the 50 danger level at 51.5. Consumer confidence was close to the number. Earlier in the week GDP in the first quarter was a miserable 0.2% .

The first US quarter is historically low due to seasonal effects but even so in the current economic climate it was bound to cause concern. And it did with a downgraded Q2.

The Fed have completely abandoned any guidance and continue their data watch as we must to. Uncertainty and volatility can only increase under such circumstances. It can be an expensive guessing game as some traders discovered this week.

From here, it requires, as we are now accustomed, to a careful monitoring of data and of course next week holds the famed NFP. That is sure to move markets if it beats or misses so the interconnected market place will be watching and the chances of volatility are very high.

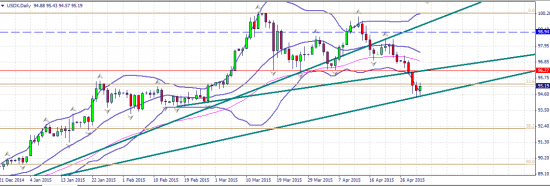

For the USD despite the last pieces of data for the week there has been a rally into the close . That seems a contradiction bearing in mind we are data dependant, though Thursday did show a marked improvement in jobless numbers. What we now have to watch is whether the ‘correction’ is over or pausing and I am afraid the answer will not come at least until NFP is announced next Friday and could be well after that. One cannot deny the interesting technical perspective of the USD index;

One thing can be added and that is no positions should be taken on the majors unless there is good confirmation. If in doubt a trend-line break is the most conservative. It is also a position to patiently wait on the sidelines.

Whats ahead for Oil

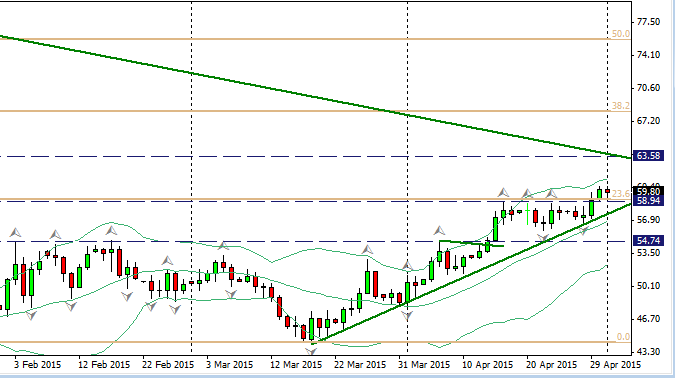

As we have seen in the last few weeks, and indeed since the oil route began last summer, a lot of decisions ride on understanding this market. There is a weekly resistance that broke and held on a daily basis and that technically implies a continuing rally.

However, in this blog I have often considered the sustainability of a rally in oil and many factors still stand in the way. Inventories this week slightly missed the target but they are still growing and there are prepared fracking sites waiting for a rise in price to begin operations…which could bring it straight back down…The weaker dollar has fueled this rally but from here there is much uncertainty (a familiar theme!) and there has not been a let up so far in Saudi production.

The crude oil chart also reveals an interesting situation. The daily shows the break of the weekly area

The Canadian Dollar has seen a strong rally partly because of the oil rally but also a much more upbeat outlook from the BOC. They are of the opinion that the worst is over and that enough accommodation has been provided to stimulate a recovery. Some of those gains were surrendered in the last day of the trading week. Watching the oil market is critical in any cross pairs and of course the major requires understanding of the USD correction as well.

The Asian effect

Japan has seen PMI fall to 49.9 below the critical divider between growth and recession. Wage improvement has not been achieved and growth outlook continues to be bleak. That may invite more aggressive action from the BOJ .

The PMI in China is also close to the 50 level at 50.1. and the implications for the Australian economy are worrying. The rate decision ahead in the coming week warrants attention and there is a feeling they may cut the rate. This coincides with the trade balance data and offers another volatility catalyst. Certainly a rising Aussie dollar could cause problems and certainly that is something the RBA will want to prevent.

The UK Election: Neck and Neck

It looks like a certainty that the UK will have a hung parliament with no party gaining a working majority. That means a scrabbling for a coalition with some strange combinations possible or another election after a few ineffective months.

It looks like a certainty that the UK will have a hung parliament with no party gaining a working majority. That means a scrabbling for a coalition with some strange combinations possible or another election after a few ineffective months.

Either way this is not good for the economy for the trading sentiment or for the strength of the GBP. The data disappointed also this week PMI slipping to 51.9, GDP at 0.3% and consumer confidence slipping also. The GBP slipped back on Friday to 1.5135.

The Week Ahead

NFP Friday; need I say more? PMI’s and USD and CAD trade balance both on Tuesday to watch for NZD employment numbers. A huge week for the Aussie with the rate decision on Tuesday and trade balance and retail sales the same day and jobs numbers on Wednesday. This will be a week offering many opportunities for further choppiness.

There is an expression in the market that goes thus; Sell in May and go away. It could be good advice but if you you stay and trade, keep risk control as the number one priority, keep positions small and stay ahead of the news curve. If you want to make profit in a market like this one you will need discipline and control and you will have to negotiate some difficult conditions.

There is an expression in the market that goes thus; Sell in May and go away. It could be good advice but if you you stay and trade, keep risk control as the number one priority, keep positions small and stay ahead of the news curve. If you want to make profit in a market like this one you will need discipline and control and you will have to negotiate some difficult conditions.

Safe trading

Judith Waker.

0 Comments

Trackbacks/Pingbacks