Last week’s focus was on the Fed and Janet Yellen’s testimony to the Senate committee. What she said and the light she threw on the FOMC’s rate intentions is critical to assess, especially with the USD index at record highs. There is no let up. This week we have had the RBA, and ahead the BOC, the ECB and the BOE all to deliver rate decisions, except the ECB who are expected to start providing details of the QE project. Four economies all in different places and circumstances vying for their place in the global structure with a focus on one goal; recovery against a background of global deflationary pressure.

Forex Insights; FOMC

Starting first with the Yellen transcript last week, and the inevitable and plentiful interpretations. It was in its simplest terms a bit of a fudge and one I beleive to give her plenty of wiggle room in a country that demands policy transparency. Mildly hawkish, especially as she left the blocks with an upbeat report of economic recovery so far. It didn’t last long as she turned her attention to the difficulties abroad resulting in the inevitable challenge and delay in reaching the magic 2% inflation target. Thereafter, there was plenty for the doves to alight on;

Starting first with the Yellen transcript last week, and the inevitable and plentiful interpretations. It was in its simplest terms a bit of a fudge and one I beleive to give her plenty of wiggle room in a country that demands policy transparency. Mildly hawkish, especially as she left the blocks with an upbeat report of economic recovery so far. It didn’t last long as she turned her attention to the difficulties abroad resulting in the inevitable challenge and delay in reaching the magic 2% inflation target. Thereafter, there was plenty for the doves to alight on;

”In response to unforeseen developments, the Committee will adjust the target range for the federal funds rate to best promote the achievement of maximum employment and 2 percent inflation”.

This was indeed a shift away from the focus on jobs despite the recent positive data and she still saw slack that inflation problems are not going to help;

”This judgment reflects the fact that inflation continues to run well below the Committee’s 2 percent objective, and that room for sustainable improvements in labor market conditions still remains”.

However, GDP despite disappointing is promising on an annual basis when compared to the year before and there is still no doubt that the USD has been bucking the global trend for a considerable time. No-one disputes the fact that in the big picture the US is ahead of the pack, in fact most of the pack are heading in the opposite direction so the winning line of rate hikes is a no-brainer.

What is less clear is whether the USD trend continues at its previous pace and that now seems less likely. Let us see if the range breakout seen Thursday can sustain itself as we move through this ‘Central Banks’ week;

As the future becomes less and less predictable, I can only stress the importance of selecting trading pairs according to the relative strength of the economies in question, as this necessity can only increase in importance. This is dealt in more detail below.

A word about the US 10 year treasury yield. The Yellen speech saw a spike up and then it whipsawed down, overall this month however the sentiment is a little brighter and bond demand has slowed raising the yield.. The US 10 yr note has risen from 1.67 at the end of January. Some analysts even think this may be an indication that there is still possibility of the Fed moving in June.

Fed ‘speak’ will be in focus in future meetings, the since word patience has been under watch, Yellen went as far to say that when it is dropped the rate rises could happen in any meeting thereafter, depending on data. I have seen opinions in well respected publications that disagree about whether the hike is most likely in the summer or in September.

As if speculation is not running high enough, we have NFP at the end of the trading week. It is going to be a critical piece of data and necessary to watch out for wage pressure indications as well as employment numbers. This may prove to be ‘the piece’ of data that can remove the word ‘patience’ if it it is a strong one and now Yellen’s focus has shifted to inflation the wage growth data is likely to carry even more weight.

Forex Pairs to Watch

The Dovish Economies

Of course there is another side to the equation. The rise and strength of the USD is not just about the FOMC and the data coming out of the States. The indirect effect from the policy and events elsewhere will without question take its toll on the USD as the dollar can be pushed up or down by perceived (and actual) weakness or indeed recovery elsewhere.

The week ahead has major catalysts from four other economies that can effect the USD one way or another and push it beyond the range it has maintained this month.

The Euro also suffered big losses last week as the market awaits Thursdays meetings and the details they expect to receive. QE will start to be felt in the market. For now, it is all quiet on the Greek front and I should add that German CPI (prelim) beat the expectation.

The Euro also suffered big losses last week as the market awaits Thursdays meetings and the details they expect to receive. QE will start to be felt in the market. For now, it is all quiet on the Greek front and I should add that German CPI (prelim) beat the expectation.

The bias has been negative but watch carefully to see if improvements start to get some traction at current levels. It is fair to say that even with strong down days last week it has maintained a weekly range.

The Aussie saw weakness in the later part of the week ahead of the RBA meeting. There was uncertainty as to whether the RBA will follow through its last decision but the majority were expecting a rate cut, and in that context, it is worth noting that Governor Stevens would prefer the AUD down at 75 to promote recovery in the economy.

The decision not to cut was a mild surprise but the easing bias was clearly stated. There has been a subsequent move up but it is unlikely to have ‘legs’ as the market digests the news.

Meanwhile, and of great importance in Australia the Chinese cut its rate for the second time on Saturday. Their final PMI crept over 50. It should be stressed that exports however, fell worryingly. Chinese rate cut will have its effect on the Aussie. The bias is still down .

In Canada on Wednesday, another rate decision and another possible cut. Canada has been effected more than most by oil price drops and although crude has had a better month there is still doubt that it can sustain a rally . Certainly US rigs are still closing but it is also true that inventories are still rising. I think a wide range for the medium term at least is the most likely prognosis for black gold. In that oil range the Canadian economy will continue to bare the effects for some time to come and thus long opportunities in the USDCAD are to be preferred on a decent pullback or any impetus from the BOC.

The Hybrid; The UK.

With clear signs of recovery the GBP has done well this month against the USD , data will be important and maybe more so than the rate decision due on Thursday which is expected to keep the current rate. Carney was hawkish at his last opportunity but the hike will be data driven and whilst improving it is slow at present.

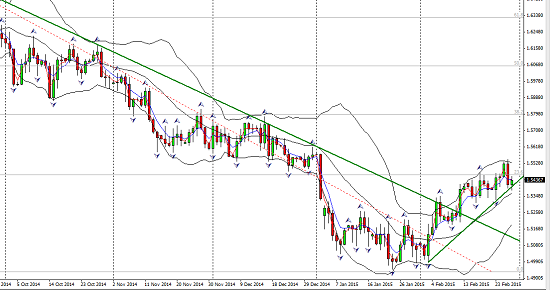

The EURGBP still has downside potential, but there is an election in the UK to keep in mind and continuing improvements in Euro data will be a signal to tighten stops if you are in this trade.

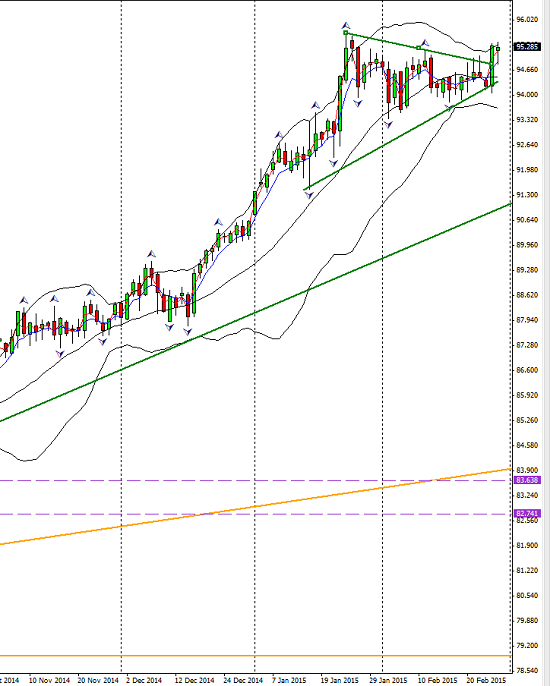

As for the GBPUSD, they are both on the hawkish side of the curve and thus not predictable enough in terms of relative strength. There are better options. Here is a picture of the recent push against the dollar, now resisted at the 23rd Fib;

Forex Risk issues

A very strong week for global equities may belie a truth. The European bonds and bourses have seen significant inflows ahead of the anticipated QE details this coming week. Bond yields on the negative side are becoming more common. The S and P is reaching for an all-time high but does this mean risk-on?

The vix has dropped for another week but volatility has been seen elsewhere including in the Forex.

This may well be an unreliable’ risk-on’ environment and one to watch. There is some evidence of equity positions becoming shorter term.

As always we also need to monitor geopoliticals news which includes a fragile peace treaty in the Ukraine, the death of Putin’s adversary and the IS, running short of funds continuing to make its presence felt.

For now, risk appetite is strong and may grow or change so be watchful!

Trader Beware!

There is a massive amount of news to come in the week ahead and a lot of insights to be gained and potential opportunities as well as risk. In terms of global economies, nothing fundamentally in the big picture has yet changed as far as the status and policies of the major economies but the shifting sentiment can cause unexpected movement, and it is not simply identifying risk environments. That is long term sentiment. Short term sentiment is at the root of the current choppiness and in some places the whipsawing we have seen of late and there is no shortage of catalysts for more of the same in the week ahead.

Judith Waker

0 Comments