Trading the Forex successfully is not just about finding a system. They rarely work for long and as market circumstances change so do results. Successful trading requires knowledge of the market drivers before any technical system is of value and before any decision is made. Fundamentals and technicals is not a choice. It is a winning combination.

Trading the Forex successfully is not just about finding a system. They rarely work for long and as market circumstances change so do results. Successful trading requires knowledge of the market drivers before any technical system is of value and before any decision is made. Fundamentals and technicals is not a choice. It is a winning combination.

Market sentiment and how it affects market behaviour is just one of the concepts that can provide some Forex clues and recently there have been many to monitor.

Last week, with the volatility index of the S and P in decline again and stock markets rallying ever upwards to set new highs one would be inclined to think that risk adversity among our fellow traders was non existent.

Indeed, Greek issues continued to dominate the news desk with deals being struck that there is little confidence in, growing disharmony in the EZ and a constant replacement of one deadline with another, not to mention the increasing appearances of Putin in unexpected places such as Hungary this week. It would quite acceptable to assume a little fear showing up in the usual places .

It isn’t, as we shall see , so I had a look behind the events and the data to see if I could make sense of the current sentiment. What I found should perhaps put us on guard.

Forex Fundamentals; The State of Play

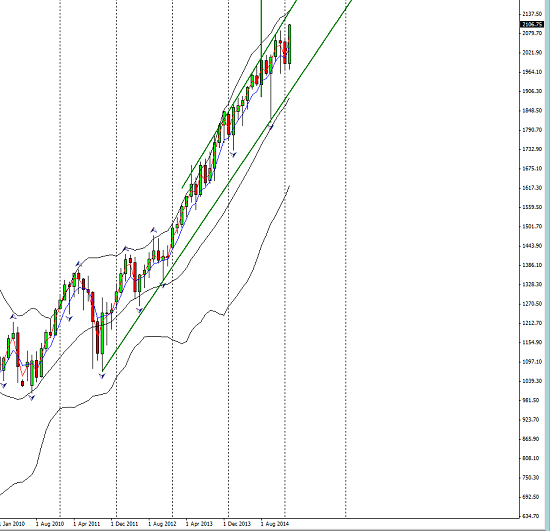

A quick review of the week saw a rally in the S and P. Just to put this in context, this is a monthly chart;

Similarly there was rally in the Dax; this is a daily view but nonetheless impressive and entirely to be expected after the QE announcement;

Gold saw another week of lower prices somewhat erasing the recent uptrend;

and a drop in the vix, our sentiment standard!; (chart courtesy of stockcharts.com)

The market seemed to be ignoring the Greek issue and the reaction was muted even when the deal was struck at the end of the week.

One cannot do a state of play review without a look at the USD index, showing a weekly consolidation;

As I said last week, clearly on a break and a lot of talk lately about the extent to which rate hikes, FOMC transparency, likely moves and anticipated data improvement have been factored in already so where can the USD go from here?

I repeat the view that a more careful selection, reviewed week to week, can help keep us long the dollar and out of trouble. And that is only if circumstances allow it.

The truth is IF deflationary trends are perceived as getting a grip and increasing in the other vulnerable major currencies, then the USD stands to gain whatever has been factored in.

If, however, improvement in the struggling economies is discerned, then expect at least a pullback in an index that has grown fast and furiously to its current levels. It always windy at the top!!

The data from the US is maybe strong enough to get the hawks exercising their wings a little ahead of Janet Yellen’s testimony this coming week. Building permits and PPI both missed early in the week, but the big number, unemployment went well beyond the expected number and they finished on Friday with a strong PMI.

I cannot stress how important Ms Yellen’s testimony is, even with our focus in southern Europe. Rest assured she will choose her words very carefully and the market will be listening.

Commodity prices

There is an consensus that oil has found a bottom, whether it has the conditions to permit a sustainable rally remain to be seen.

There is an consensus that oil has found a bottom, whether it has the conditions to permit a sustainable rally remain to be seen.

I have my doubts as the struggling producers that caused the glut will be enable to come back on stream as the prices rallies causing continuing inventory rises and the consequent supply issue.

Last weeks US inventories showed another rise even at the current price, and this will continue downward pressure on the Loonie.

Iron ore is another example. The week’s rally gave the Aussie dollar a boost, but the outlook is not particularly good as there is a mining resource expectation that more iron ore will arrive in the market as demand shrinks.

The bias for commodities remains neutral to down and in the medium term that is true at least for both the AUD and the CAD

It is interesting to note that only last week, the governor of the RBA re-iterated his view that the Aussie needs to go lower to refire the economy. He has the means and has already marched in that direction.

In the new age order of global competitive interest rates the downward spiral is not going to increase the chances of sustainable rallies in the commodity currencies, Japan, China or the Eurozone.

The commodity currency group winner last week was New Zealand. An upbeat dairy auction showing upwards price pressure pushed the Kiwi to

0.75733 against the USD retreating to0.75211 at close . This week, disappointing inflation data has had a negative effect on price.

Asian Growth

Japan data now shows tentative growth, the stock market is hitting all time high and GDP data shows the economy is technically out of recession. Its only one quarter and was below estimates. This recovery is fragile at best and is export driven with consumer sentiment still ’soft’.

The JPY seen here on a lite forex chart shows the strength of the Yen against the basket of others. A strong up move currently consolidating on a daily perspective;

More data from the UK

As the watchers wait fro signs of trend reversal in the GBPUSD, the data has shown mixed signals. Unemployment is falling and wage growth is at its best rate for 5 years. Retail sales however missed the estimate and sank to 0.3% in January.

Analysts do feel that consumer spending will rise this year, despite a disappointing number as wage growth gets traction and confidence rises. There is the question of the election so data on this one has to be used for short term advantages or forward looking projection after the May events have played out.

Identifying Fear

There is, on closer inspection a shift in the sentiment and clear evidence that the market is in fact watching the crises in Europe and tentatively trading around it. One of the places to search for a real sense of the market psyche is in the futures pit. There traders must factor in the risks of such big events and possible eruptions as they position themselves in forward months. Just how they behave and where they are shorting and longing, can be very insightful, especially the commercial traders (aka the big boys)viewing how they see the market unfolding and their current sentiment.

Additionally there is the question of volume. In the last week, almost all major pairs showed low volumes.

Volatility is showing up elsewhere and more can be expected, so sentiment is changing and there is a lack of commitment to a longer term view which may well persist until the Greek issue has been resolved. That could be some time, although the current ‘agreement’ looks to have calmed tensions at least for the short time as attention turns to the Fed this week.

Market-Watch

Once again we have a catalyst list!

The Greek’s are filing their list of reforms to the EZ by Monday.

Tuesday and Wednesday is Yellen testimony.

Draghi is also speaking on Tuesday.

The BOC governor Poloz speaks, again it is on Tuesday. Rate declines in Canada are in the watch list for sure.

Chinese PMI early Wednesday morning subject to the usual allowances for ‘tweaking’.

Finally US CPI on the schedule on thursday and German CPI on Friday.

Not a quiet week even by recent standards.

Consumer price indexes are all about inflation and deflation so they are noteable market drivers.

We will keep a monitor of fear in the market. Remember that fear does not always act precipitously. It can stand back from the action, keep hands in pockets and await direction. There is only one thing harder than spotting a trend change and that is understanding the mood that controls it.

Judith Waker

0 Comments